MAKE YOUR FREE Partnership Agreement

What we'll cover

What is a Partnership Agreement?

When should I use a Partnership Agreement?

Use this Partnership Agreement:

-

when you and one or more other individuals want to create (or have already created) a general (or ‘ordinary business’) partnership

-

when you want to clarify each partner’s rights and obligations within the partnership and how various situations will be dealt with

-

for individuals based in England, Wales or Scotland

If you want to create a limited liability partnership (LLP), use an LLP agreement instead.

Sample Partnership Agreement

The terms in your document will update based on the information you provide

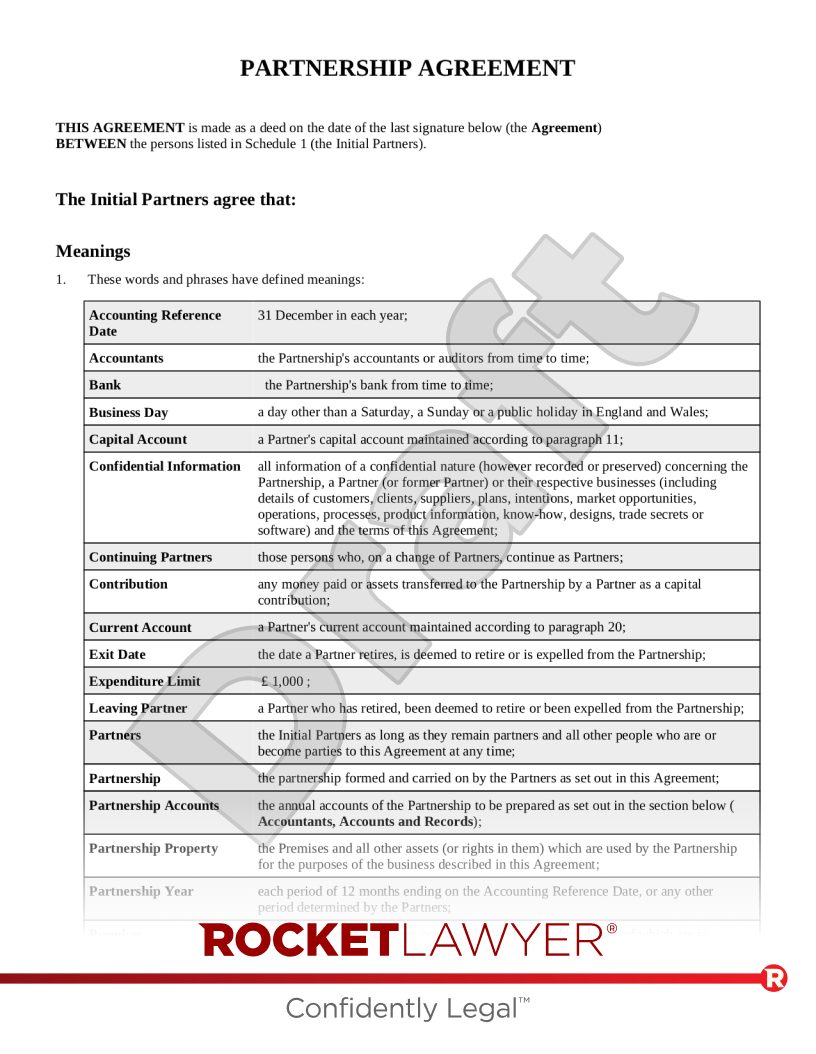

PARTNERSHIP AGREEMENT

THIS AGREEMENT is made as a deed on the date of the last signature below (the Agreement)

BETWEEN the persons listed in Schedule 1 (the Initial Partners).

The Initial Partners Agree That:

Meanings

- These words and phrases have defined meanings:

Accounting Reference Date in each year; Accountants the Partnership's accountants or auditors from time to time; Bank the Partnership's bank from time to time; Business Day a day other than a Saturday, a Sunday or a public holiday in England and Wales; Capital Account a Partner's capital account maintained according to paragraph 11; Confidential Information all information of a confidential nature (however recorded or preserved) concerning the Partnership, a Partner (or former Partner) or their respective businesses (including details of customers, clients, suppliers, plans, intentions, market opportunities, operations, processes, product information, know-how, designs, trade secrets or software) and the terms of this Agreement; Continuing Partners those persons who, on a change of Partners, continue as Partners; Contribution any money paid or assets transferred to the Partnership by a Partner as a capital contribution; Current Account a Partner's current account maintained according to paragraph 20; Exit Date the date a Partner retires, is deemed to retire or is expelled from the Partnership; Expenditure Limit £ ; Leaving Partner a Partner who has retired, been deemed to retire or been expelled from the Partnership; Partners the Initial Partners as long as they remain partners and all other people who are or become parties to this Agreement at any time; Partnership the partnership formed and carried on by the Partners as set out in this Agreement; Partnership Accounts the annual accounts of the Partnership to be prepared as set out in the section below (Accountants, Accounts and Records); Partnership Property the Premises and all other assets (or rights in them) which are used by the Partnership for the purposes of the business described in this Agreement; Partnership Year each period of 12 months ending on the Accounting Reference Date, or any other period determined by the Partners; Premises the offices or other premises occupied by the Partnership, details of which are in paragraph 10; and Profit for any Partnership Year, the net profit of the Partnership as shown by the Partnership Accounts for that Partnership Year, and Loss has a corresponding meaning. - In this Agreement, unless the context means a different interpretation is needed:

