What are partnerships?

A partnership is legally defined as the relationship between two or more partners carrying out a business with a view to making a profit. This definition is set out in the Partnership Act 1890.

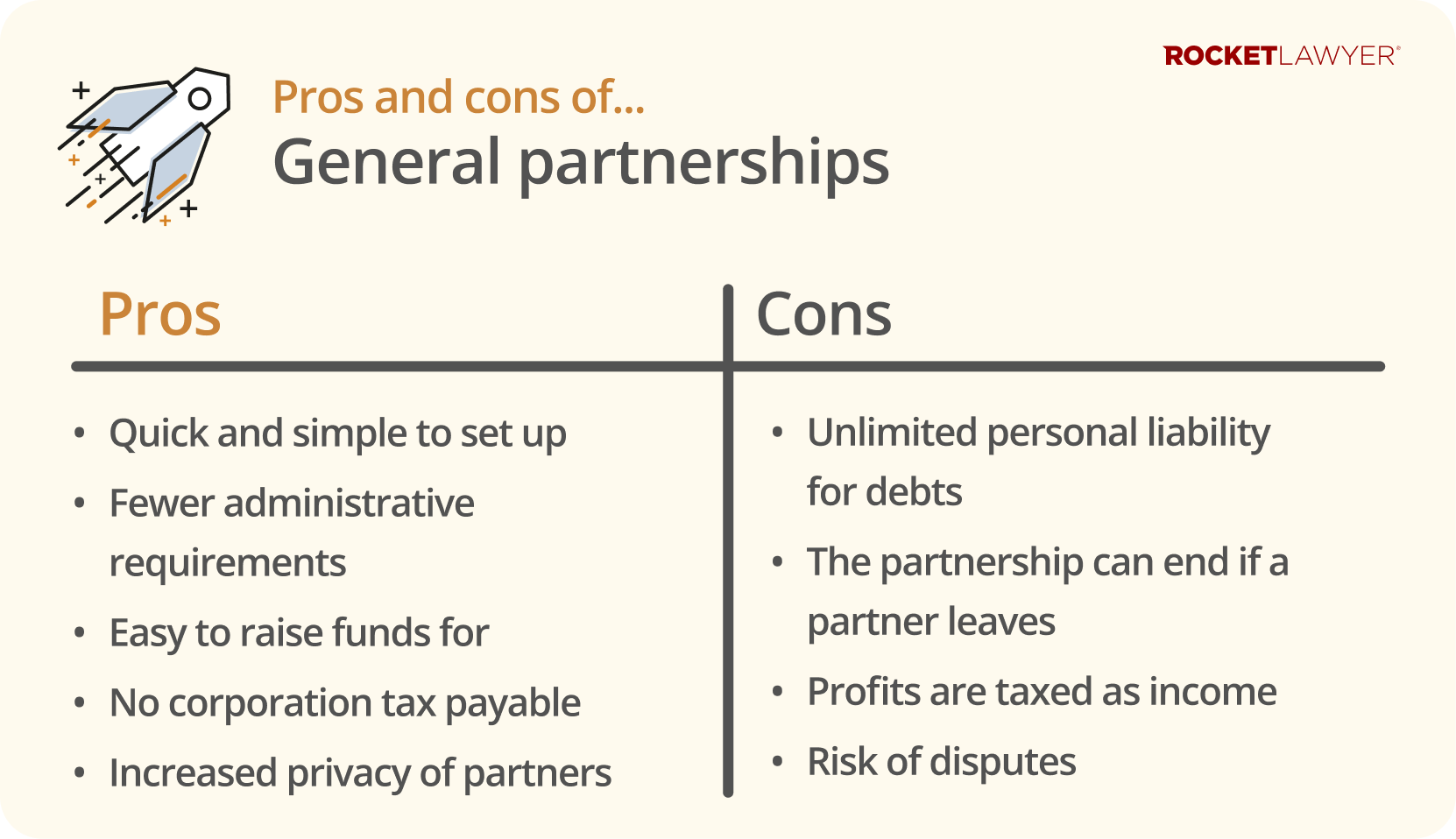

The most common type is a general partnership. In this simple structure, the business and its partners are treated as one entity, meaning there is no separate legal protection. All partners typically share in decision-making and profits. While you don't need to register a general partnership with Companies House, each partner must register with HMRC for tax.

However, the key feature of a general partnership is that partners are personally responsible for all the business's debts. This is known as ‘joint and several liability’. Other structures, such as limited partnerships (LPs) and limited liability partnerships (LLPs), exist to provide partners with greater financial protection. For more details, read Types of partnerships.

