What are tips, troncs, and service charges?

These three things make up the UK’s complex gratuity system, ie the way in which customers within the hospitality industry express their gratitude after receiving good service.

What are tips?

What is a service charge?

Service charges are charges that are commonly added to customers’ bills in hospitality establishments (eg restaurants). Service charges are usually expressed as a percentage of the relevant bill (eg 12.5% of the total amount due), recognising the value of the service a customer has received.

Service charges can be either mandatory or optional. When a service charge is optional (ie voluntary), a customer does not have to pay it. However, it’s often assumed that a customer will pay an optional service charge that’s been added to their bill except in rare circumstances. They can request that a service charge be removed if, for example, they felt they received extremely poor service. A mandatory (ie compulsory) service charge may be added to a bill if this service charge and its compulsory nature has been clearly communicated to the customer before they commit to a purchase (ie this charge will form part of the contract of purchase). A customer must pay a compulsory service charge (unless they do not receive what they’ve been promised. For example, if they’re kicked out of a restaurant before receiving any service).

Note that the customs surrounding service charges vary somewhat throughout the UK. For example, in some cities, automatically adding a service charge to a bill would be considered unusual.

How are service charges different to tips?

The line between service charges and tips is not clear-cut. For many purposes (eg tax purposes), voluntary service charges are simply considered tips that are suggested on people’s bills. Mandatory service charges are, for most purposes, not considered tips, but rather payments made in exchange for services purchased.

What is tronc?

A tronc (or ‘tronc system’) is a system under which tips and service charges are collected and then distributed to staff members by a third party (ie not their employer). This third party, often referred to as the ‘troncmaster’, may be an employee of the business or an independent outsider.

A tronc will often have its own tip distribution rules that are independent of the employer. Using a tronc system allows tips and service charges to be allocated efficiently to staff members, usually with fewer tax liabilities than are applicable to tips paid out directly by the employer.

For more information on operating a tronc, see HMRC’s guidance on tips, gratuities, service charges, and troncs.

Can tips or service charges make up a worker’s wage?

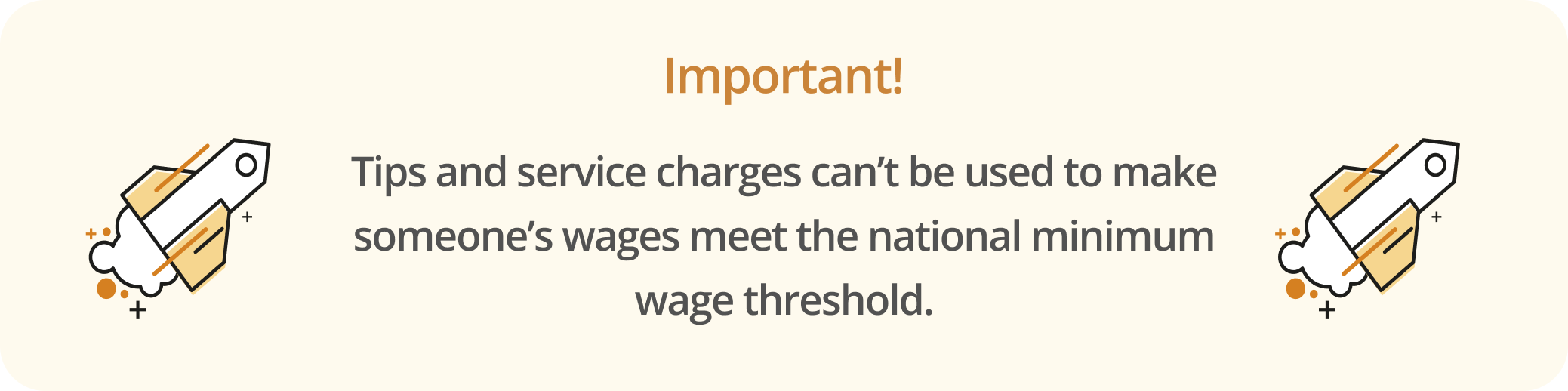

The National Minimum Wage Regulations 2015 prohibit tips and service charges from being used to bring a worker’s or employee’s wage (or salary) up to national minimum wage (NMW) level. This means that all workers and employees must be paid at least the minimum wage (as applicable to their age group) and any money they’re paid that’s from tips or service charges must be in addition to this minimum amount. This applies regardless of how the tips and services charges are collected (eg either via tronc or outside of a tronc system).

What are the new laws applicable to tips?