- including means "including without limitation";

- words denoting the singular include the plural and vice versa, and words denoting any gender include all genders;

- a person includes firms, companies, government entities, trusts and partnerships;

- a party means a party to this Agreement and includes its assignees and successors in title and, in the case of an individual, to their estate and personal representatives;

- reference to a paragraph or Schedule is to a paragraph or Schedule of or to this Agreement (and the Schedules form part of this Agreement);

- reference to a statute or statutory provision includes any modification of or amendment to it, and all statutory instruments or orders made under it; and

- reference to writing or written includes faxes and email but not any other type of electronic communication.

- The headings in this Agreement are for convenience only and do not affect its meaning.

Formation and Name

- The Partnership is formed for the purpose of engaging in .

- The Partnership is called .

- Any person can with this agreement be appointed as a Partner provided:

- their appointment is approved by a unanimous vote of the Partners; and

- they enter into a written instrument, stating the date on which the appointment takes effect and otherwise in such form as the Partners specify, under which they agree to be bound by the terms of this Agreement.

Start Date and Duration

- The Partnership begins on or, if the Agreement is signed after , is deemed to have begun on .

- The Partnership will not automatically dissolve if any Partner stops being a Partner by reason of their death, retirement or expulsion, or a new Partner is admitted, under the provisions of this Agreement.

- The Partnership continues until dissolved by the Partners under the section below (Management and Decisions).

Place of Business

- The business of the Partnership is carried on at the premises known as or such other premises as the Partners from time to time determine under the section below (Management and Decisions).

Capital

- Each Partner will have a Capital Account. Any Contribution made by that Partner, their share of any capital profits and any interest payable on their share in the Partnership capital will be credited to their Capital Account. Any repayment of capital to a Partner and their share of any capital losses will be debited to their Capital Account. Each Capital Account will be adjusted to reflect any revaluation of assets.

- The initial capital of the Partnership is to be contributed immediately by the Partners equally.

- Any Contribution must be:

- a payment in cash into the Partnership bank account, and/or

- with the agreement of all the other Partners, a contribution of assets.

- If at any time the Partners decide to increase the capital of the Partnership, the amounts of the increase will be contributed in such proportions as they may agree and, in default of agreement, in the same proportions to which they are entitled to share in the capital of the Partnership.

- The capital for the time being of the Partnership belongs to the Partners in the proportions to which the balance of each of their Capital Accounts bears to the total capital of the Partnership.

- No Partner is entitled to any interest on the amount of their share of the Partnership capital unless agreed by all the Partners.

- No Partner while in the Partnership can withdraw any of their capital except with the written consent of all the other Partners.

Profits and Losses

- The Partners will share the Profit for each Partnership Year and bear any Loss for any Partnership Year unless otherwise determined by the Partners.

- If any person is a Partner for part only of a Partnership Year, their share of any Profit or Loss for that Partnership Year will be calculated as if they have been a Partner for the whole of that Partnership Year, but the share to which they would otherwise have been entitled will then be reduced by applying a fraction, where the denominator is the number of days in the Partnership Year, and the numerator is the number of days in that Partnership Year during which the person was not a Partner.

Current Accounts, Drawings and Tax

- Each Partner will have a Current Account. The Partner's share of any Profit (other than capital profits) will be credited to their Current Account. Any drawings made by the Partner, any payments of or provisions for tax and the Partner's share of any Loss (other than capital losses) will be debited to their Current Account.

- Each Partner is entitled to draw on account of their share of the Profit for the then-current Partnership Year such sum as the Partners may determine.

- As soon as practicable after the Partnership Accounts are approved under paragraph 30, each Partner's Current Account will be credited or (as the case may be) debited with their share of the Profit or Loss for that Partnership Year, after reserving out of the Profit before distribution any tax which the Accountants estimate is payable by that Partner during the next Partnership Year and after taking into account any amount which has been credited or debited to that Partner's Current Account during the Partnership Year under paragraph 20. If, after this, there is a debit balance on that Current Account, that Partner will, unless the Partners otherwise determine, pay to the Partnership a sum equal to that balance within 30 days from the date which the relevant Partnership Accounts are approved under paragraph 30.

