What is a private limited company?

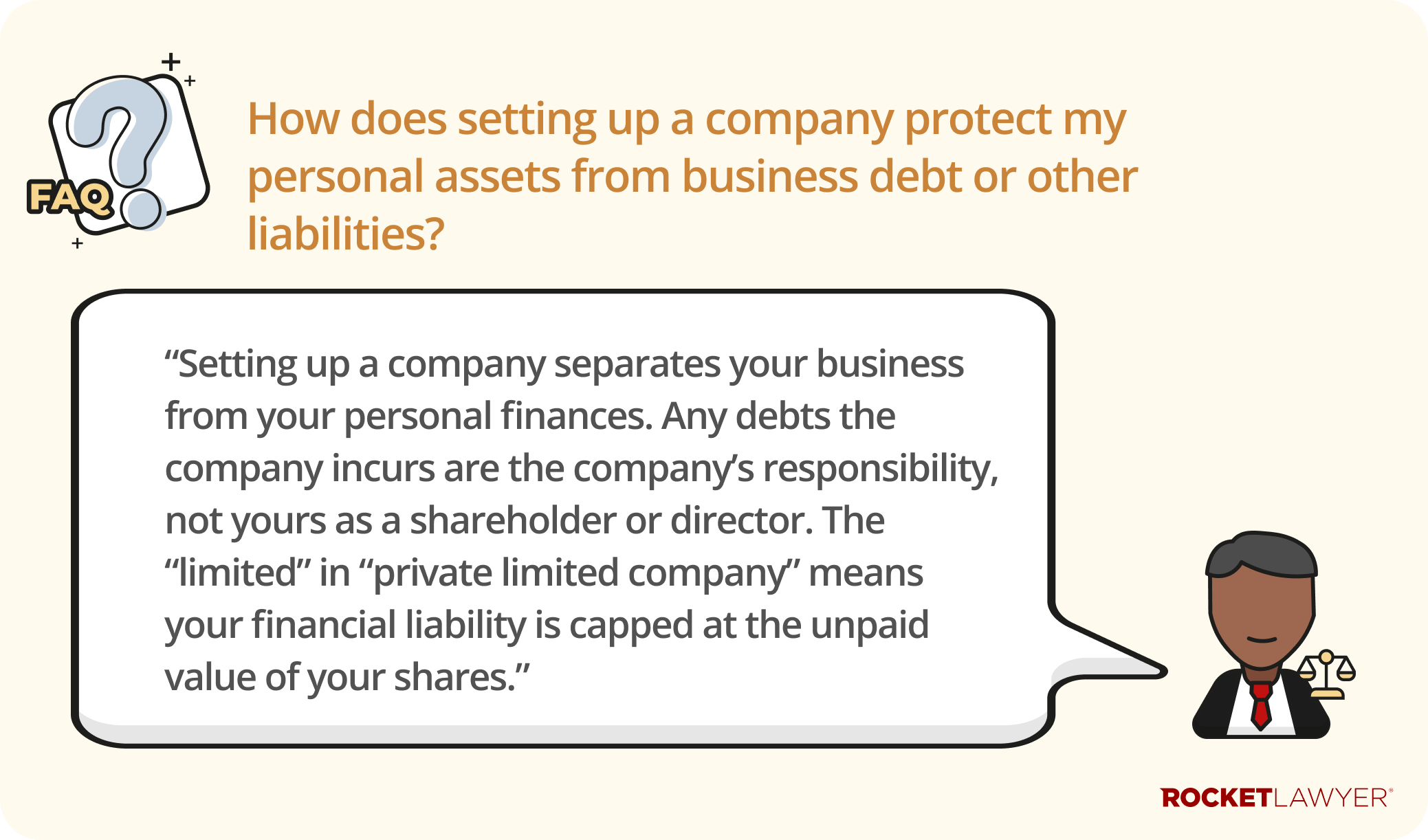

A private limited company (often abbreviated as 'LTD') is a type of business structure where the company is legally distinct from the people who run it and own it. Because an LTD is a separate legal entity from its owners, its finances are distinct from those of its owners, and its owners are not liable for (all of) the company’s debts. Further, an LTD’s shares are not sold to the public.

There are two main types of private limited companies: those limited by shares and those limited by guarantee.

What is a private company limited by shares?

