What is a consultant?

A consultant (also referred to as a ‘contractor’ or ‘freelancer’) is a self-employed individual or a company that provides professional consultancy services or advice to a business on a specific project or for a set period. They might be working on a specific project or for a set amount of time.

Unlike employees, consultants are their own bosses. They're in control of their own workload, decide how and when they'll get the work done, and are responsible for handling their own tax and National Insurance.

They typically have specialised knowledge in areas like IT, marketing, or finance. Because they are external experts and not employees, they don’t have employment rights like statutory sick pay or paid holidays, which is a key difference in how you manage the relationship.

What's the difference between a consultant and an employee?

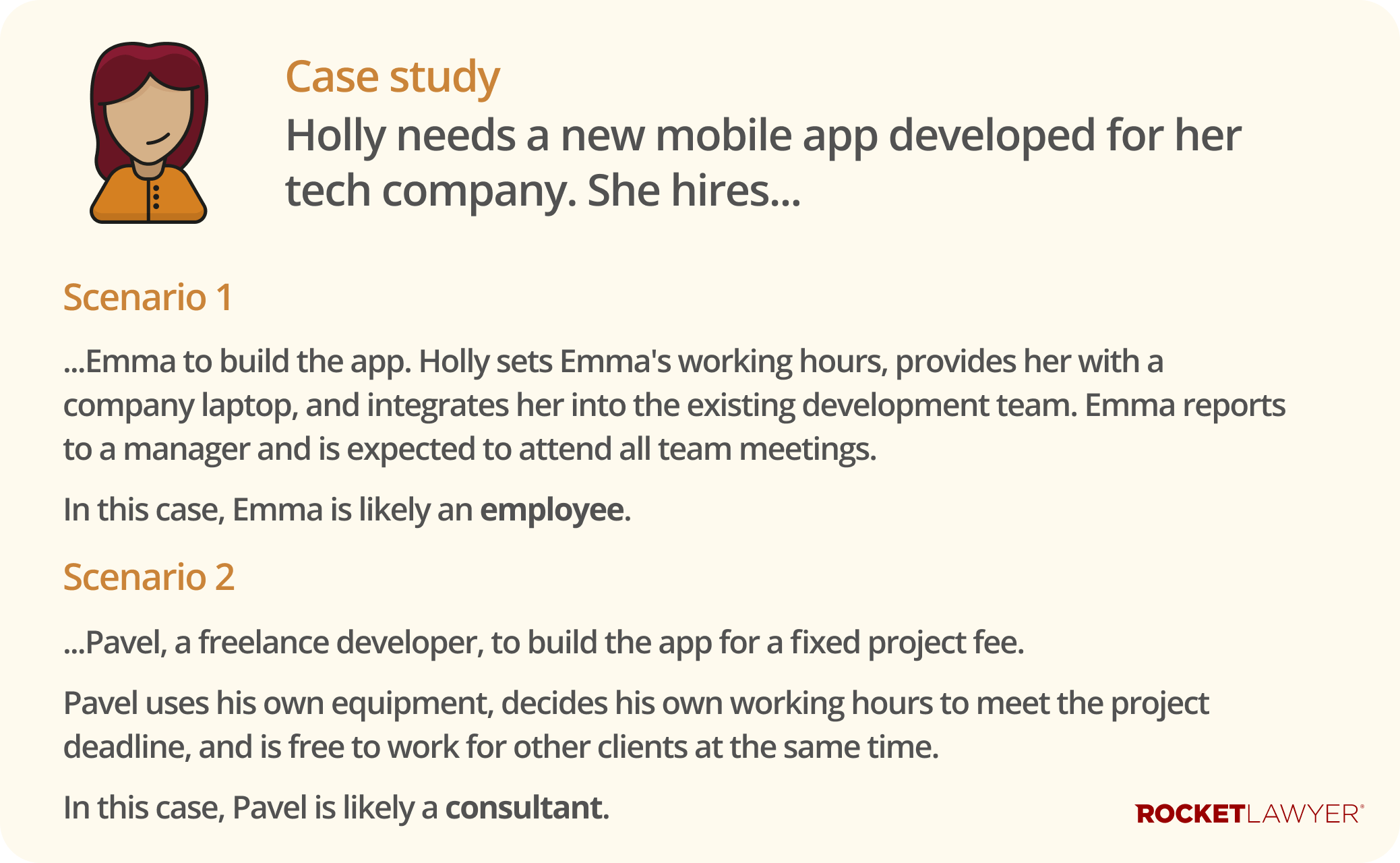

It’s crucial to understand the difference between a consultant and an employee, as misclassifying someone can lead to serious legal and financial problems. The distinction isn't just about what you call them or what's written in a contract; it's about the reality of the working relationship.

Key differences include:

-

control - you can direct what work an employee does and how they do it. For a consultant, you agree on the desired outcome, but they decide how to achieve it

-

substitution - a consultant can usually send a substitute to do the work if they're unavailable. An employee cannot

-

equipment - employees typically use equipment provided by the business, while consultants often use their own

-

financial risk - consultants bear their own financial risk. They're not paid for time off and must correct faulty work in their own time

-

exclusivity - consultants are free to work for multiple clients at the same time

For more information, read Consultants, workers, and employees.