- Subject to paragraph 22, no Partner can, without the previous consent of the Partners, allow a debit balance to arise on their Current Account, and each Partner must, at the request of the Partners, immediately pay to the Partnership the amount of any such debit balance.

- Without prejudice to paragraph 23 above, if there is at any time a debit balance on any Partner's Current Account then (except as set out in paragraph 25 below) interest, calculated at the rate of % above the base lending rate from time to time of the Bank (the Interest Rate), is payable by the Partner on the amount of the balance outstanding from time to time until payment is made in full.

- Interest is not payable on any part of that debit balance (i) which is attributable to the Partner's share of any Loss for any Partnership Year and is paid to the Partnership under paragraph 22 and (ii) where the obligation to repay such debit balance has not yet arisen under paragraph 22.

- The Partners will ensure that any amount of Profit reserved under paragraph 22 on account of tax estimated to be payable by a Partner is paid to HM Revenue & Customs (or other appropriate tax authority) at the appropriate time

Accountants, Accounts and Records

- The Partners will ensure that proper books of accounts are kept giving a true and fair view of the Partnership's business. The books are available for inspection by each of the Partners and the Accountants at any time.

- As soon as practicable after the end of each Partnership Year, the Partners will instruct the Accountants to draw up a profit and loss account in respect of that Partnership Year and a balance sheet as at the relevant Accounting Reference Date (Partnership Accounts).

- The Partnership Accounts must be approved by the Partners and, once approved, will become binding on each of the Partners, except in the case of manifest error.

Bank Accounts

- The Bank is the banker of the Partnership.

- All Partnership monies not required for current expenses and all cheques must be paid promptly into the Partnership bank account.

- All cheques or instructions for the electronic transfer of money from any account of the Partnership with the Bank will be in the Partnership's name and can be drawn or given:

- for amounts up to and including the Expenditure Limit, by any Partner; and

- for amounts in excess of the Expenditure Limit, by the Managing Partner.

- In the case of instructions for electronic transfer, written confirmation of those instructions will be signed by the Managing Partner.

Partnership Property

- Partnership Property belongs to the Partners in the proportions in which they are entitled to share in the capital of the Partnership.

- Any Partnership Property which is vested in one or more of the individual Partners' names is held by them on trust for sale for all of the Partners. All costs and expenses relating to such Partnership Property will be borne by the Partnership and the other Partners shall indemnify the Partner or Partners in whom such property is vested against all liabilities which may arise directly or indirectly in respect of it.

Indemnity

- Each Partner will indemnify and keep indemnified the other Partners from and against all payments made and liabilities incurred by each such Partner in the performance of their duties as a Partner in the ordinary course of the business of the Partnership or in respect of anything necessarily done by them for the preservation of the business or Partnership Property.

Insurance

- The Partners will obtain and maintain policies of insurance against risks and for amounts as the Partners agree for:

- Partnership Property;

- employers' liability;

- public liability;

- professional negligence;

- loss of profits resulting from the destruction of or damage to premises used to carry out the business of the Partnership;

- loss of profits resulting from the destruction of or damage to or theft of any plant equipment, chattels, cars and other vehicles, including in the case of any computers or ancillary equipment any virus or corruption or loss of any software or data;

Holidays

- Each Partner is entitled to a total of holiday in each Partnership Year. Each Partner must consult with the about the time when the Partner intends to take holidays and take them at a time considered most practical for the Partnership.

Obligations of Partners

- Each Partner agrees at all times:

- to use their best skills and endeavours towards the successful operating of the Partnership and at all times conduct themselves in a fair and proper manner in all transactions of any nature affecting the Partnership;

- to disclose to the other Partners any matter that may prejudice the business prospects of the Partnership and generally show the utmost good faith to the other Partners in all transactions relating to the Partnership;

- not to disclose Confidential Information to any person, firm or business unless with the prior written consent of all the other Partners;

- that no other partners will be added to the Partnership without the express prior written approval of all of the Partners;

- to keep proper records of all business transacted by or on behalf of the Partnership;

- to duly and punctually pay and discharge their separate and private debts and liabilities and keep the Partnership, the Partnership Property and the other Partners and their respective estates and effects indemnified against all actions, proceedings, costs, claims, and demands in relation to such private debts and liabilities;

- to comply with all regulations, professional standards and other provisions about the conduct of the Partnership's business generally, including any directions made from time to time by the Partners.

