What is the Rent a Room scheme?

The Rent a Room scheme allows homeowners to earn up to £7,500 each year tax-free when they rent out a room in their home. To qualify, the room must be:

-

in their only or main home, and

-

offered on a furnished basis

How can you rent out a room?

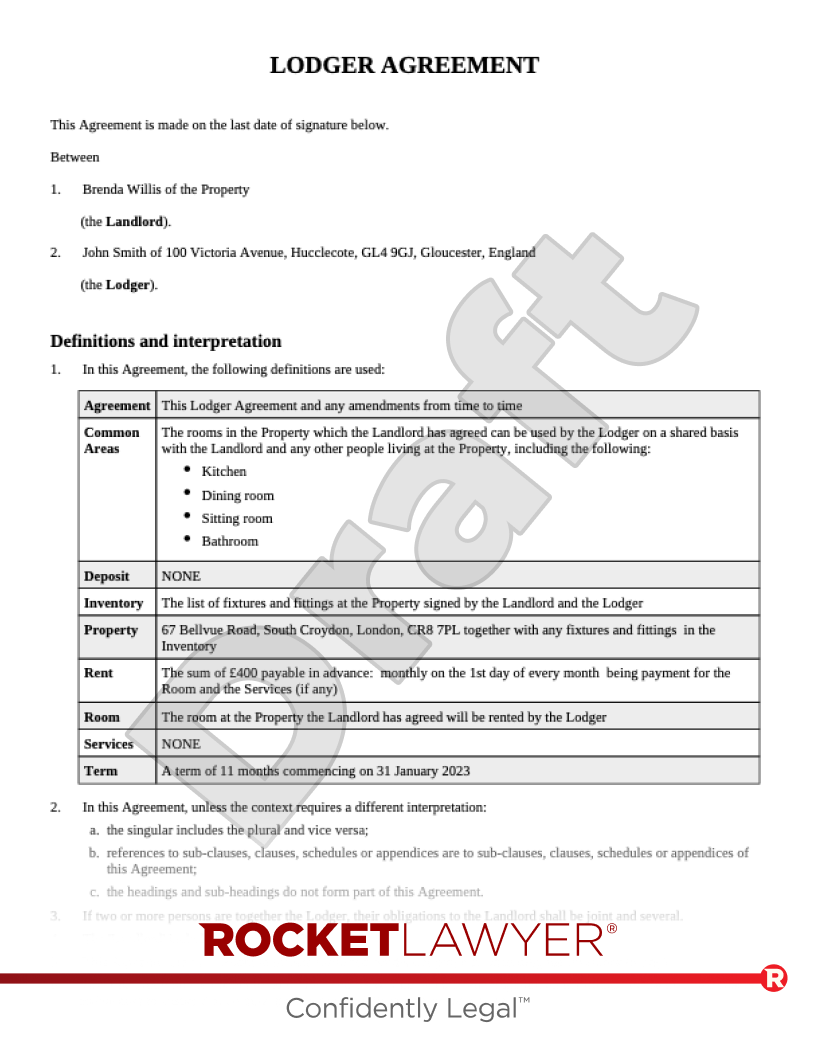

Usually, a furnished room will be let under a Lodger agreement (or Lodger Agreement for Scotland). This is a type of contract that grants someone (ie a lodger) permission to stay in the room and use certain aspects of the home (eg the bathroom and kitchen) but does not grant them a full tenancy of the property. This can be a great way to rent out property, as it generally offers the homeowner more flexibility. For more information, read Taking in a lodger.

Who can take in a lodger?

It’s generally a homeowner’s choice to take in a lodger. However, they may need permission from other parties who have an interest in the property. For example, you may need to obtain permission from your mortgage provider (eg if there are rules about lodgers or renting out your home in the mortgage contract).

People who rent their home may be able to sublet a spare room and utilise the Rent a Room scheme, but they will generally need permission from their landlord.

What tax needs to be paid under the scheme?

The Rent a Room scheme grants a tax exemption. Individuals do not need to pay tax on the first £7,500 that they earn under the Rent a Room scheme within a year.

