Laying the groundwork for your partnership

A successful partnership is built on a strong foundation of mutual understanding. Before any paperwork is filed or registration is completed, all partners should meet to agree on the following fundamental points that will shape your business:

Choose a name for your partnership

Your name is your identity, and there are rules you must follow when picking a name. Your partnership’s name must not:

-

infringe on any existing trade marks and

-

be offensive

-

use 'sensitive' words or expressions

-

suggest a connection with government or local authorities without official permission

-

include ‘limited’, ‘Ltd’, ‘public limited company’, or ‘plc’ (note that only an LLP can include ‘limited liability partnership’ and ‘LLP’ in their name)

Special naming rules may apply depending on the type of partnership you choose.

For more information, read How to choose a name for your business.

Define partner roles

Your partnership will need to appoint partners to specific administrative roles with legal responsibilities.

For a general partnership, you must choose a ‘nominated partner’. This person is formally responsible for the partnership's tax records and returns.

For an LLP, you must appoint at least two ‘designated members’. They have extra legal duties, such as signing the annual accounts, filing documents with Companies House, and ensuring their identity is verified with Companies House.

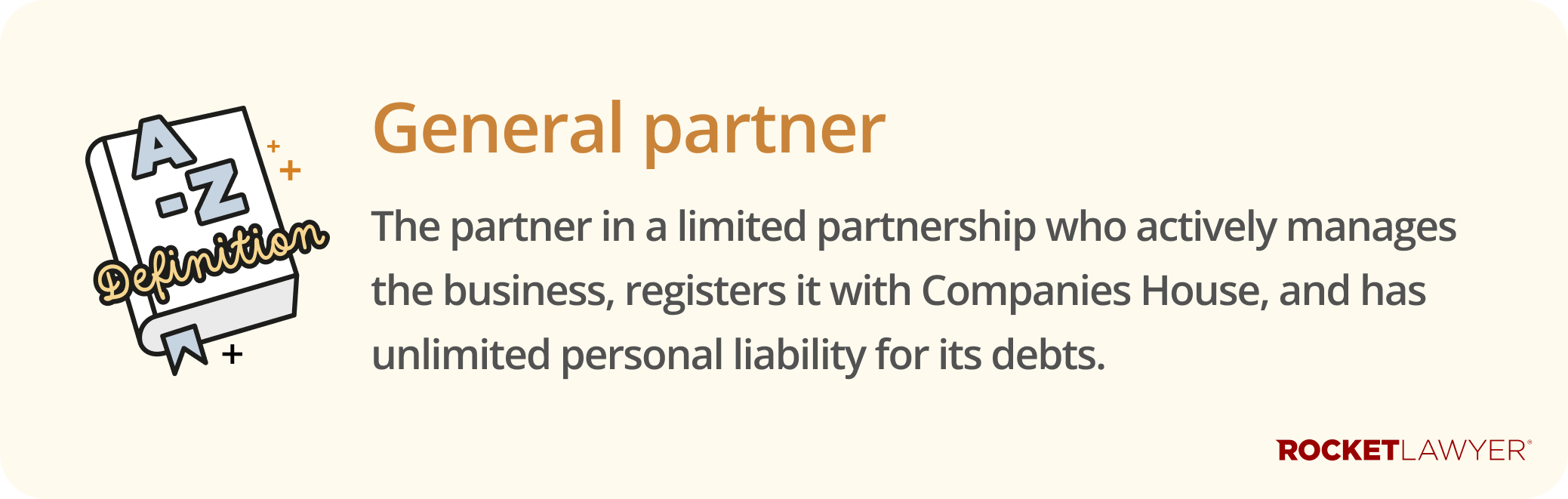

For an LP (or Scottish LP), you must have at least one ‘general partner’ and at least one ‘limited partner’. The general partner has more control over the partnership and has unlimited liability for the partnership’s debts. They are also responsible for registering the partnership with Companies House and submitting any additional filings if necessary.

The limited partner contributes capital (ie money or property) to the LP when it is initially set up. Their liability for the partnership debts is limited to the amount they initially contributed. They cannot remove their original contribution from the partnership, nor can they manage it.