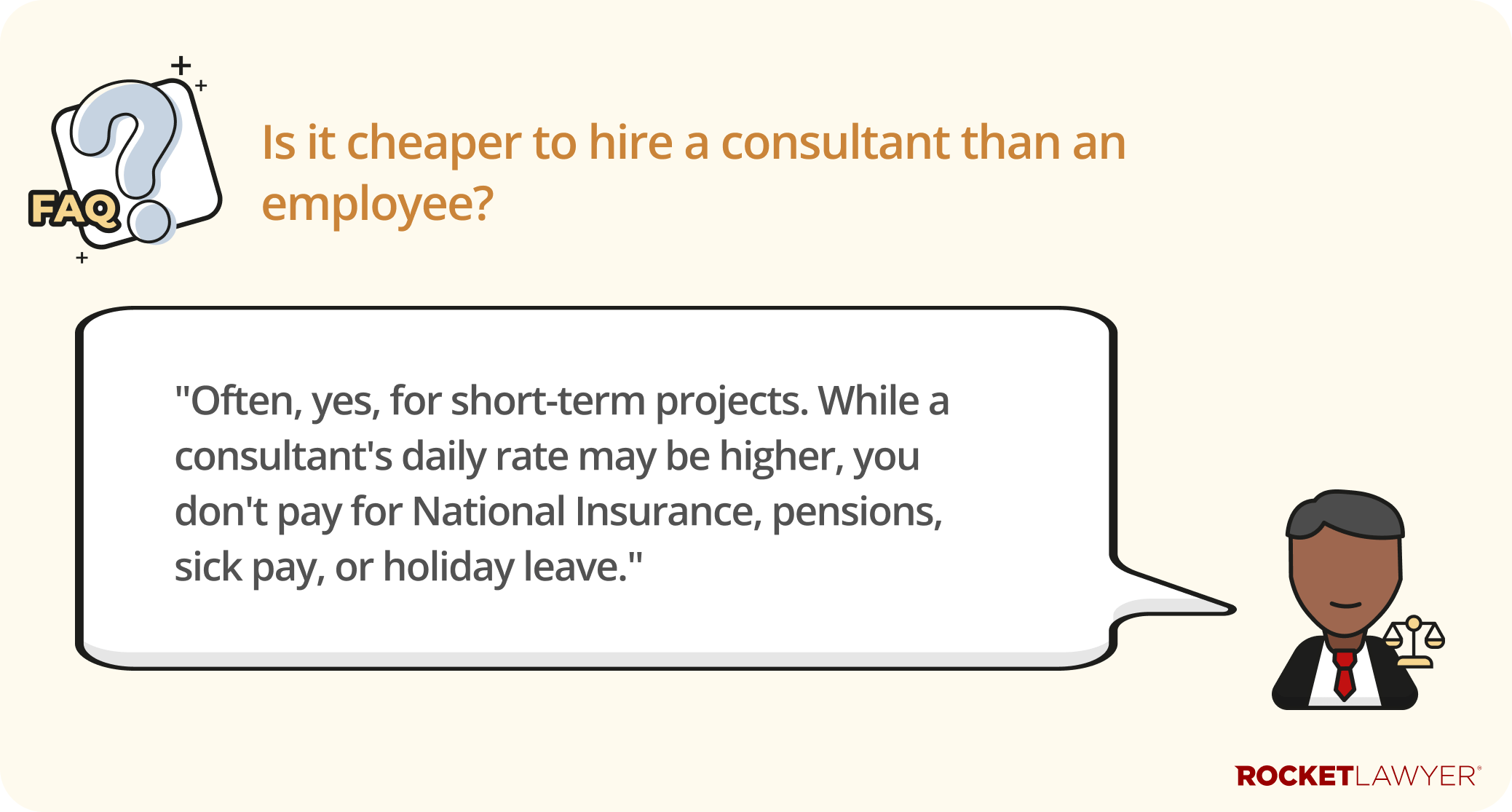

What are the benefits of hiring a consultant?

Businesses often hire consultants for several key reasons. Understanding these benefits can help you decide if it's the right choice for your needs.

One of the main advantages is gaining access to expert knowledge that you don't have within your permanent team. This is perfect for one-off projects, like developing a new marketing strategy or implementing a new software system, where you don't need a full-time employee.

Using a consultant also offers great flexibility and cost-effectiveness. You can engage them for a specific project without the long-term financial commitments of employment, such as employer National Insurance, pension contributions, or other employee benefits.

How do I correctly engage a consultant?

