What is income tax?

Income tax is a mandatory payment to the government based on your annual earnings. It is one of the UK's primary sources of funding for public services like the NHS, schools, and infrastructure. Unlike some other taxes, it's personal to you, and the amount you owe is calculated based on your total income from various sources during the tax year.

Who pays income tax?

Most individuals who earn more than their personal allowance (more on this below) must pay income tax. This includes:

-

individuals

-

partnerships - partners are individually responsible for the tax due on their shares of partnership profits

-

personal representatives - these are individuals who manage administration of the estate of someone who has died. They often need to pay the deceased's outstanding income tax during the administration of the estate

-

trustees (ie those who hold property on trust for others) - they will be responsible for paying income tax on the income produced by a trust’s assets

You don't usually pay income tax if your total taxable income is below the standard personal allowance.

Companies pay corporation tax rather than income tax.

What is the tax year?

The UK tax year is the 12-month period used to calculate your income and the tax you owe. Unlike the calendar year, it doesn't run from January to December. Instead, it runs from 6 April until the following 5 April.

The 2026/27 tax year starts on 6 April 2026 and ends on 5 April 2027.

For more information, read What calendars should businesses be aware of?

What are the tax bands?

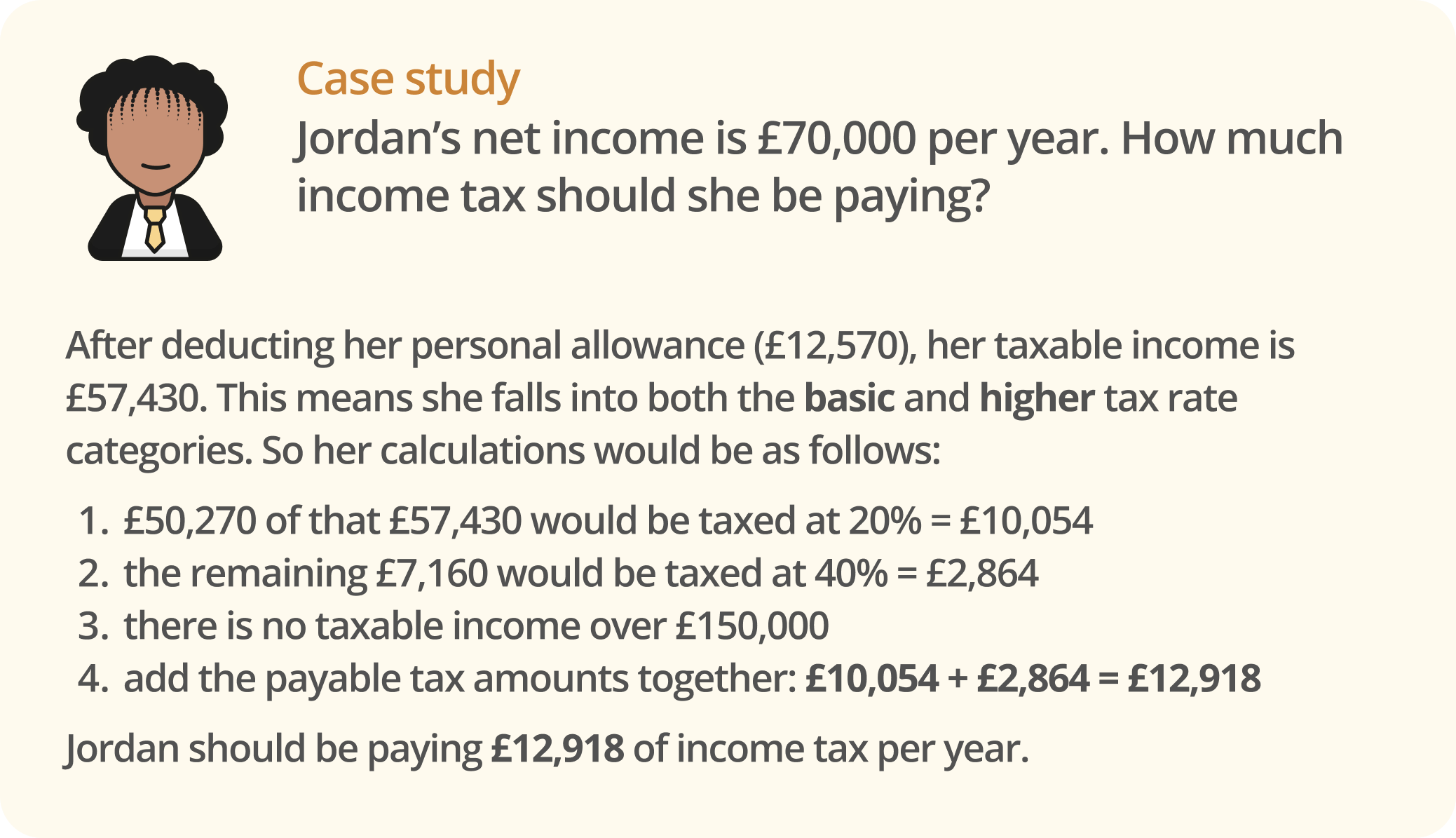

Tax bands determine the percentage of tax you pay on different ‘slices’ of your income. As your income increases and moves into a higher band, you only pay the higher rate on the portion of money that falls within that specific bracket.

For the 2026/27 tax year, the bands for taxable income (after deducting your personal allowance) are:

-

basic rate - 20% on income between £12,571 and £50,270

-

higher rate - 40% on income between £50,271 and £125,140

-

additional rate - 45% on income over £125,140

What is the personal allowance?

The personal allowance is the amount of income you can earn each year without paying any income tax. For the 2026/27 tax year, the standard personal allowance is £12,570. If you earn less than this, you usually won't pay any income tax at all.

Your allowance is higher if you claim Blind Person’s Allowance.

If you earn over £100,000, your personal allowance gradually reduces. It decreases by £1 for every £2 that your adjusted net income exceeds £100,000. This means your allowance is zero if you earn £125,140 or more per year.

How much income tax do I pay?

When calculating income tax, you will need to work through the following steps:

1. Calculate your total income

Add together all of your before-tax taxable income.

What is taxable income?

Taxable income is any type of income you pay tax on. It includes, but is not limited to:

-

money you earn from employment (including bonuses and commissions)

-

profits you make if you are self-employed (ie from goods or services that you sell)

-

taxable state benefits

-

income from renting out property

-

pensions (including most state and company pensions)

-