Agree on the core terms

This is the most important conversation you will have as new business partners. You should discuss and agree on the essential terms of your relationship, including how much capital each partner is contributing, each person's ownership stake and salary, the principal duties of each partner, the procedures for admitting a new partner or handling the departure of an existing partner, and the precise method for sharing profits and losses.

All agreed-upon terms should be recorded in writing in a Partnership agreement or LLP agreement.

Setting up a general partnership

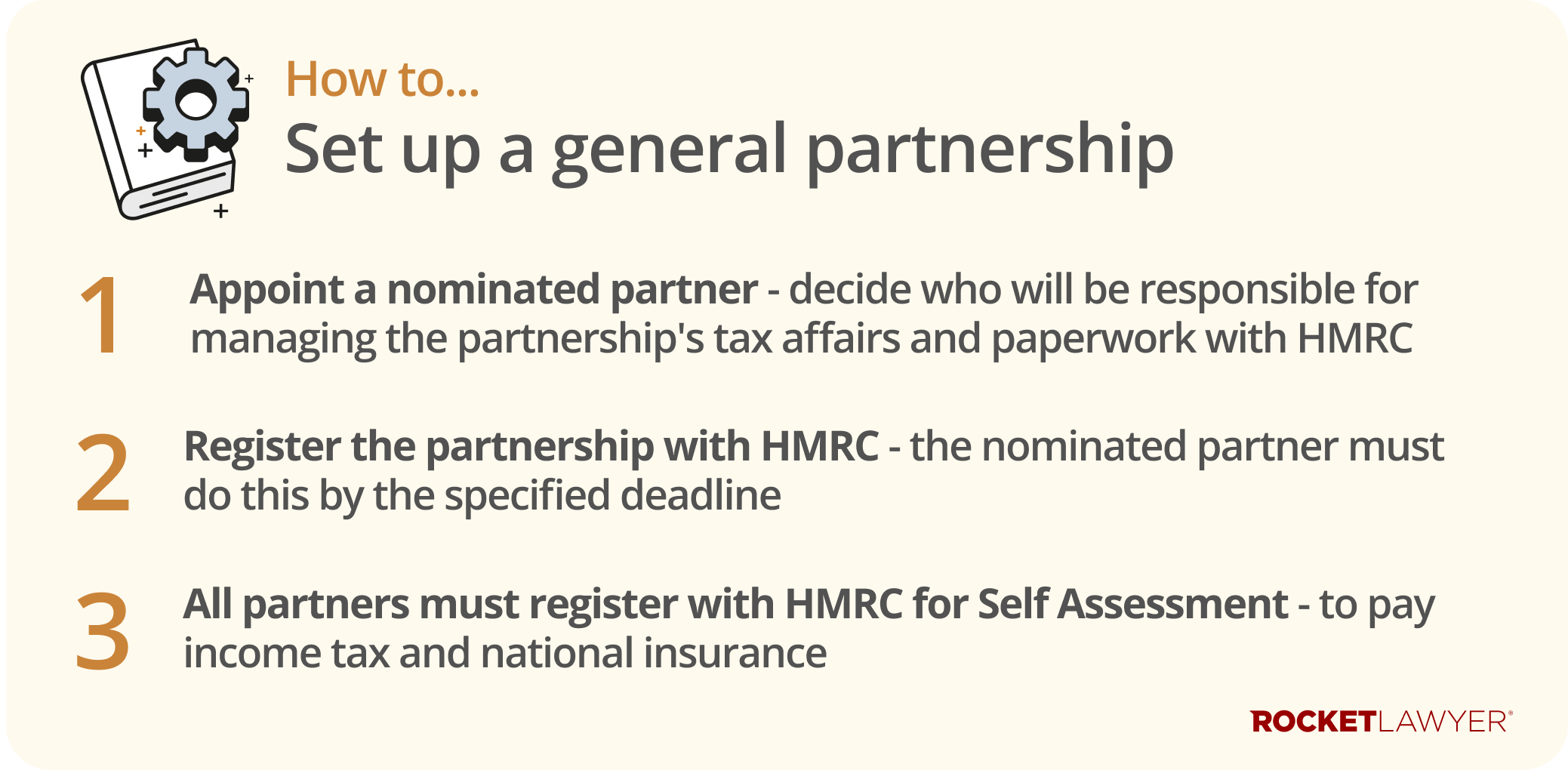

A general partnership is the most straightforward partnership structure to set up, and it does not need to be registered with Companies House. The process focuses on ensuring each partner and partnership is correctly registered for tax with HMRC. To set up your ordinary partnership, follow these steps:

1. Appoint a nominated partner

You must formally decide which partner will take on the legal responsibility for managing the partnership's tax affairs with HMRC. While this partner handles the paperwork, all partners remain jointly responsible for the debts.

