What is a sole trader?

A sole trader is a self-employed person who runs their business as an individual. You’re legally the same entity as your business, meaning you're personally responsible for any debts and obligations.

This structure is widely used by freelancers, tradespeople, consultants, and small business owners.

Key features of being a sole trader include you:

-

keeping all profits after tax

-

being personally liable for any losses your business makes

-

having full control over your business and its decisions

-

needing to register with HMRC and filing a Self Assessment tax return each year

Being a sole trader is ideal if you’re just starting out, testing a new business idea, or running a low-risk operation.

How to register as a sole trader

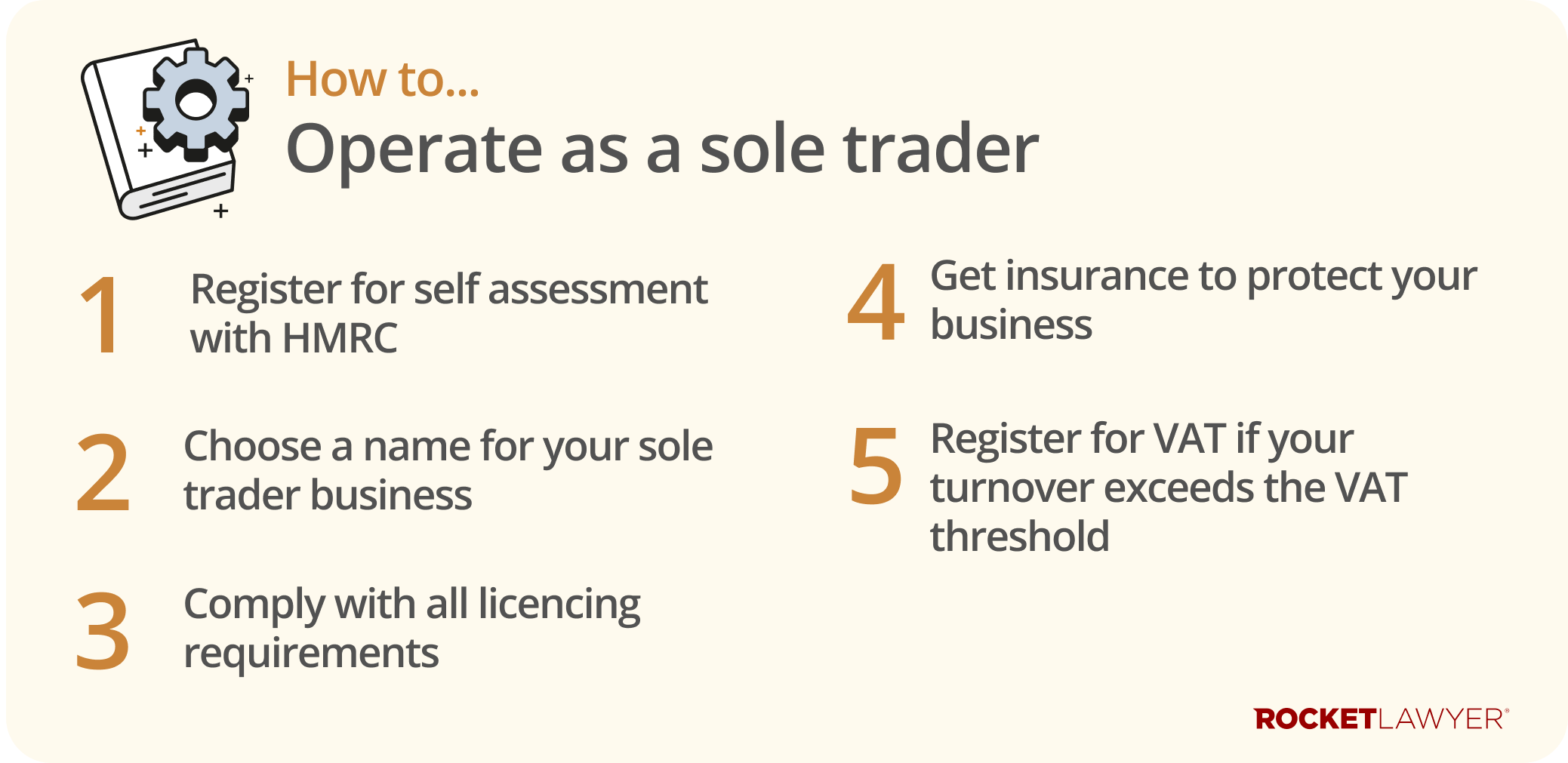

Setting up as a sole trader in the UK is quick and free. To become a sole trader, you’ll need to:

