1. What do I have to tell HMRC about my new business?

Precisely what (and when) you have to tell HMRC about your new business depends on your business structure:

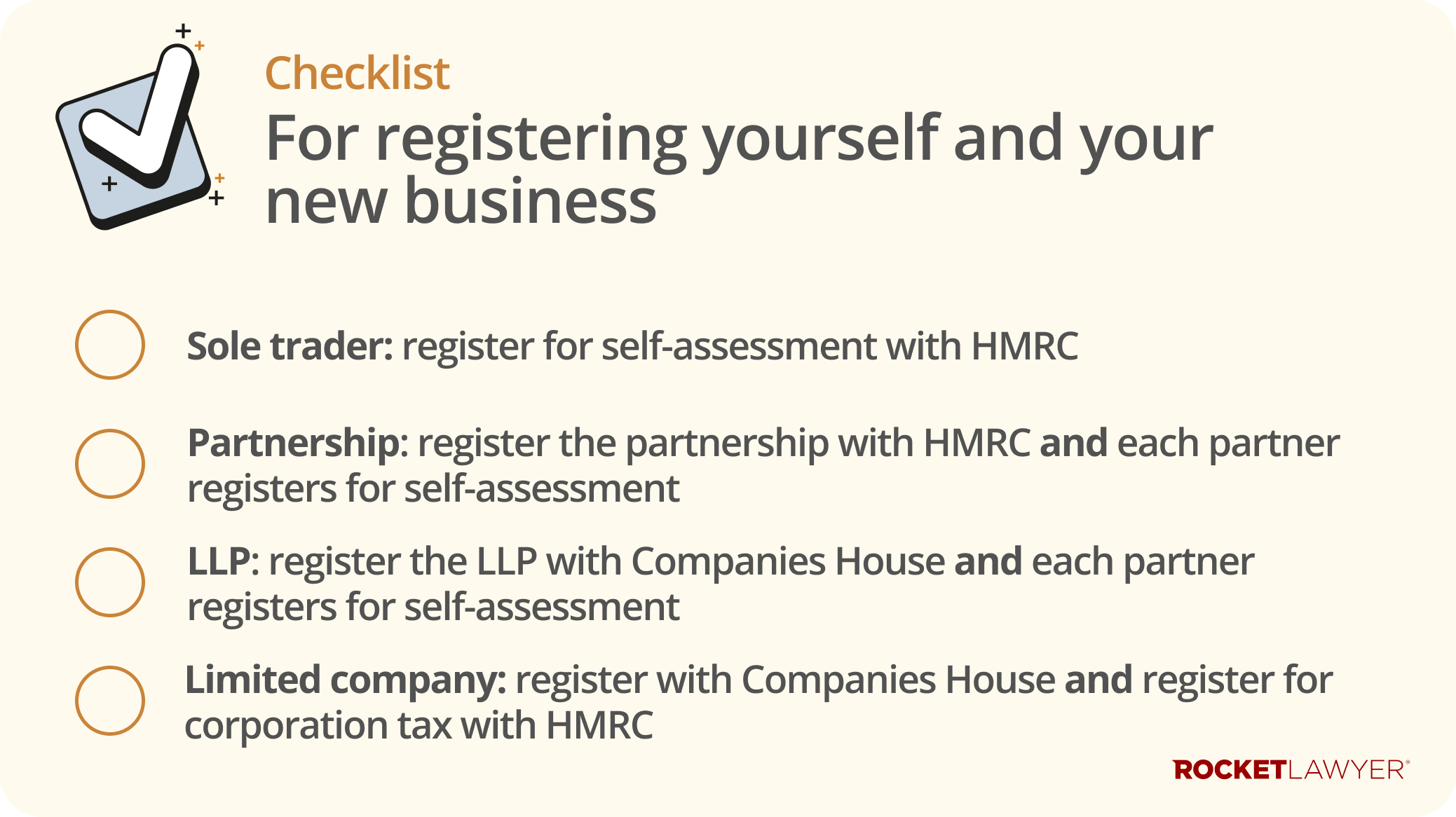

Sole traders

If you conduct business as a sole trader (either under your own name or under a trading name), you need to register for self-assessment. Registering as a sole trader is simple, as you merely need to tell HMRC that you are operating as a sole trader and provide your details.