interest from bank and building society accounts

What does not constitute taxable income?

Certain types of income are not taxable and can, therefore, be ignored for tax purposes. Some types of income are only taxable once they’re over a certain threshold. You usually do not have to tell HMRC about income that is not taxable. Income that is not taxable includes, but is not limited to:

-

income from tax-exempt accounts, like Individual Savings Accounts (ISAs)

-

income from dividends from company shares that’s under the dividend allowance (£500 for the 2026/27 tax year)

-

the first £1,000 of income from self-employment (ie the trading allowance)

-

premium bonds or National Lottery wins

- rent you receive from a lodger that is below the rent a room threshold (currently £7,500)

For more information on which income is and isn’t taxable, see the government’s guidance on income tax. If you're unsure as to whether income is taxable or not, you can Ask a lawyer for assistance.

2. Deduct any allowable tax relief

Check whether you can claim tax relief for any payments made during the year. Allowable reliefs remove sums of money from the income tax calculation and apply to:

-

pension contributions - you can get tax relief on private pension contributions if certain conditions are met

-

charity donations - donations to charity from individuals are often tax-free (ie if they are made using Gift Aid)

-

maintenance payments - the Maintenance Payments Relief reduces your income tax if you make maintenance payments to an ex-spouse or civil partner

-

work expenses - you can claim tax relief if you are employed and use your own money for travel or things you have to buy for your job. If you are self-employed (ie if you are a sole trader or a partner in a partnership), you can get tax relief on what you spend running your business

Different types of tax relief are applied in different ways. Some tax reliefs reduce your overall tax bill by a certain amount. Others affect the amount of income that you pay tax on.

For more information, see the government’s guidance on income tax reliefs.

3. Deduct any personal tax allowances

Once you’ve worked out your total taxable income, subtract your personal allowance from that figure. This leaves you with your ‘taxable income’, which is the actual amount you'll be taxed on.

As noted above, the standard personal allowance for the 2026/27 tax year is £12,570. If your income is over £100,000, remember to reduce this allowance according to the rules mentioned above.

4. Calculate the tax

Apply the relevant tax rates to your remaining taxable income. Remember that you only pay the higher rates on the portion of your income that falls within those specific bands.

For the 2026/27 tax year, you'll calculate your tax as follows:

-

20% on the portion of income between £12,571 and £50,270

-

40% on the portion of income between £50,271 and £125,140

-

45% on any income over £125,140

Note that your rates and calculations will be different if your personal allowance is reduced. You may also have to fill in a Self Assessment tax return. For more information, see the government’s guidance on personal allowances and higher rates of income.

Estimate your income tax for the current year using the government's income tax calculator.