-

register with HMRC - if you earn more than £1,000, you must let HMRC know that you're self-employed by registering for Self Assessment

-

choose a business name - you can trade under your own name (eg ‘John Smith’) or a separate business name, known as a ‘trading name’ (eg ‘John Smith trading as Smith and Sons’). For more information, read How to choose a name for your business

-

ensure you comply with any applicable licensing requirements - some businesses, such as food services or taxi services, may need licences or permits

-

consider insurance - public liability insurance or professional indemnity insurance can protect you and your business

-

register for Value Added Tax (VAT), if required - if your turnover exceeds the VAT threshold (currently £90,000), you must register. If your turnover is below the VAT threshold, registration is optional

When do I have to register with HMRC?

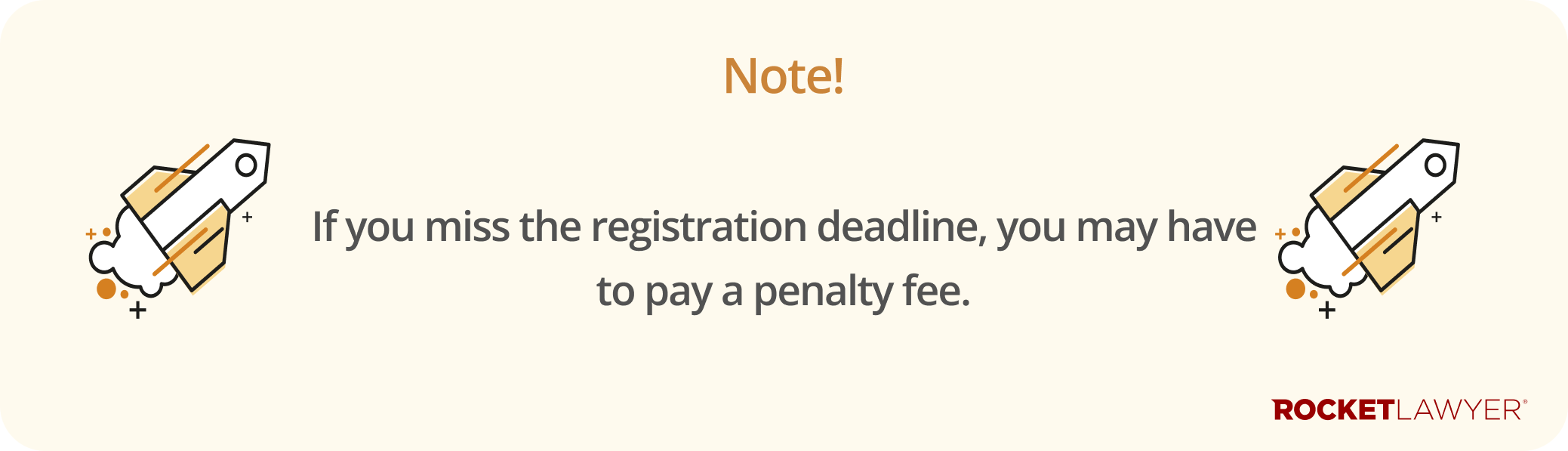

You must register as a sole trader with HMRC by 5 October following the end of the tax year in which you started trading. For example, if you begin work in June 2025, you must register by 5 October 2026.

