What is a general partnership?

General partnerships (also known as ‘ordinary business partnerships’) are the simplest and most common type of partnership in the UK.

Key features of general partnerships

A general partnership is defined by its straightforward nature and the direct responsibility of its partners:

-

liability - partners have unlimited liability, meaning their personal assets are at risk to cover business debts. This is also known as ‘joint and several liability’

-

legal status - the business is not legally separate from its owners

-

management and profits - all partners can be involved in management and have a right to share in the profits

-

administration - you must register each partner with HMRC for Self Assessment, but there is no requirement to register with Companies House. A written Partnership agreement is not legally required, but is highly recommended to prevent disputes

Bear in mind that you, along with the other partners in the partnership, will be acting as agents for each other, and you will be individually responsible for your and their actions as well as being collectively responsible as a partnership. As a partner, you must comply with your fiduciary duties to act honestly and in the best interests of the partnership, and you must tell the other partners about any benefit you have derived from the partnership without the consent of the other partners.

For more information on setting up a general partnership, read How to set up and register a partnership..

Anyone starting a general partnership should enter into a written Partnership agreement, to prevent disputes between partners.

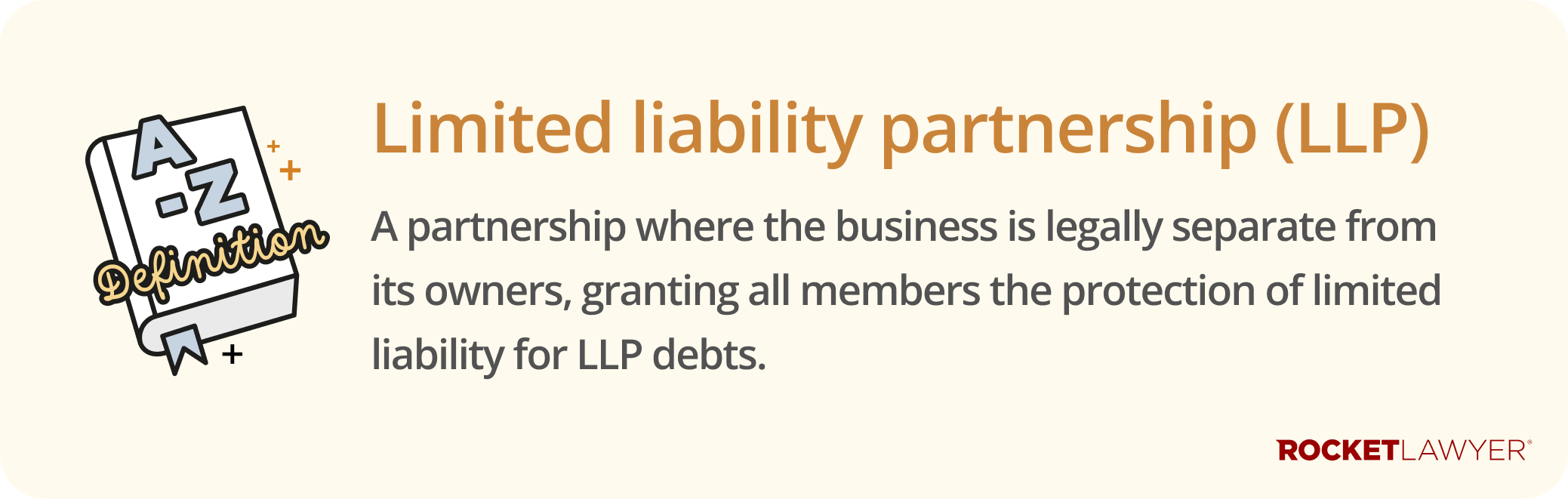

What is a limited liability partnership (LLP)?

An LLP is a corporate body with a legal personality separate from its members (ie partners). The members in an LLP aren’t personally liable for debts the business can’t pay. Instead, their liability is limited to the amount of money they invest in the business.

This structure is popular with professional services firms, like solicitors and accountants.

Key features of LLPs

The key features of an LLP provide the flexibility of a partnership with the protection of a company:

-

liability - a member’s liability is limited to the amount of money they invest in the business. Their personal assets are protected

-

legal status - an LLP is a separate legal entity that can own property and enter into contracts in its own name

-

management and profits - all members can be involved in the management of the business and share in its profits

-

administration - you must register an LLP with Companies House, file annual accounts, and maintain a central register of people with significant control (PSCs) at Companies House. An LLP agreement is essential for setting out how the business will be run

-

identity verification - all individual members and PSCs of an LLP must verify their identity with Companies House. Corporate members will need to verify their identity at a later date

For more information on setting up an LLP, read How to set up and register a partnership.