Who can be a partner in a partnership?

A partner has to be a legal person. This means that a partner can be:

-

an individual (aged 18 or over), or

-

a company or another business (acting as a corporate partner) that is considered by the law to be a separate legal entity

Partnerships must have at least two partners, but there’s no upper limit. However, each partner must agree to share in the business's profits and responsibilities.

The type of partnership you choose will also determine your liability. For example, in a general partnership, all partners are personally liable for debts, whereas in an LLP, partners’ liability is limited. Read Types of partnerships to find out more.

Core features of partnerships in the UK

While partnerships are flexible, they are defined by a few core legal concepts that govern how partners must act and what they are responsible for.

Ownership and control

In a partnership, the business is owned and controlled directly by the partners. Unlike a limited company, where directors manage the business on behalf of shareholders, partners are typically involved in both ownership and day-to-day management. Defining each partner’s ownership stake (eg 50/50, 60/40) and their specific decision-making powers is fundamental to avoiding future disputes.

The partnership agreement

Although not always legally required to start a partnership, a written Partnership agreement is the single most important document for your business. It is a binding contract setting out the rules on everything from profit sharing to decision-making. Without one, your business will be governed by the default rules of the Partnership Act 1890, which can lead to unwanted results like equal profit sharing regardless of each partner's contribution.

Fiduciary duties

A fiduciary duty is a legal responsibility of trust and good faith that all partners owe to each other and the partnership. This duty, which applies even without a written agreement, requires every partner to act honestly, avoid conflicts of interest, and never put their personal interests ahead of the business's.

Sharing profits and losses

A primary function of a general partnership is to share its profits, but the law also requires the sharing of any losses. The default rule under the Partnership Act 1890 is that all profits and losses must be shared equally among the partners. This applies regardless of the amount of time, effort, or capital each partner has invested. To create a more suitable arrangement, such as sharing profits based on contributions, partners must define their own specific terms within their Partnership agreement.

Joint and several liability

In most partnerships (excluding LLPs and LPs), partners are responsible for all business debts both jointly (as a group) and severally (as individuals). This means a creditor could pursue any single partner for the full amount of a business debt if the other partners are unable to pay. LLPs, LPs, and Scottish limited partnerships (SLPs) are specifically designed to limit this personal liability.

How are partnerships taxed?

A partnership does not pay tax as a separate business entity. Instead, its profits ‘pass through’ to the partners.

Each partner is then individually responsible for paying income tax (at the applicable rates in England and Wales or Scotland) and National Insurance on their share of the profits via their annual Self Assessment tax return.

While the partnership itself doesn't pay tax, the business must still file a separate partnership tax return with HMRC each year. Note that LLPs have additional responsibilities, including filing annual accounts with Companies House.

For more information on operating as a partnership, including how each type of partnership is taxed, read Running a partnership.

What are the advantages of a partnership?

The key advantages of a business partnership are its flexibility, simplicity, and lower setup costs compared to a company. This straightforward structure is a major reason why it remains a popular choice.

One of the most significant benefits is operational simplicity. Most partnerships have fewer administrative requirements, as there is no need to register with Companies House and file annual accounts. This not only saves time but also ensures the business’s financial details remain private and confidential.

A partnership is also an excellent structure for combining resources. It allows partners to pool their skills, experience, and capital to create a more dynamic business. Raising further investment can also be simpler, as bringing in a new partner is often more straightforward than issuing new shares in a company.

What are the key risks of a partnership?

The most significant disadvantage of a general partnership is the unlimited personal liability of the partners. Because the business is not a separate legal entity from its owners, you are personally responsible for all business debts. This means your personal assets could be at risk if the business is unable to pay its bills.

Another major risk is the lack of continuity. Under the Partnership Act 1890, if there is no agreement to the contrary, the partnership is automatically dissolved if a partner dies or chooses to leave. This can unexpectedly bring the entire business to a halt. You can learn more about this process in our guide to Ending and dissolving a partnership.

Finally, the potential for disputes between partners can seriously disrupt business operations. Disagreements over money, strategy, or responsibilities are common, and without a formal process for resolving them, they can escalate quickly.

These risks highlight why making a comprehensive Partnership agreement is the most critical step you can take to mitigate the potential downsides and protect all partners involved.

While a partnership offers a flexible and simple way to run a business with others, it comes with significant personal risks, especially regarding liability and disputes. The key to a successful partnership lies in establishing clear rules from the outset. Making a comprehensive Partnership agreement is the most critical step you can take to mitigate risks and protect all partners involved. If you have any questions about partnerships in the UK, Ask a lawyer.