Partnerships and LLPs

If you are running a partnership, it must be registered with HMRC. You will need to provide certain information to HMRC, including:

-

the partnership name

-

the details of the nominated partner (ie the person responsible for filing the partnership tax return and looking after the partnership’s records)

-

information about the nature of the business

-

the partnership’s address

-

the details of each partner

If you are running a limited liability partnership (LLP), it must be registered with Companies House. You will need to provide certain information to Companies House, including, but not limited to, the LLP’s:

-

name

-

registered address

-

other partners (also known as ‘members’)

In both situations, each partner must also register with HMRC for self-assessment.

Private limited companies

If you are running a private limited company, it must be registered with Companies House. You will need to provide certain information to Companies House, including, but not limited to, the company’s:

-

name

-

registered address

-

initial director(s)

-

initial share issue

-

shareholder details

-

business activity

If you’re not registered for corporation tax when you register with Companies House, you’ll also have to separately register your company with HMRC.

For more information, read Choosing your business structure and Running your business.

2. What taxes does my business have to pay?

Businesses have to pay an annual tax on taxable income or profits. What tax depends on your business structure. If your business is:

-

conducted as a sole trader, you, as the sole trader, will have to pay income tax on your taxable income

-

a partnership or LLP, all partners will have to pay income tax on their taxable income. The partnership itself does not have to pay any tax

-

a company, the company itself will have to pay corporation tax on its taxable profits. Company owners (ie shareholders) will have to pay income tax on their taxable income (eg income from shares)

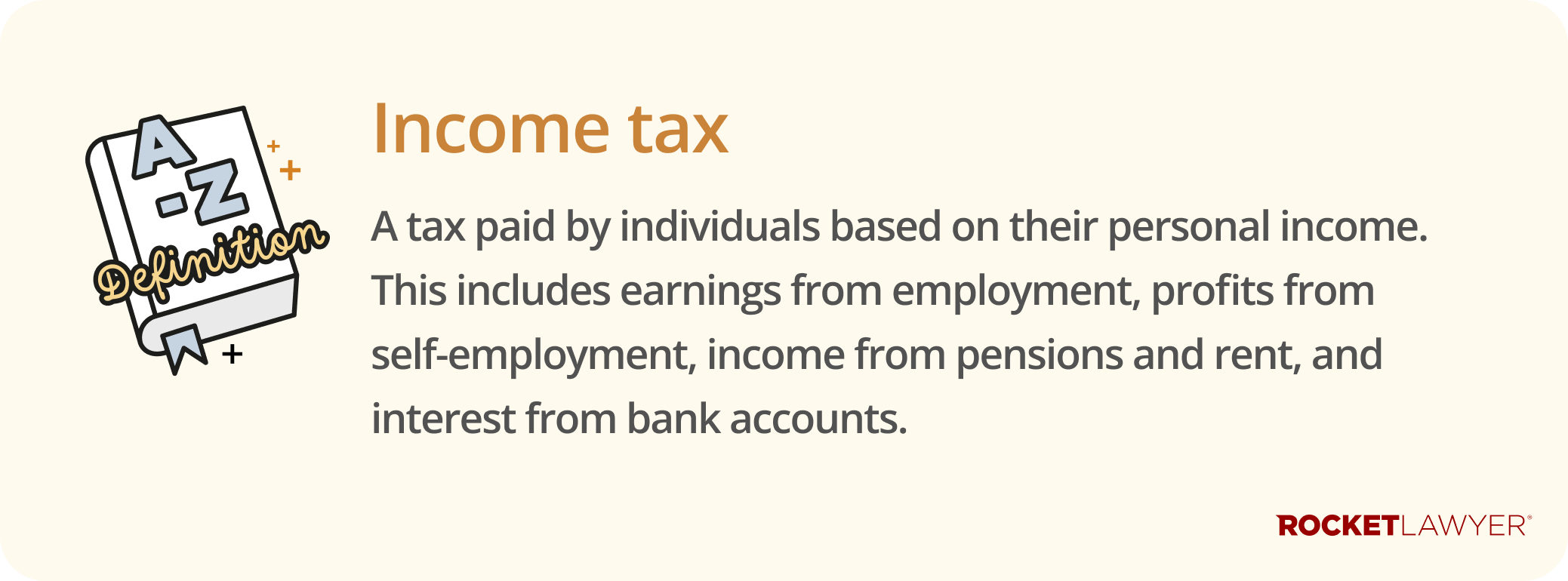

What is income tax?

Income tax is a tax that individuals pay on their earnings. This includes, but is not limited to:

-

income from employment

-

income from self-employment

-

certain rental income

-

income from trusts

For more information, including current income tax rates, read Income tax in England and Wales and Income tax in Scotland.