- Each Partner agrees that they will not without the written consent of all the other Partners:

- whilst they are a Partner, carry on or be engaged or interested in any business, occupation or activity or take steps to set up or promote or facilitate the establishment of any business, occupation or activity which competes or intends to compete with any part of the business of the Partnership;

- employ, or terminate the employment of, any employee or agent of the Partnership;

- loan any money or Partnership Property to any other person, firm or business, nor accept any such money or property, whether in the form of a loan or otherwise, on behalf of the Partnership from any other person, firm or business;

- offer a guarantee, security or any other promise for the payment of any liabilities incurred by the Partnership in the ordinary course of business, nor shall they accept a guarantee, security or promise for such sums as may be owed to the Partnership from time to time, nor shall accept any compromise or part-payment of any such sums that may be owed to the Partnership from time to time;

- transfer, mortgage, or charge their share in the Partnership or any part of it;

- open any bank account or borrow any money in the name of or for the Partnership.

Management and Decisions

- Unless this Agreement specifies otherwise, where a matter under this Agreement requires the decision of the Partners, such matter will be determined by the Partners by simple majority vote.

- The following matters require the unanimous consent of the Partners:

- the admission of new Partners to the Partnership;

- the alteration of the Partners' shares in Profits and Losses;

- any change to this Agreement;

- the Partnership giving a guarantee in excess of the Expenditure Limit;

- changing the Premises or opening new premises;

- changing the name of the Partnership;

- the Partnership borrowing or lending any sum in excess of the Expenditure Limit;

- the acquisition or disposal of all or part of the business of the Partnership or merger with another partnership;

- any purchase of a capital item by the Partnership costing in excess of the Expenditure Limit;

- a change in the Accounting Reference Date;

- a change in the business of the Partnership as set out in paragraph 4;

- the expulsion of any Partner;

- any decision to dissolve the Partnership.

- Meetings of the Partners may be called by any Partner .

- No less than days' notice of the meeting must be given to all those entitled to attend, but a meeting can be convened at shorter notice if all the Partners agree in writing.

- The quorum for a meeting of the Partners is Partners.

Goodwill

- The goodwill of the Partnership is deemed to be of nil value and the share of a Leaving Partner in the goodwill, if any, of the Partnership automatically accrues to the Continuing Partners and no Leaving Partner has any claim in respect of it.

Expenses

- Each Partner is entitled to claim back out-of-pocket expenses properly incurred by them in connection with the Partnership on provision of a receipt and VAT invoice where appropriate.

- The Partners can decide to place upper limits on any category or categories of expenses that can be claimed.

Voluntary Retirement

- A Partner can retire from the Partnership by giving not less than written notice to the other Partners. Their Exit Date will be the date that notice expires.

Involuntary Retirement

- A Partner will be deemed to retire from the Partnership:

- immediately on their death and their Exit Date will be the date of their death;

- on expiry of at least three months' written notice from the Partners requiring them to retire as a Partner because they have been unable to perform their duties as a Partner for either:

- a continuous period of 6 months or more; or

- an aggregate period of 6 months or more during the previous 12 month period.

- immediately if the Partners serve them written notice requiring them to retire as a Partner after they have become a patient under the Mental Health Act 1983 and their Exit Date will be the date of that notice.

Expulsion

- The other Partners may by written notice (signed by all of them) to the Partner concerned expel that person immediately from membership of the Partnership if that person:

- commits a serious breach of this Agreement which is either incapable of remedy or is not remedied within Business Days after it occurs;

- commits persistent breaches of this Agreement;

- has a bankruptcy order made against them;

- fails to pay any money owed by them to the Partnership within 10 Business Days of a written request for payment from the Partnership or any Partner;

- is guilty of any conduct likely to have a serious negative effect upon the business of the Partnership; or

- no longer holds a professional qualification or certification required for the normal performance of their duties as a Partner.

- If the Partners are not already aware, a Partner must inform the other Partners as soon as possible after the occurrence of an event mentioned in the above paragraph.

- The expulsion notice must give sufficient details of the alleged breach or breaches.

- The expelled Partner's Exit Date is the date of expiration of the expulsion notice.

Provisions Relating to Leaving Partners

- If a Partner retires, is deemed to retire or is expelled on a date other than an Accounting Reference Date:

- they are not entitled to receive any share of the Profit and will not be liable for any share of the Loss of the Partnership arising after their Exit Date;

- the Partnership is not obliged to prepare any accounts other than the Partnership Accounts which would normally be prepared up to the next Accounting Reference Date; and

- the Profit or Loss shown in those Partnership Accounts will be apportioned on a time basis for the periods before and after the Partner's retirement, deemed retirement or expulsion in order to calculate the amount of their share in the Profit or Loss.