2. Register the partnership

The nominated partner must register the partnership for Self Assessment with HMRC. This can be done online or using Form SA400. The deadline for registration is usually 5 October in your partnership’s second tax year.

3. All partners must register for Self Assessment

This is a crucial individual responsibility. Every partner, including the nominated partner, must register with HMRC for Self Assessment to pay income tax (at the applicable rates in England, Wales, and Scotland) and National Insurance on their share of the partnership's profits. This can be done online or using Form SA401.

If a general partnership only has partners who are corporate bodies (eg partners who are private limited companies), it becomes a qualifying partnership (QP). QPs are subject to more stringent reporting requirements. Similarly, general partnerships registered in Scotland that only have corporate-body partners become Scottish qualifying partnerships (SQPs), which are subject to more stringent reporting requirements. For more information, read Running a partnership.

Setting up a limited liability partnership (LLP)

Setting up an LLP is a more formal process involving creating a distinct legal entity. The steps are centred around registering the business with Companies House, which provides the partners with the protection of limited liability. To set up your LLP, follow these steps:

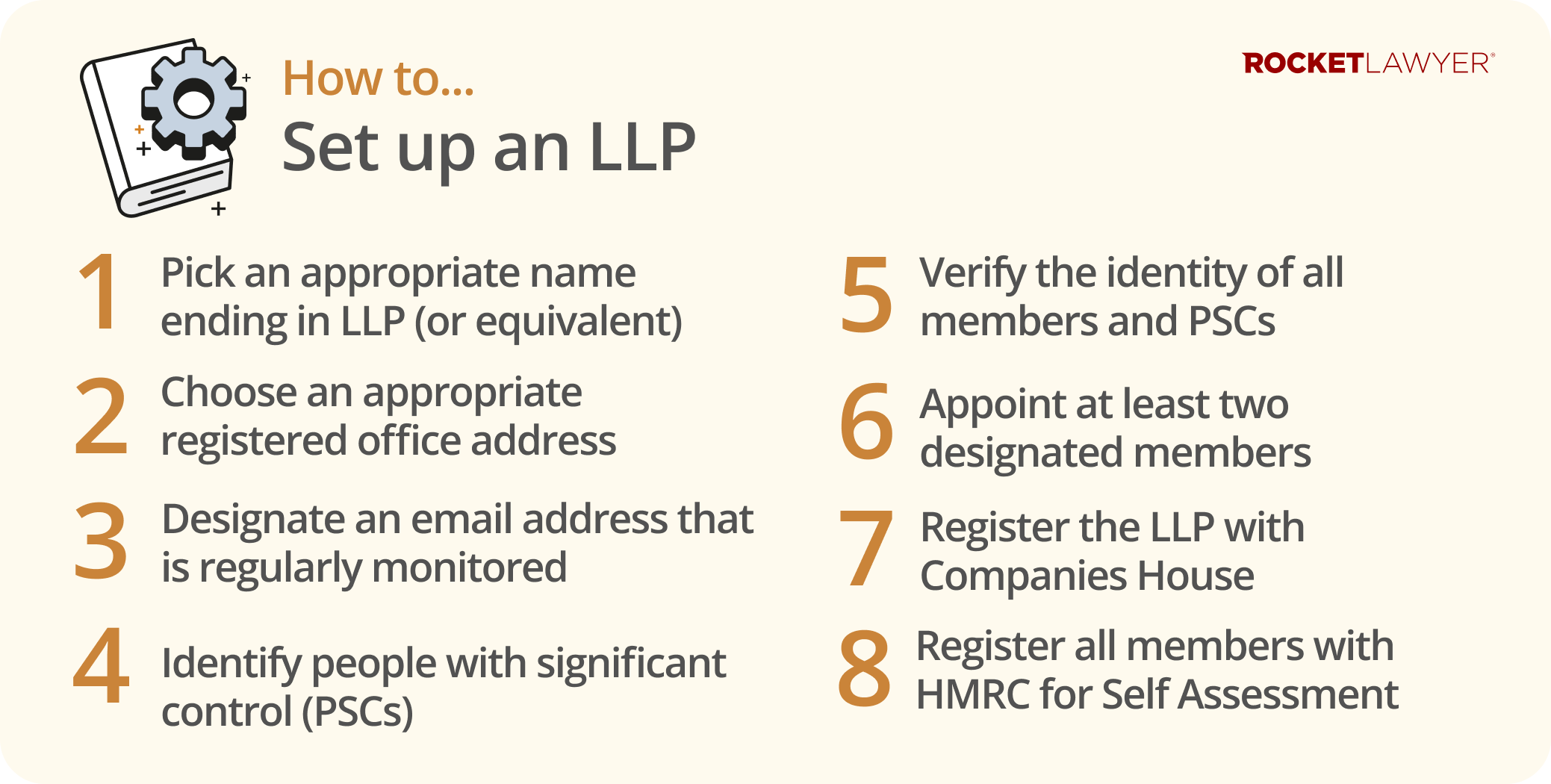

1. Choose a name for your LLP

You must decide on a name for your LLP. This must end in ‘limited liability partnership’ or ‘LLP’. LLPs registered in Wales can also use the Welsh equivalents (‘partneriaeth atebolrwydd cyfyngedig’ or ‘PAC’).

Remember to comply with all other rules about naming your business.

2. Decide on an office address for your LLP

When setting up your LLP, you must provide an ‘appropriate’ registered office address. This must be a physical address in the same country your LLP is registered in (eg England or Scotland) and will be on the public record (so be mindful about using your home address).

The address must be effective for receiving official correspondence. Any document delivered there must be expected to come to the attention of someone acting for the LLP, and recorded or signed-for deliveries must be possible. A PO Box (or equivalent) cannot be used as your registered address.

3. Decide on an email address for your LLP

You must also provide an official registered email address. This needs to be an active account that is regularly monitored by a member or someone acting on behalf of the LLP, to ensure that important communications from Companies House are received promptly. Unlike your registered office address, this email address is not made public.