If someone else also receives income from letting accommodation in the same property (eg your partner or joint owner of the property), your £7,500 allowance is halved to become a £3,750 tax-free allowance per person.

Essentially, the exemption is shared. This includes when you’re both earning income on the rental of the same room.

The tax-free allowance includes income from all expenses charged to the lodger. This means that if your lodger is charged separately (ie in addition to their rent) for cleaning, utility bills, meals, laundry, or similar, these fees make up part of the income that is applied to the tax-free allowance.

How much tax must be paid once you earn more than the tax-free allowance?

Regular income tax must be paid once you earn more than your tax-free allowance from renting out a room.

You can calculate exactly how much tax you need to pay using one of two methods:

-

Method A – you can pay tax only on your actual profits – ie on your income from renting out the room minus any expenses and capital allowances, or

-

Method B – pay tax on your gross income from renting out the room (ie without accounting for any expenses), but only on the amount over your tax-free allowance (ie over £7,500 or £3,750)

Which of these methods will be most advantageous for you largely depends on how much your related expenses amount to. Method A is used by HMRC as a default – you need to tell HMRC if you wish to use Method B.

How do I claim the tax-free allowance?

What you need to do to benefit from the allowance depends on how much income you make from renting out a room:

If you earn less than your tax-free allowance

If you earn less than your tax-free allowance (ie £7,500 or £3,750), there is no requirement to opt into the Rent a Room scheme. The exemption is automatic and you don’t need to do anything to benefit from it. You should keep records of your rental income in case you ever need to demonstrate that you’re earning within your allowance but, as long as any income earned falls within the tax-free threshold, there is no obligation to report this to HMRC.

If you earn over the allowance

If your income from renting out a room is more than your allowance, you’ll need to complete a Self Assessment tax return.

You can choose to opt into the Rent a Room scheme when completing your return and benefit from the tax exemption this way. If you do not wish to claim Rent a Room tax relief, you need to pay tax in the normal way on any rent earned from renting out rooms. You can cover this in the relevant section of a Self Assessment form.

Is a tax return required?

People taking advantage of the Rent a Room scheme who are not otherwise required to submit a Self Assessment tax return (ie people whose income is taxed at source by their employer via PAYE and who do not need to fill out a tax return for other reasons) will not need to complete Self Assessment specifically to deal with income from renting out their room unless they receive income in excess of their tax-free allowance. If they receive more than their allowance, a Self Assessment tax return will be required.

Do I need to notify HMRC?

There is no need to inform HMRC unless income earned under the Rent a Room scheme exceeds your tax-free allowance. If the income earned does exceed your allowance, notify HMRC via your Self Assessment tax return form.

Anyone who decides to opt-out of Rent a Room relief – or switch back into the scheme – should notify HMRC by filling out the relevant section in their tax return. You should also notify HMRC if you want to change the method you use to calculate your exemption.

Do I need to register to rent out a room?

Whether a landlord needs to register before renting out a room depends largely on where in the UK their property is located.

Landlord registration in Scotland

Landlords in Scotland usually need to register as a landlord before renting out residential property. However, you usually do not need to register to rent out a home with a resident landlord (ie to rent out rooms in the only or main home that you live in).

If you are renting to two or more lodgers in your home and between the home’s occupants you make up three or more separate households, your home may constitute a house in multiple occupancy (HMO) and require a HMO licence.

For more information, read Landlord registration in Scotland.

Landlord registration in Wales

Landlords in Wales generally must register as landlords with Rent Smart Wales. However, an exemption applies for homeowners who only rent to lodgers within their own home and share amenities.

Similar to Scotland, you may need a licence if you’re renting out your property as a HMO.

Landlord registration in England

England does not have a nationwide requirement for landlord registration. However, registration may be required depending on where your property is located. Certain local authorities have their own registration and licensing requirements – ie selective licensing schemes. For example, certain areas of London require licences. You can check with your local authority to see whether you need any licences or registrations (eg via their website).

HMOs in England may require licences, as for elsewhere in the UK.

For more information on the Rent a Room tax exemption, read the government’s guidance on the scheme.