- On retirement, deemed retirement or expulsion of a Partner the Partnership will owe them the amount of their share in the Partnership capital as shown in the Partnership Accounts as at either the Accounting Reference Date following their Exit Date or the Accounting Reference Date that is their Exit Date. For the avoidance of doubt, there will be no amount payable to them in respect of goodwill.

- If a Partner is expelled and the profitability of the Partnership is reduced as a result of any event which led to their expulsion, the other Partners may instruct the Accountants (or, if they are unwilling or unable to act, an alternative firm of accountants appointed by the President of the Institute of Chartered Accountants in England and Wales) to certify as experts the amount of that reduction in profitability. Regardless of any other paragraph in this Agreement, the amount that would otherwise be payable to the expelled Partner will be reduced by the certified amount of that reduction in profitability.

Payments to Leaving Partners

- On the death of a Partner the Partners must:

- on the first day of the next three months, pay an amount equal to their normal monthly drawings then applicable. These payments will be made to the deceased Partner's personal representatives, widow or another person as the Partners decide in their absolute discretion (but the Partners are not concerned whether or not the recipient(s) of these payments will prove to be entitled at law to the deceased Partner's estate); and

- pay the Partner's share in the capital of the Partnership (after allowing for the payments referred to in the above paragraph to the deceased Partner's personal representatives) as soon as reasonably practical but in any case within one year of their death (together with interest at the Interest Rate on the amount payable).

- On the retirement, deemed retirement (other than on a death) or expulsion of a Partner, the Partnership will pay to the retiring or expelled Partner the amount of that Partner's share in the capital of the Partnership (together with interest at the Interest Rate on any part of it outstanding). The payment will be made by four equal six-monthly instalments. The date of the first instalment will be either the Accounting Reference Date following their Exit Date or the Accounting Reference Date that is their Exit Date. Instalments can be paid earlier by the Partners at their discretion.

Leaving Partners' Obligations

- Each Leaving Partner must pay into the Partnership's bank account immediately all sums due from them to the Partnership and any of these sums which are not paid will be recoverable from them by the Partners as a debt.

- Each Leaving Partner must return to the Partners all accounting records, letters and other documents in their possession relating to the Partnership which are needed for the continuing conduct of the business of the Partnership. While the Leaving Partner is owed money by the Partners, they or their duly authorised agents are permitted to inspect by appointment the Partnership's accounting records, letters and other documents to the extent they relate to any period preceding the Exit Date.

- Each Leaving Partner must promptly do all things and sign all documents reasonably requested by the Partners (and at the Partners' sole expense) to assign or transfer to the Partners any property or assets which immediately prior to the Exit Date were owned by or vested in the Leaving Partner as nominee for or in trust for the Partners.

GENERAL

Dissolution

- If the Partnership is dissolved, the affairs of the Partnership will be wound up and the assets and liabilities dealt with in the manner provided by the Partnership Act 1890.

Entire Agreement

- This Agreement contains the whole agreement between the parties relating to its subject matter and supersedes all prior discussions, arrangements or agreements that might have taken place in relation to the Agreement. Nothing in this paragraph limits or excludes any liability for fraud or fraudulent misrepresentation.

Assignment

- No party may assign, transfer, sub-contract, or in any other manner make over to any third party the benefit and/or burden of this Agreement without the prior written consent of the other party or parties.

Variation

- No variation to this Agreement will be valid or binding unless it is recorded in writing and signed by or on behalf of each of the parties.

Notices

- Any notice (other than in legal proceedings) to be given to a Partner under this Agreement must be in writing and delivered by handing such notice to the Partner in question personally, or by sending it pre-paid first class post to or by leaving it by hand delivery at the last known address of the Partner in question or, being addressed to such Partner, by sending it pre-paid first class port to or by leaving it by hand delivery at the main place of business of the Partnership or by sending it by email to an address notified by the Partner in question as being an address at which such Partner is prepared to accept service of notices.

- Notices which are:

- sent by post will be deemed to have been received, where posted from and to addresses in the United Kingdom, on the second Business Day after the date of posting, and where posted from or to addresses outside the United Kingdom, on the tenth Business Day after the date of posting;

- delivered by hand will be deemed to have been received at the time the notice is left at the proper address; and

- sent by email will be deemed to have been received on the next Business Day after sending.

Miscellaneous

- The Contracts (Rights of Third Parties) Act 1999 shall not apply to this Agreement and no third party will have any right to enforce or rely on any provision of this Agreement.

- Unless otherwise agreed, no delay, act or omission by a party in exercising any right or remedy will be deemed a waiver of that, or any other, right or remedy.

- Provisions which by their intent or terms are meant to survive the termination of this Agreement will do so.