4. Identify people with significant control (PSCs)

Every LLP must identify its people with significant control (PSCs) and maintain a record of these PSCs with Companies House. A PSC is someone who ultimately owns or controls the partnership. An individual or legal entity (eg a company) that meets one or more conditions relating to ownership or control is normally considered a PSC. For an LLP, this usually means they:

-

hold the right to share in more than 25% of the surplus assets on the winding up of the LLP

-

hold more than 25% of the voting rights

-

have the right to appoint or remove a majority of the designated members

-

otherwise exercise significant influence or control

5. Verify the identity of members and PSCs

From 18 November 2025, all individual members and all individual PSCs must verify their identity with Companies House. You cannot successfully register the LLP until all initial individual members and PSCs have completed this verification process. For more information on the process, read Company roles and appointments.

6. Appoint at least two designated members

An LLP must have at least two members who are appointed as 'designated members' at all times. If you don't specify who they are, all members will be considered designated members. They have additional legal responsibilities for filing documents and notifications with Companies House, and each individual member and PSC must verify their identity with Companies House. They are also responsible for registering the LLP for VAT if applicable.

7. Register the LLP with Companies House

This is the formal step that brings the LLP into legal existence. The designated members can register online or by post using Form LLIN01. You must include information on the LLP's PSCs for the central register, and the application will only be approved if all initial individual members and PSCs have verified their identity.

Once approved, Companies House will issue a certificate of incorporation, and your LLP is legally registered.

Use our Business registration service to register your LLP for free.

Once approved, Companies House will issue a certificate of incorporation, and your LLP is legally registered.

Note that LLPs will automatically be registered for Self Assessment from their Companies House registration.

8. All members must register for Self Assessment

All members must register themselves with HMRC for Self Assessment to pay income tax (at the applicable rates in England, Wales, and Scotland) and National Insurance on their share of the partnership's profits. This can be done online or using Form SA401.