This is the most common type of company for businesses that trade to make a profit. It is owned by shareholders (or ‘members’) and run by directors. The company is divided into shares, and the shareholders are entitled to the profits (usually paid as dividends).

What is a private company limited by guarantee?

This structure is typically used by non-profit organisations, charities, clubs, and student unions. It does not have shares or shareholders. Instead, it has guarantors (or ‘members’) and a guaranteed amount. Any profit made is usually reinvested back into the organisation rather than distributed to members.

For more information on setting up a private limited company, read How to register a company in five steps.

What is limited liability?

Limited liability is a form of legal protection for shareholders, ensuring they are not personally liable for the company's debts beyond a certain amount.

The basis of a limited liability company is that all debts incurred by the company are the company's liabilities and are not directly the legal liabilities of the company's shareholders.

The way this protection works depends on whether the company is limited by shares or by guarantee.

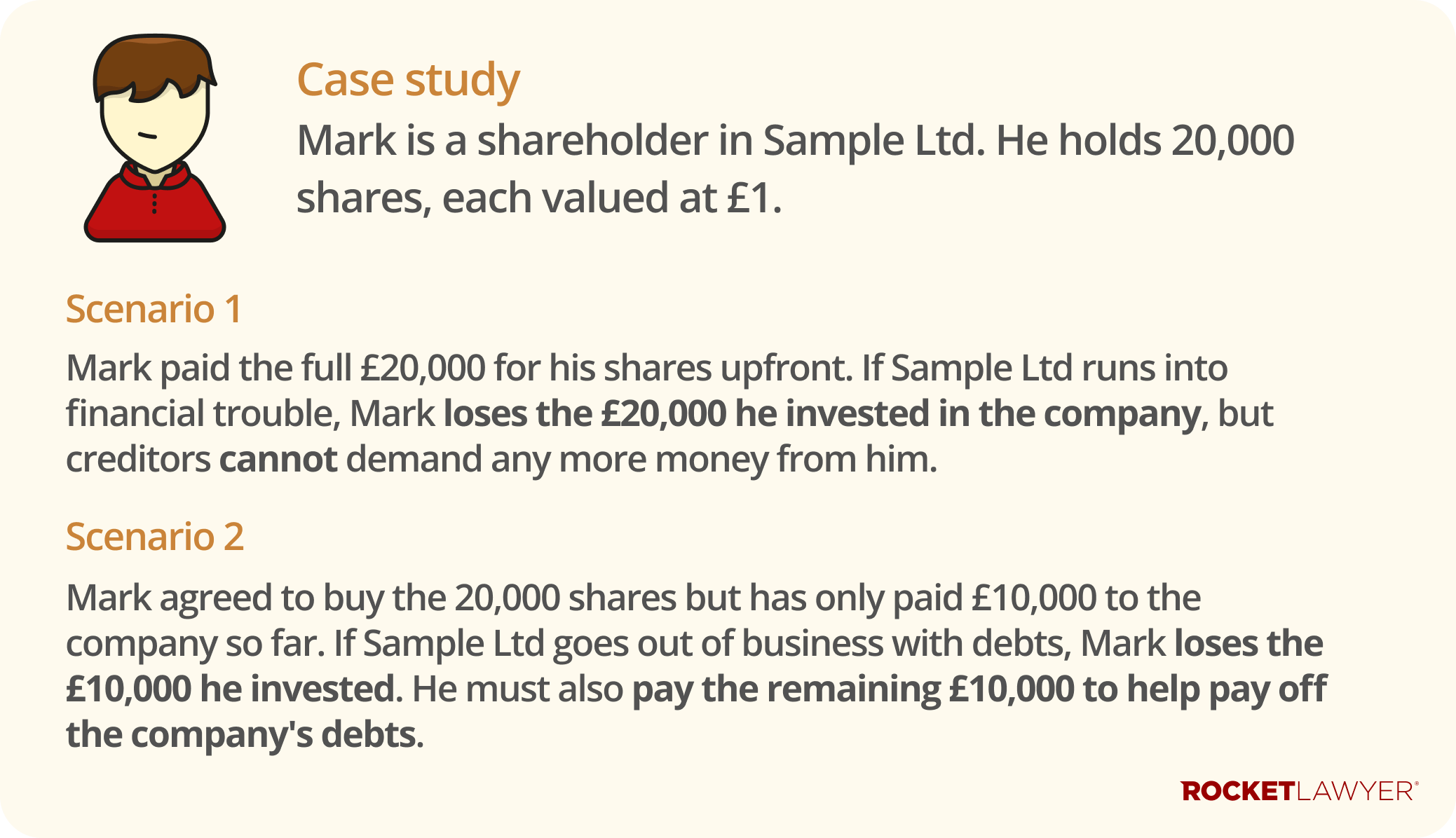

Liability in a company limited by shares

If a company is limited by shares, a shareholder's liability is limited to the amount of their investment in the company. In practice, this means the amount unpaid on shares they hold (if any).