- If any court or competent authority finds that any provision of this Agreement (or part of any provision) is invalid, illegal or unenforceable, that provision or part-provision will, to the extent required, be deemed to be deleted, and the validity and enforceability of the other provisions of this Agreement will not be affected.

Governing Law and Jurisdiction

- This Agreement and any non-contractual obligations arising in connection with it will be governed by and interpreted according to the law of England and Wales. All disputes arising under or in connection with the Agreement will be subject to the exclusive jurisdiction of the English and Welsh courts.

SCHEDULE 1

Details of Initial Partners

About Partnership Agreements

Learn more about making your Partnership Agreement

-

How to make a Partnership Agreement

Making your Partnership Agreement online is simple. Just answer a few questions and Rocket Lawyer will build your document for you. When you have all the information about the partnership relationship prepared in advance, creating your document is a quick and easy process.

You’ll need the following information:

Key details about the partnership

-

What’s the partnership’s name?

-

What is its main purpose?

-

On which date was it formed?

-

What’s the partnership’s address?

Partners

-

What is each partner’s name and address?

-

Will you appoint a managing partner? If so, what’s their name and how many years will you appoint them for?

Partners’ benefits

-

What is the partners’ annual leave entitlement?

-

Are there restrictions on how many days’ holiday can be taken at once? If so, what’s the limit?

-

Partners’ obligations

-

If a partner breaches the Partnership Agreement, how many days do they have to remedy this breach (ie before the other partners may expel them from the partnership)?

-

If a partner owes money to the partnership, what interest rate is applicable to this debt?

Day-to-day operations of the partnership

-

How many days’ notice is required to call a meeting of the partnership?

-

Are all partners required to conduct a meeting? If not, how many are required?

-

Does the partnership already have a bank account? If so, with which bank?

-

Has the partnership appointed accountants? If so, which accountants?

-

What is the partnership’s accounting reference date (ie the end of its accounting year)?

-

Regarding expenditures, what’s the expense limit above which the managing partner’s (if appointed) or more than one partner’s approval is required?

Capital and income

-

Will the partners contribute (or have they already contributed) to the partnership’s initial capital in equal or in specified unequal amounts?

-

If they’re contributing in equal amounts, what’s the total amount of the partnership’s initial capital?

-

If they’re contributing in unequal amounts, how much is each partner’s contribution?

-

-

Will the partners share profits and losses in equal or in specified unequal amounts? If in unequal amounts, what’s each partner’s profit share (as a percentage)?

Leaving the partnership

-

How much notice do partners need to give to voluntarily leave the partnership?

-

Will any restrictions be imposed on partners after they leave the partnership? You may include restrictions on soliciting or supplying goods and services to the partnership’s customers, soliciting the partnership’s partners or employees, or engaging in a competing business.

-

If any restrictions are included in the Agreement, how long will they apply for?

-

If you include a non-solicitation provision, how long must the leaving partner have known the customer for, if it’s to apply?

-

If you include a restriction on competing, within how many miles of the partnership’s places of business can the partner not participate in competing business activities?

-

The Partnership Agreement

- If the partnership is based in Scotland, will the Agreement be governed by the laws of England and Wales or the laws of Scotland?

-

-

Common terms in a Partnership Agreement

Partnership Agreements set out the terms of a partnership relationship and key details of how the partnership will be run. To do this, this Partnership Agreement template includes sections covering:

This Agreement

The Agreement starts by identifying the date of and parties to the Agreement.

Meanings

This definition table assigns specific meanings to key terms used throughout the Agreement. When these terms (eg ‘Accounting Reference Date’, ‘Initial Partners’ or ‘Partnership Accounts’) are used capitalised throughout the Partnership Agreement, they carry the meaning they’re given in this table.

Formation and name

This section sets out the partnership’s fundamental details, including its name, key purpose, and its basic rules for appointing new partners to the partnership.

Start date and duration

Here the Agreement specifies the date that the partnership began/will begin, and states that it will continue until dissolved.

Place of business

The partnership’s main business premises are identified here and the possibility of carrying out business at other locations is noted.

Capital

This section sets out a requirement that each partner will have a capital account and specifies what will be included in it. It further sets out the partners’ contributions to the partnership’s initial capital, how capital can be added or withdrawn, and how it’s owned.

Profits and losses

The partners’ proportion shares in the partnership’s profits and losses are specified here, alongside rules for calculating shares for partners who weren’t partners for a whole partnership year.

Current accounts, drawings and tax

This section sets out various rules for the operation of partners’ current accounts. For example, it covers rules for allowing debits to arise and for paying interest due.

Accountants, accounts and records

This section sets out the partners’ obligations to maintain accurate accounts and the binding nature of approved accounts. It also specifies the partnership’s accountants, if appointed.