Anyone starting an LLP should enter into a written LLP agreement, to clearly manage rights and obligations between the members and prevent potential future disputes.

What is a limited partnership (LP)?

A limited partnership is a structure that has at least one ‘general partner’ and one ‘limited partner’. It is often used for businesses that need to raise capital from outside investors.

Key features of LPs

LPs are defined by their two distinct classes of partners, each with different levels of liability and responsibility:

-

liability - general partners have unlimited liability (ie the general partners can be personally liable for all the partnership's debts), while limited partners have their liability limited to the amount they invest

-

legal status - the business is not legally separate from its owners

-

management and profits - only general partners can manage the business. Limited partners cannot take part in management; if they do, they lose their limited liability status

-

administration - the general partner must register the LP with Companies House

In future, general partners will need to verify their identities with Companies House.

For more information on setting up an LP, read How to set up and register a partnership.

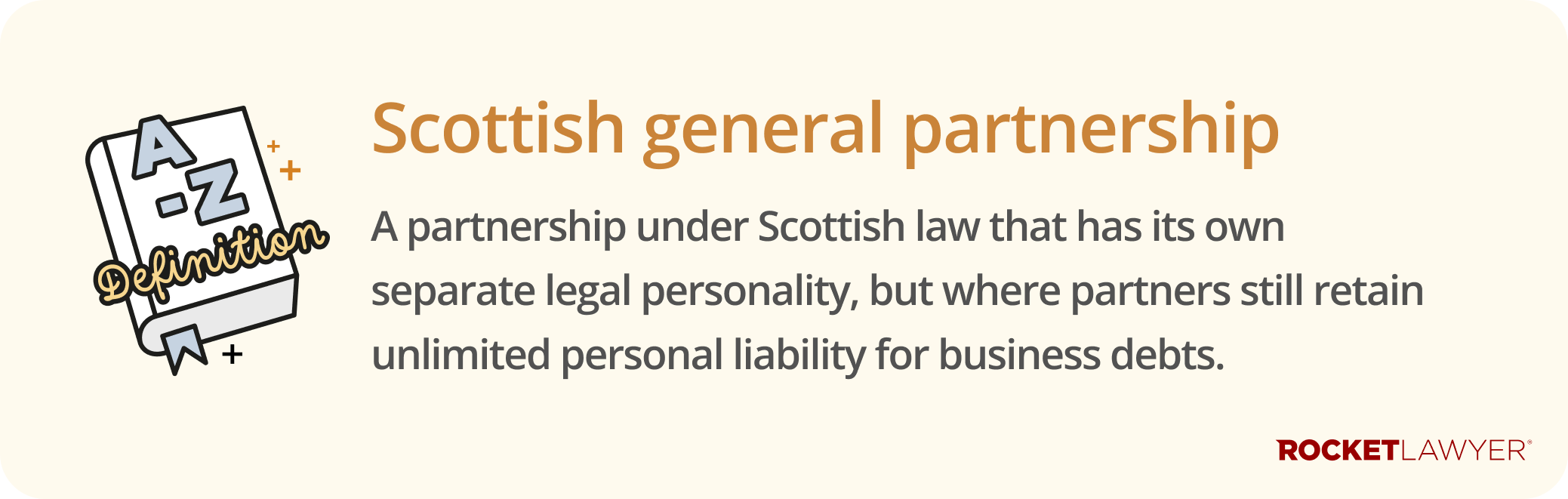

Partnerships in Scotland

Partnerships formed under Scottish law have some unique features, most notably that they are considered to have a separate legal personality from the partners.

Scottish general partnerships

While the process of registering a Scottish general partnership is the same as for general partnerships in England and Wales, the Scottish general partnership has a separate legal personality from the partners. However, partners in a Scottish general partnership still have unlimited liability for the business's debts.

The registration process is the same as for general partnerships in England and Wales, but they may need to be registered with Companies House in certain circumstances (eg where all partners are limited companies).