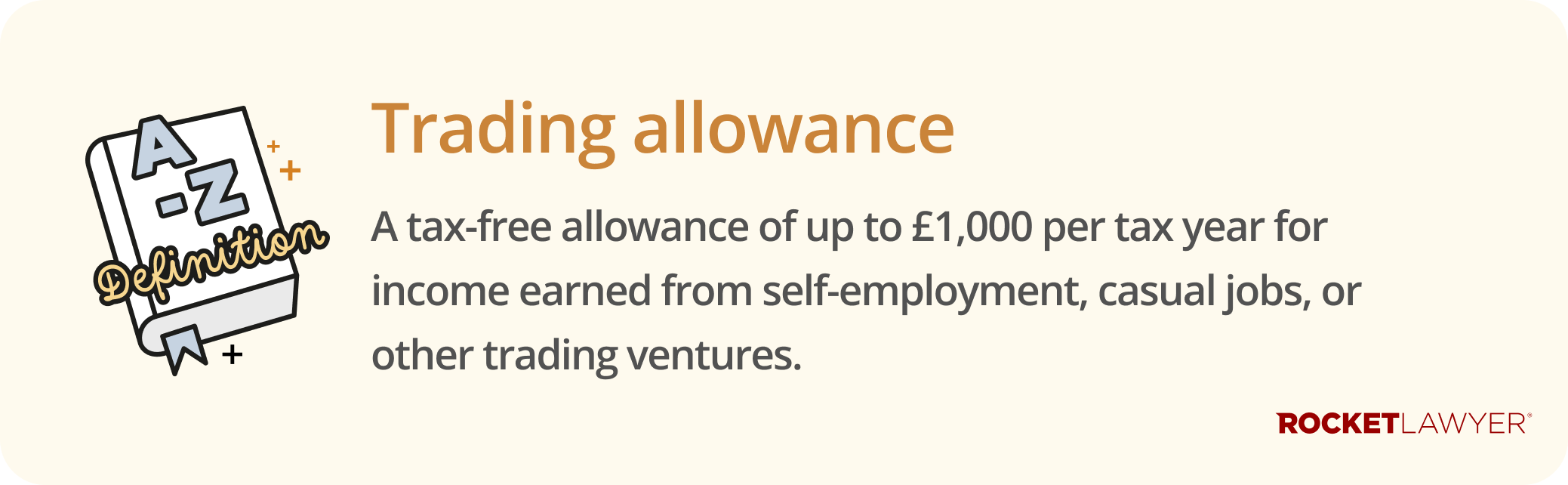

Do I need to register as a sole trader if I earn under £1,000?

You do not need to register with HMRC if your trading income is under £1,000 in a given tax year (ie under the £1,000 trading allowance). However, registering can be helpful for claiming expenses and building a business history.

What records will I need to keep as a sole trader?

As a sole trader, you're legally required to keep detailed records of your business finances. These records are essential for completing your Self Assessment tax return and proving your income and expenses to HMRC.

You must keep records of:

-

all income from sales or services

-

all business expenses, such as equipment, travel or office costs

-

receipts and invoices

-

bank statements for any business accounts

-

VAT records, if you're registered for VAT

-

PAYE records, if you employ anyone

For how long do I need to keep records?

You must keep your records for at least five years after the 31 January submission deadline for the relevant tax year. HMRC may conduct a compliance check on your tax return (ie a tax audit) and ask to see these records to ensure you are paying the correct amount of tax.

Using accounting software or hiring a bookkeeper can help you stay organised and compliant.

What taxes do sole traders pay?

As a sole trader, you're responsible for calculating and paying the correct amount of tax on your profits. You’ll typically need to pay:

-

income tax - based on your business profits after allowable expenses

-

National Insurance contributions (NICs) - Class 2 and Class 4 NICs apply depending on your earnings

-

VAT - if your annual turnover exceeds the VAT registration threshold

For more information on submitting your tax return, read Personal tax.

What are the pros and cons of being a sole trader?

Setting up as a sole trader is a popular choice for people starting a business in the UK. While it's quick and easy to get going, it’s important to understand how this structure could affect your responsibilities and liabilities.