Setting up a limited partnership

A limited partnership also requires formal registration with Companies House. The setup process focuses on legally defining the distinct roles and liability levels of the ‘general partners’ who manage the business and the ‘limited partners’ who are passive investors. To set up your LP, follow these steps:

1. Decide on the general and limited partners

You must have at least one ‘general partner’, and at least one ‘limited partner’. The general partner has more control and responsibilities than the limited partner.

Amongst other things, the general partner:

-

is liable for any debts the business cannot pay

-

has control over and manages the LP

-

can make binding decisions on behalf of the LP

-

is responsible for registering the LP with Companies House, for Self Assessment, and for VAT if applicable

The limited partner, on the other hand, has fewer powers and responsibilities. They:

-

contribute an amount of money or property to the LP when it’s initially set up

-

are only liable for debts up to the amount they initially contributed

-

cannot manage the business

-

cannot remove their original contribution

2. Choose a name for your LP

You must decide on a name for your LP. This must end in ‘limited partnership’ or ‘LP’. LPs registered in Wales can also use the Welsh equivalents (‘partneriaeth cyfyngedig’ or ‘PC’).

Remember to comply with all other rules about naming your business.

3. Establish a principal place of business

To run an LP, you must have a registered address. This is also known as the ‘principal place of business’ and is where all official communications about your LP are sent. Your registered address must be:

-

a physical address

-

your main place of business

-

in the same country that your LP is registered in. Note that once your LLP is incorporated, you can move anywhere in the UK

Bear in mind that the registered address will be publicly available, so you may not wish to use your home address.

4. Register the LP with Companies House

The general partner must register the LP with Companies House. This can be done using Form LP5, which must be signed by all partners.

LPs will automatically be registered for Self Assessment from their Companies House registration.

If an LP only has general partners who are corporate bodies, it becomes a qualifying partnership and will be subject to more stringent reporting requirements. For more information, read Running a partnership.

Note that although LLPs are currently the only entities required to comply with identity verification, the same rule will apply to individual general partners of LPs on a future date that hasn't been specified yet.

5. All partners must register for Self Assessment

All partners must register themselves with HMRC for Self Assessment to pay income tax (at the applicable rates in England, Wales, and Scotland) and National Insurance on their share of the partnership's profits. This can be done online or using Form SA401.

Setting up a Scottish limited partnership (SLP or Scottish LP)

The process for setting up an SLP is similar to that of an LP but uses Scotland-specific forms and must be registered with Companies House in Edinburgh. It is vital that the legal agreements are governed by Scottish law. As indicated by their name, SLPs are only available for businesses based in Scotland that wish for their primary place of work to be in Scotland.

To set up your SLP, follow these steps:

1. Decide on the general and limited partners

As with a standard LP, you must appoint at least one ‘general partner’ who has unlimited liability and manages the business, and at least one ‘limited partner’ whose liability is limited to their investment.

2. Choose a name for the partnership

The name you choose must end with the words ‘limited partnership’ or the abbreviation ‘LP’.

3. Establish a principal place of business

You must provide an official address in Scotland for the SLP. All official correspondence will be sent here, and it will be part of the public record.

4. Register the SLP with Companies House

The general partner must register the SLP with Companies House in Edinburgh. This can be done using Form LP5(s), which must be signed by all partners.

This form requires you to provide key details, including the firm's name, business nature, partner details, and, most importantly, a statement of initial significant control, which contains your SLP’s PSC information. For more information on who qualifies as a PSC, see the government’s guidance on PSCs for SLPs.

The SLP legally comes into existence once your application is accepted and registered, at which point Companies House will issue a certificate of registration.

Note that SLPs will be automatically registered for Self Assessment through their Companies House registration.

Note that although LLPs are currently the only entities required to comply with identity verification, the same rule will apply to individual general partners of SLPs on a future date that hasn't been specified yet.

5. All partners must register for Self Assessment

All partners must register themselves with HMRC for Self Assessment to pay income tax and National Insurance on their share of the partnership's profits. This can be done online or using Form SA401.

For more information on the different types of partnerships, read Types of partnership. If you have any questions, do not hesitate to Ask a lawyer.