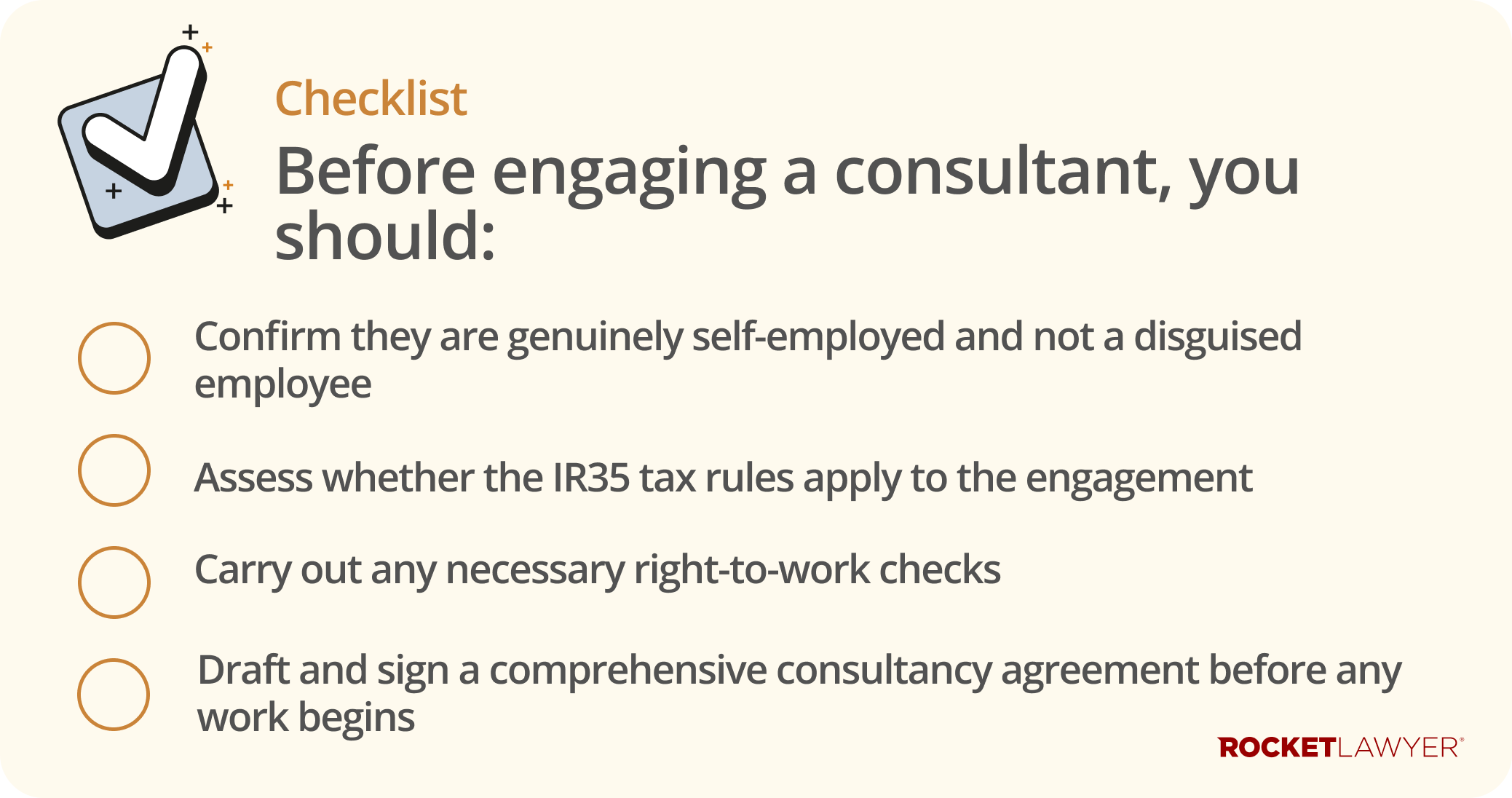

To protect your business and avoid future problems, it's important to follow a clear process when you bring a consultant on board.

Determine their employment status

The first and most critical step is to ensure the person you're hiring is genuinely a self-employed consultant, not a 'worker' or an 'employee' in disguise.

Simply labelling someone as a 'consultant' in an agreement isn't enough. If an Employment Tribunal or HMRC investigates and finds they are treated like an employee, the label will be ignored. This could mean you're suddenly responsible for things like PAYE tax and providing employment rights, losing all the benefits of the consultant relationship.

For a detailed breakdown of how to correctly classify a work relationship, read Consultants, workers, and employees.

Consider IR35 for consultants

The IR35 rules (or 'off-payroll working' rules) are tax laws designed to stop 'disguised employment', where someone works like an employee but is paid as a consultant to avoid tax. If your business is medium or large, it's your responsibility to determine the consultant's status for tax purposes. If HMRC disagrees with your assessment, your business could be liable for unpaid taxes and penalties.

For detailed information on how these rules work and what your obligations are, read IR35. You may need to provide the consultant with an IR35 status determination statement.

Protect your confidential information and IP

You also need to think about confidentiality and any intellectual property (IP) the consultant creates.

Generally, you'll want to ensure that any of your sensitive business information a consultant sees remains confidential, even after their contract ends. Similarly, you'll want to be sure that your business – not the consultant – owns the IP rights to any work they create for you during the engagement. A good contract will cover both of these points clearly.

Think about data protection

When you hire a consultant, you'll be collecting and handling their personal data (eg name and address). The consultant may also be processing personal data on your business's behalf. Because of this, you must comply with the UK General Data Protection Regulation (GDPR) and the Data Protection Act 2018.

For more information, read Data protection and Processing personal data.

Put a strong agreement in place

A clear, written contract is essential. A Consultancy agreement sets out the terms of the relationship, including the consultancy services to be provided, the fees, and how intellectual property and confidentiality will be handled. This document helps to avoid misunderstandings and serves as key evidence that the relationship is one of business-to-business and not employment.

Can I pay a consultant a retainer fee?

A retainer is a fixed, regular payment you make to a consultant to keep them 'on stand-by' so you can use their consultancy services when you need them

While this guarantees you access to their expertise, you should be cautious. Paying an ongoing fee in return for an expectation that the person will be available can create 'mutuality of obligation', which is a key element of an employment relationship. This can weaken their self-employed status and create risks for you under the IR35 rules. Before offering a retainer, carefully consider how it might affect their employment status for tax purposes.

If you’re ready to hire a consultant, you should make a Consultancy agreement. If you have specific questions about your situation, do not hesitate to Ask a lawyer.