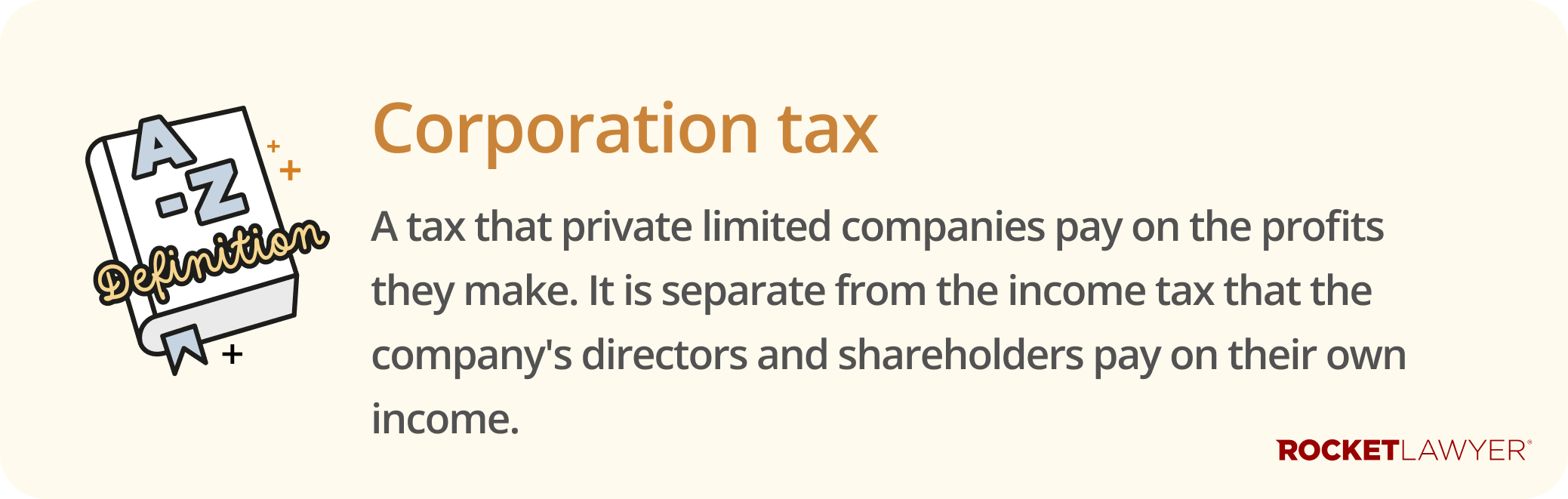

What is corporation tax?

Corporation tax is a tax paid by private limited companies (and certain other businesses, like co-operatives) on the company’s taxable profits. These include trading profits and chargeable gains.

When corporation tax must be paid depends on the value of taxable profits. For taxable profits of up to £1.5 million, the payment deadline is nine months and one day from the end of the company’s accounting period.

The end of the accounting period is determined based on the company’s accounting reference date (ARD). This is issued on registration by Companies House. It is the date you’ll prepare your annual accounts and is usually the last day of the month in which you registered your company. For example, if you registered your company on 11 November, your ARD would be 30 November.

For more information on corporation tax, including current tax rates, read Corporation tax. For more information on accounting reference dates and accounting periods, see Companies House’s accounts guidance.

3. What are tax returns?

Tax returns are used by HMRC to collect relevant taxes from individuals and businesses. The type of tax return your business needs depends on your business’s structure.

What is a self-assessment tax return?

A self-assessment tax return is the system HMRC uses to collect income tax. While income tax from employment and pensions is generally deducted automatically, anyone with other income sources must report it independently. This is what self-assessment tax returns are used for.

A self-assessment tax return must be completed after the tax year it covers. The tax year runs from 6 April to 5 April the following year.

Self-assessment tax returns must be submitted by midnight on 31 October (for paper returns) or by midnight on 31 January (for online returns). The deadline for paying any income tax owed is midnight on 31 January. There are fines for late filings of self-assessment tax returns.

For more information, see the government’s guidance on self-assessment tax returns.

What is a partnership tax return?

A partnership tax return is a document that declares the income (or losses) of a partnership or LLP. It details the partnership’s or LLP’s income and how it is distributed amongst the partners.

The deadlines for filing a partnership tax return are the same as for a self-assessment tax return. There are fines for late filings of partnership tax returns.