Bank accounts

This section sets out how the partnership’s bank accounts must be dealt with. For example, the requirement for partnership money that’s not immediately needed to be paid into the accounts.

Partnership property

This section specifies that the partners own the partnership’s property (ie real property and other assets) in the same shares in which they own the capital. It sets out how this is managed in terms of legal and beneficial ownership.

Indemnity

An indemnity is provided in this section, by each partner to all other partners, against any payments made and liabilities incurred by that partner during the course of ordinary partnership business conducted to preserve the partnership.

Insurance

This section sets out the types of insurance (eg public liability and professional negligence) that the partners must take out, for agreed amounts.

Holidays

This section sets out the partners’ holiday entitlements under the partnership and rules for taking holiday.

Obligations of partners

This section sets out a series of things that the partners all agree to do or not to do. For example, they promise:

-

not to disclose the partnership’s confidential information

-

to use their best skills and endeavours to promote the success of the partnership

-

not to deal with (eg mortgage or transfer) their share in the partnership without the other partners’ consent

-

not to employ or let go any partnership employees without the other partners’ consent

Management and decisions

Rules on how partnership decisions can be made are contained in this section. It sets out a list of decisions that require the partners’ unanimous agreement (eg admitting new partners or changing aspects of the Partnership Agreement). It sets out that all other decisions can be made by simple majority (ie when more than 50% of partners agree).

If a managing partner is being appointed, this appointment is set out here alongside their responsibilities (eg executing partnership policies and arranging meetings) and what happens when their term is over.

Lastly, this section sets out rules for holding partnership meetings.

Goodwill

This section explains that the partnership’s goodwill (ie the partnership’s good reputation related to its products) does not have monetary value and partners have no claim over it if they leave the partnership.

Expenses

Partners’ right to claim payment for necessary expenses related to the partnership is set out here.

Voluntary retirement

This section sets out partners’ ability to retire from the partnership by choice by giving a specified amount of notice.

Involuntary retirement

This section sets out situations in which partners will be considered to have retired from the partnership without their explicitly doing so. For example, if they die or they’re unable to perform their duties to the partnership for a long period of time.

Expulsion

This section sets out when the collected partners can require one of the partners to leave the partnership. For example, if they’ve committed a material (eg very serious) breach of the Partnership Agreement or they’ve had a bankruptcy order made against them. It sets out the required procedure for such expulsions.

Provisions relating to leaving partners

This section sets out how a partner’s shares of the partnership’s capital, income, and losses will be handled when they leave the partnership.

Payments to leaving partners

This section specifies how capital and other payments will be made when a partner leaves, differing depending on whether the partner died or left for other reasons.

Leaving partners’ obligations

A partner’s obligations on leaving the partnership are set out here. For example, they must pay any sums due to the partnership, return partnership documents, and transfer any assets held in their name for the partnership to the remaining partners.

Any restrictions you’ve chosen to impose on leaving partners will also be included here. For example, non-solicitation and non-compete clauses.

General

This section deals with various other points of law that govern how this Partnership Agreement operates. For example:

-

explaining that, if the partnership is dissolved, the partnership’s assets and liabilities will be dealt with following the provisions of the Partnership Act 1890

-

stating that this Agreement is the entire agreement, ie the Partnership Agreement contains all of the agreement between the partners (ie there are no additional terms)

-

restricting how the partners can deal with the Agreement (eg preventing them from assigning their benefits under the Agreement to others)

-

requiring that any variations to the Agreement must be made in writing

-

excluding the Contracts (Rights of Third Parties) Act 1999 or the Contract (Third Party Rights) (Scotland) Act 2017, except in certain circumstances. This essentially means that third parties (ie not one of the partners) that would otherwise be able to enforce obligations under this Agreement under the Act cannot do so

-

setting out how any notices or other similar communications that must be given under the Agreement should be delivered

-

which country’s legal system must be used to resolve any disputes (ie the Agreement’s jurisdiction). This is necessary as the legal systems of England and Wales and of Scotland are different

Schedule 1 - Details of initial partners

This schedule contains the names of all of the original partners to the partnership and, if not in equal shares, their shares of profits and contributions to the initial capital.

This Agreement has been executed as a deed…

The Agreement ends with spaces for the partners and their witnesses to sign the document. It also states that the document is signed as a deed.

If you want your Partnership Agreement to include further or more detailed provisions, you can edit your document. However, if you do this, you may want a lawyer to review the document for you (or to make the changes for you) to make sure that your modified Partnership Agreement complies with all relevant laws and meets your specific needs. Use Rocket Lawyer’s Ask a lawyer service for assistance.