There are two main scenarios for shares:

-

fully paid shares - in most small companies, shareholders pay for their shares in full when they are issued (eg paying £1 for one share). If the shares are fully paid, the shareholder has no further financial obligation. Their liability is simply that they lose the money they originally invested if the company fails

-

unpaid shares - if a shareholder has been issued shares but has not yet paid the company for them, they are legally liable to pay that specific amount if the company is closed

For a comparison of these risks against other business structures, read Are sole traders personally liable for debts?

Liability in a company limited by guarantee

If a company is limited by guarantee, the members do not hold shares. Instead, they provide a guarantee to contribute a specific amount to the company's assets if it closes. Key aspects of this guarantee include:

-

the guarantee amount - this is usually a nominal sum (eg £1 or £10) set out in the company's articles of association

-

when it is paid - unlike shareholders, who often pay for their shares upfront, members of a company limited by guarantee generally do not make a financial contribution while the company is operating. They only pay if the company goes out of business and cannot pay its debts

What are the shareholders' and directors' responsibilities?

Shareholders own the company. Their primary powers include voting on key decisions (such as changing the company name or appointing directors) and receiving dividends.

Directors are responsible for managing the company and ensuring it complies with its legal obligations. Even if you hire an accountant, the directors are legally responsible for the company's records and filings.

For more information on the different roles within a company, read Company appointments.

Are directors personally liable for company debts?

Generally, directors do not incur personal liability for the company's debts. Because all acts are undertaken as agents for the company, the debts are considered the company's liabilities.

However, liability may be imposed on directors in the event of wrongful or fraudulent trading (ie allowing a company to trade when it cannot pay its debts).

For more information, read Directors' duties, Different types of company directors, or Ask a lawyer about personal liability.

Reporting and filing requirements for LTDs

Private limited companies must file various documents with Companies House and HMRC every year to remain compliant. Failure to file on time can lead to penalties and even the company being struck off the register.

Annual accounts

Every company must prepare and file annual accounts, even if the company is dormant (ie not trading). These accounts provide an overview of the company's financial performance. For more information, read Annual accounts and tax return.

Confirmation statement

You must file a confirmation statement at least once a year. This confirms that the information Companies House holds about your company (such as directors, registered office, and shareholders) is correct. You must also confirm that the company's intended future activities are lawful. For more information, read Filing your confirmation statement.

Register of people with significant control (PSC)

You must identify and register anyone who exercises significant control over your company (usually anyone holding more than 25% of shares or voting rights). For more information on PSCs, read Company appointments.

Company statutory books

Companies are required to keep certain records, known as statutory books. These include registers of members and directors. While some registers (like the register of directors) are now held centrally by Companies House, you must still maintain your register of members and other internal records. For more information, read Company books and records.

Event-driven notices

There are certain other 'event-driven notices' that have to be submitted to Companies House to update their records. For example, if a company changes its address or appoints a new director, Companies House must be informed. For more information, read Important Companies House filings.

Corporation tax and VAT

Your company must pay corporation tax on its profits. You must register for corporation tax within three months of starting to trade. You may also need to register for VAT if your taxable turnover exceeds the VAT threshold. For more information, read Corporation tax and VAT.

Managing your finances

Running a company involves distinct financial responsibilities separate from your personal funds.

PAYE and payroll

If you employ staff, including yourself as a director, you will likely need to set up a PAYE (Pay As You Earn) payroll scheme to deduct income tax and National Insurance. For more information, read Checklist for new employers.

Self Assessment

Shareholders and directors often need to file a personal Self Assessment tax return, especially if they receive income that is not taxed through PAYE, such as dividends. For more information, read Personal tax.

For more information on other business structures, read Choosing your business structure. If you are ready to incorporate, consider using our free Company registration service. Do not hesitate to Ask a lawyer if you have any questions or concerns.