For more information, see the government’s partnership tax return guide notes.

What is a company tax return?

A company tax return sets out a company’s profits, losses, loans, and other factors relevant to its tax liability.

Your company must submit a tax return, together with supporting annual accounts, each year using form CT600. This must be done even if the company doesn’t have to pay corporation tax. As part of the company tax return, you have to work out the company’s profit or loss for corporation tax and the corporation tax bill.

Company tax returns can be submitted up to 12 months after the end of the accounting period they cover. There are fines for late or inaccurate filings of company tax returns.

For more information, read Annual accounts and tax returns.

4. What other taxes should I know about?

National insurance and income tax (especially if you’re running a company) are other taxes to be aware of as a new business.

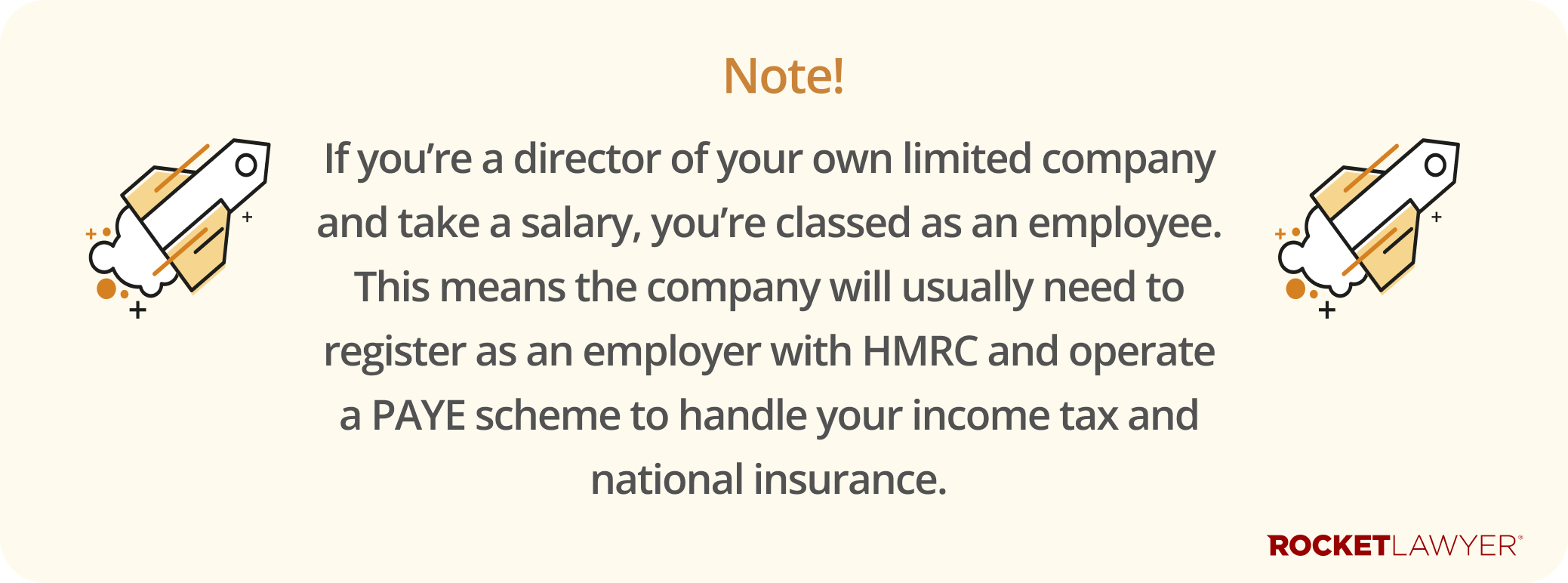

Employers and employees (including directors) have to pay national insurance. National insurance is a deduction from earnings, originally set up to fund various state benefits such as the state pension, maternity allowance, and jobseeker’s allowance.

In addition, all employees must pay income tax. In most cases, income tax is taken directly from employees’ salaries using a scheme operated by HMRC called Pay As You Earn (PAYE). If your business has at least one employee (including if you draw a salary from your company for yourself) who qualifies for PAYE, you must operate and make deductions for PAYE.

For more information on PAYE (including when it isn’t applicable) and national insurance, read Personal tax and National Insurance contributions.

Do not hesitate to Ask a lawyer if you have any questions or concerns about starting your business or meeting your tax obligations. You can also use our Business legal health check to make sure your business is set up correctly and staying on top of its legal and tax obligations.