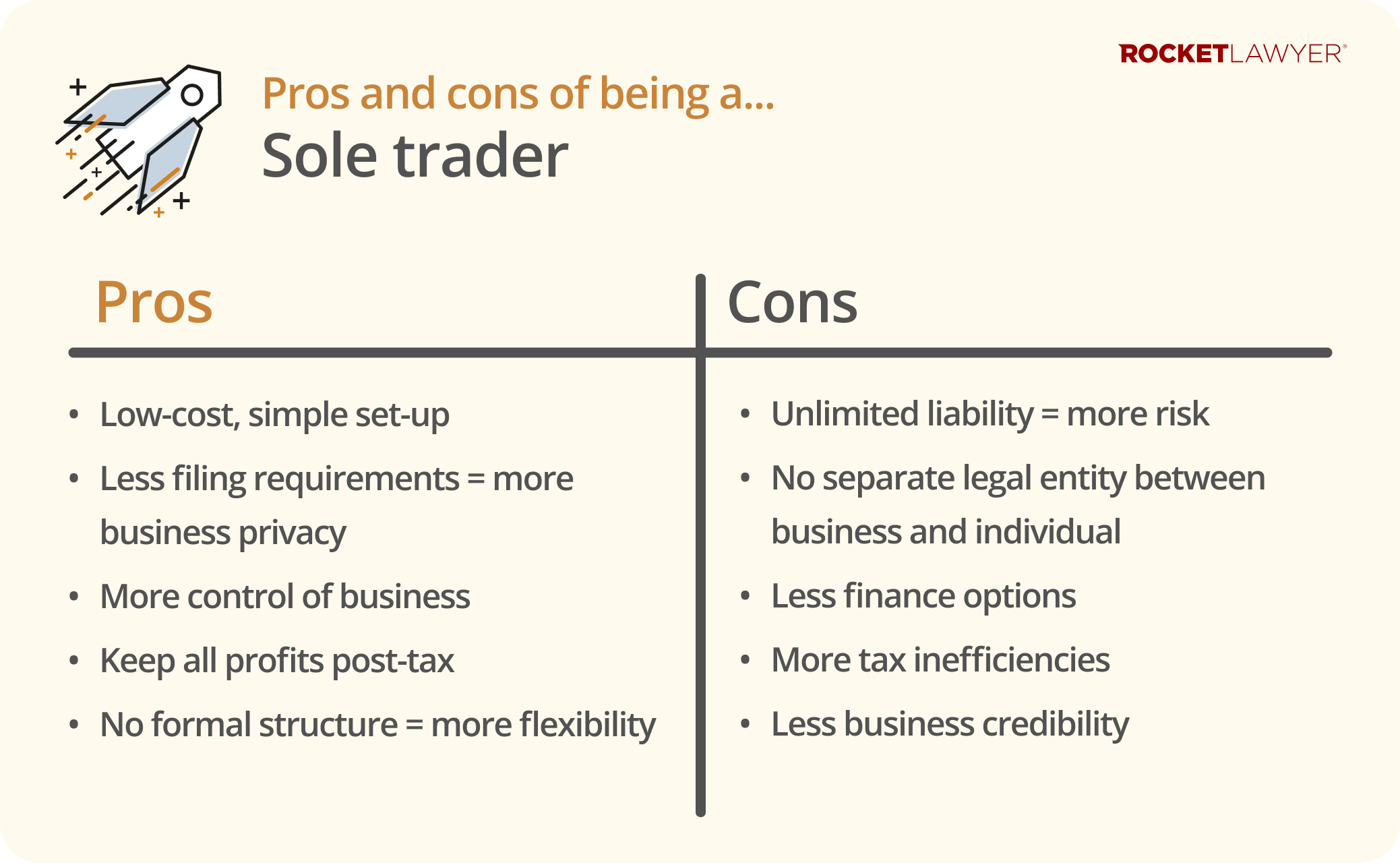

Pros of being a sole trader

There are several benefits to operating as a sole trader, including:

-

simple setup - registering with HMRC is free and can be done online in minutes

-

fewer reporting requirements - compared to limited companies there’s less admin and no need to file accounts with Companies House, which means more privacy for your business

-

full control - you make all the decisions about how the business is run

-

keep all profits - after tax, any money the business makes is yours to keep

-

flexible working - you choose when and how you work, and can easily scale up or down

Cons of being a sole trader

There are also some risks and limitations to be aware of:

-

unlimited liability - you’re personally responsible for any debts the business incurs

-

harder to raise finance - some lenders and investors prefer working with limited companies

-

tax planning limitations - you may pay more tax as your profits increase, compared to a limited company

-

less business credibility - some clients or suppliers may view limited companies as more professional

If you’re planning to grow your business or take on significant financial commitments, it may be worth considering whether a different business structure could be more suitable in the long term.

What documents do I need as a sole trader?

Running a business on your own doesn’t mean doing everything without support. Having the right legal documents in place can help protect your interests, manage risk, and present a professional image. Documents you may find useful as a sole trader include:

-

Consultancy agreement - formalises your work with clients, setting clear terms for services, payments, and intellectual property

-

Office sharing agreement - allows you to share workspace with another business, setting out fees and usage terms

-

Terms and conditions - set customer expectations and help limit your liability, with versions for consumers and business clients

-

Website terms and Privacy policy - help you stay compliant with online regulations and data protection laws

-

Non-disclosure agreements (NDAs) - protect sensitive information when sharing ideas with clients, partners, or suppliers

-

Employment contracts - outline duties, rights and pay if you decide to hire staff

Having clear, written agreements helps avoid misunderstandings and provides peace of mind if a dispute arises later in the business lifecycle.

Getting started as a sole trader is just the beginning. To build a strong foundation, consider making a Business plan to guide your strategy. Anyone still weighing their options should read Choosing your business structure and Running a business to find out more about the different business structures and what they entail. If you have any questions or concerns, do not hesitate to Ask a lawyer.