-

-

Legal tips for partners

Make sure you’re creating the right sort of partnership for your business needs

Various types of partnerships exist in the UK, each with different legal characteristics, benefits, and obligations. It’s important to choose the type of partnership that best fits your planned business operations.

Limited liability partnerships (LLPs), for example, operate similarly to limited companies in many ways (eg they are discrete legal entities to their members, whose liability for the business’ debts is limited). A general partnership does not share these similarities. However, general partnerships also don’t need to meet as many formalities as LLPs (eg general partnerships don’t need to make as many filings and don’t require Companies House registration).

For more information, read Types of partnership, Setting up a partnership, and Running a partnership.

Understand when to seek advice from a lawyer

In some circumstances, it’s good practice to Ask a lawyer for advice to ensure that you’re complying with the law and that you are well protected from risks. You should consider asking for advice if:

-

you don’t know which type of partnership is right for you

-

you want to create a partnership where one or more partners are limited companies or other types of organisation

-

you’re unsure how to fulfil your tax obligations in a partnership

-

Partnership Agreement FAQs

-

What should a Partnership Agreement include?

This Partnership Agreement template covers:

-

who the partners are

-

each partner’s capital contributions and profit shares

-

partners' duties and entitlements

-

rules for management and decision-making

-

how partners may leave the partnership and what happens when they do

-

-

Why do I need a Partnership Agreement?

A Partnership Agreement isn’t required to start a partnership - a partnership can be formed simply by the partners starting to carry on business together and sharing profits in a manner that fulfils the definition of a partnership.

It’s a good idea, however, to make a Partnership Agreement to set out key elements of how you’ll run your partnership. For example, you can set out how your business will prepare for common business scenarios, how a partner may leave, and how you will handle disproportionate contributions to the partnership. Setting out clear business expectations helps partners to avoid future misunderstandings.

For more information, read Setting up a partnership and Running a business partnership.

-

What is a partnership?

A partnership (or ‘general partnership’), as defined in the Partnership Act 1890, is a relationship between two or more partners (eg individuals or companies) in which they carry out a business with a view to making a profit. A general partnership, unlike a company or an LLP, is not a separate legal entity to its members (eg the partners remain personally liable for the partnership’s debts and obligations). For more information, read What is a partnership?.

-

Can a company be a partner in a partnership?

Partners can be individuals, companies or LLPs. This Partnership Agreement template can only be used to create a partnership in which all initial members are individuals. If you want to create a partnership with parties of different legal structures, Ask a lawyer for assistance.

-

What is a capital account?

Capital accounts are part of a partnership’s accounts records that record certain transactions made by the partners. These include:

-

their initial and subsequent capital contributions

-

any interest payable on their share of the partnership capital

A partnership can maintain a single capital account for all of the partners. However, it is easier to maintain separate capital accounts within the accounting system for each partner. This way, in the event of a partnership dissolution or the departure of a partner, it’s easier to determine the payments and liabilities of each partner.

Note that partners cannot withdraw any capital money from the partnership’s accounts while in a partnership unless they have the written consent of all of the partners.

-

-

What is a current account?

Current accounts are part of a partnership’s accounts records in which each partner's share of any profits is credited. Any share of losses, withdrawals by the partner, or tax payments will be taken from this account.

-

How are a partnership’s profits attributed and losses accounted for?

The partners will share the profits and bear any losses made within any partnership year (ie each period of 12 months ending on a specified accounting reference day or any other period determined by the partners).

This Partnership Agreement allows for an accounting period (ie the period for which the partnership has to prepare accounts) of 12 months, ending on a specified date.

-

How can partners exit the partnership?

Under this Partnership Agreement, partners may exit (ie leave) the partnership by either:

-

voluntarily retiring

-

involuntary retiring - this applies if a partner dies or if a partner needs to retire because, for example, they have not been able to perform their duties for a long period

-

written notice of expulsion - a partner may be expelled from a partnership if, for example:

-

they have committed a serious breach of the Partnership Agreement

-

a bankruptcy order is made against them

-

they have failed to pay money owed to the partnership within 10 business days of a written request for the money, or

-

they no longer hold a necessary professional qualification

-

-

-

What obligations are imposed on partners when they leave?

A leaving partner:

-

must pay into the partnership's bank account all sums that they owe to the partnership

-

must return all accounting records, letters and other relevant documents in their possession

-

may (if specified in your Partnership Agreement) not solicit customers, entice away employees, or engage in competing business

-

-

Are partners personally liable for paying their taxes?

Partners who are individuals must pay their own income tax and National Insurance Contributions through Self Assessment.

Our quality guarantee

We guarantee our service is safe and secure, and that properly signed Rocket Lawyer documents are legally enforceable under UK laws.

Need help? No problem!

Ask a question for free or get affordable legal advice from our lawyer.