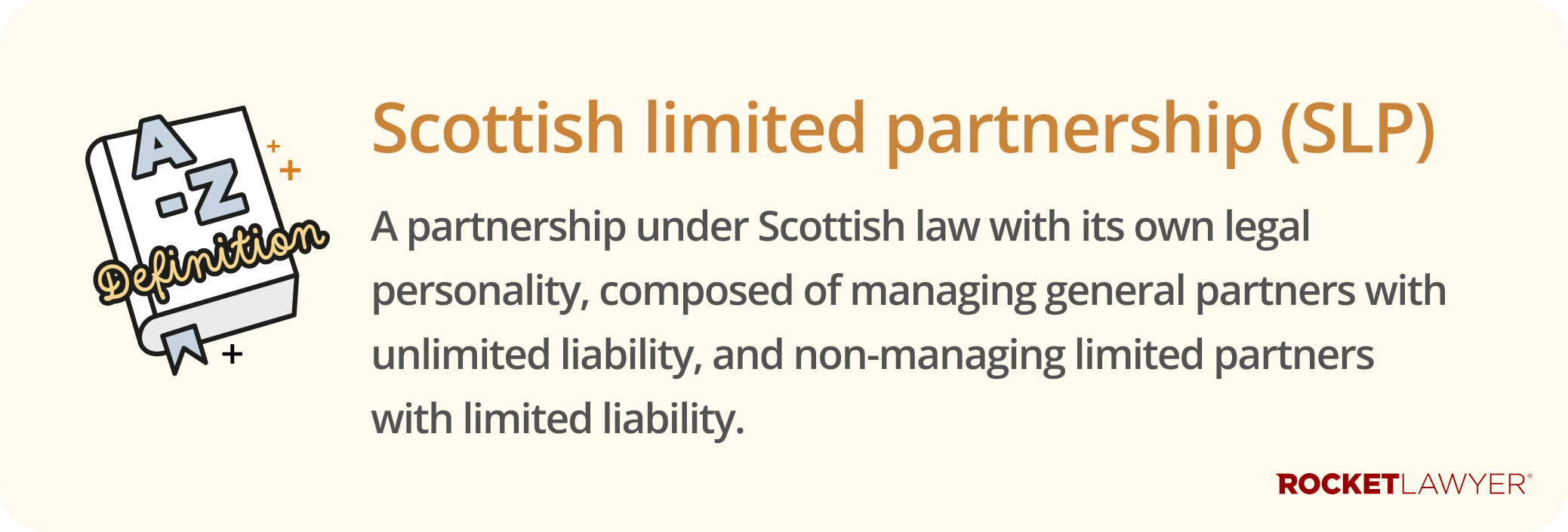

Scottish limited partnerships (SLPs)

An SLP is similar to an LP. Anyone based in Scotland who wishes their primary place of work to be in Scotland can operate as an SLP.

Like an LP, an SLP has a separate legal personality. It consists of one or more general partners with unlimited liability who manage the business, and one or more limited partners with limited liability who cannot be involved in management. SLPs are commonly used in private equity and property investment fund structures.

For more information on setting up partnerships in Scotland, read How to set up and register a partnership.

UK partnership types: at a glance

| Feature | General partnership | Limited partnership (LP) | Limited liability partnership (LLP) |

|---|---|---|---|

| Is the partnership a separate legal entity? | No (except in Scotland) | No (except in Scotland) | Yes |

| Partner liability | Unlimited (personal assets at risk) | Unlimited for general partners. Limited to investment for limited partners |

Limited to investment (personal assets protected) |

| Management | All partners can manage | Only general partners can manage | All members (ie partners) can manage |

| Registration | Partners register with HMRC | Register with Companies House | Register with Companies House |

| Privacy | Accounts are private | Accounts are private | Accounts are public |

| Best for? | Simple businesses, trusted partners, and low-risk ventures | Investment structures with passive investors (ie 'sleeping partners') | Professional services and businesses wanting liability protection |

How to choose the right partnership for you

To find the right structure for your partnership, consider these three questions:

- How much personal risk are you willing to take? If protecting your personal assets is your main priority, an LLP is the strongest choice as it limits your liability. If you are comfortable with unlimited personal liability, a general partnership offers the most simplicity.

- Who will be managing the business? If all partners will be actively involved in the day-to-day running of the business, a general partnership or an LLP is a good fit. If you have passive investors who will contribute capital but have no management role, a limited partnership is designed specifically for this.

- How important is financial privacy? General partnerships and LPs do not need to file public accounts, keeping their financial information confidential. LLPs, however, must file their accounts with Companies House, where they are publicly available.

For more information on how to set up and run these sorts of partnerships, read How to set up and register a partnership. and Running a partnership. Do not hesitat to Ask a lawyer if you have any questions.