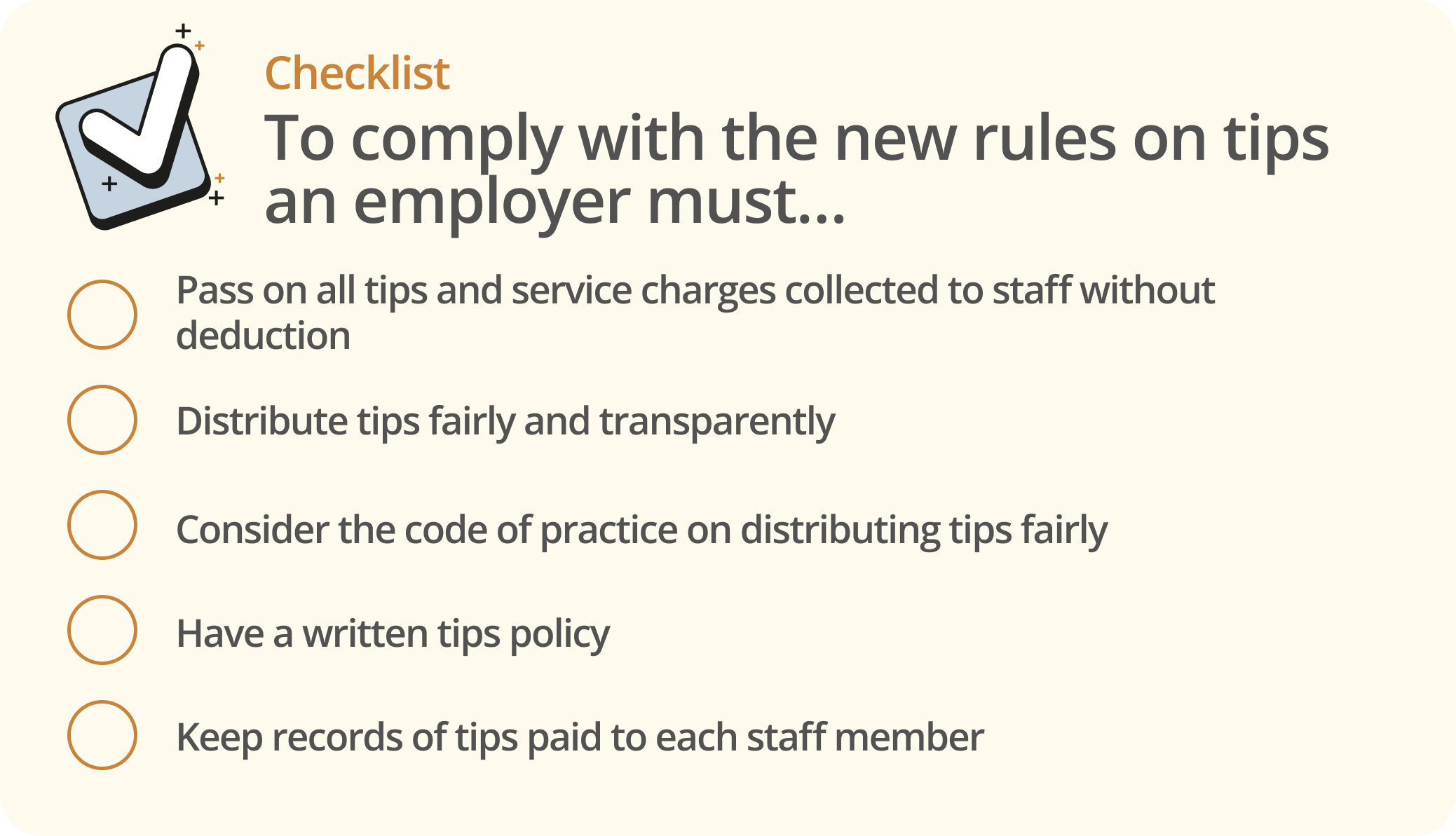

The Employment (Allocation of Tips) Act 2023 came into force on 1 October 2024. The Act introduces new rules that employers must follow when dealing with tips in order to increase the transparency of the gratuity system and ensure staff members receive their fair allocation of tips and service charges.

The Act requires that all tips and service charges collected go to staff members (eg without deductions for administrative costs). However, tax liabilities remain unchanged, and deductions for income tax purposes are still permitted.

Employers must ensure that all ‘qualifying tips’ are allocated fairly between staff members. Qualifying tips are tips and service charges that are received by the employer (eg paid by debit card when a bill is paid) or which, despite being received by a staff member, are under the employer’s control (eg due to provisions in their Employment contract). This will be assumed to have been done when tips are allocated via a fairly used tronc system.

When managing tip distribution, an employer must also have regard to the government’s statutory code of practice on distributing tips fairly.

Businesses who take in qualifying tips on ‘more than an occasional and exceptional basis’ will also have to:

-

provide a written policy setting out how they deal with tips and service charges, including how they’re allocated in line with the requirements of the Act. This policy must be made available to all staff members

-

keep written records of the amount of tips and service charge payments they’ve accrued and how these have been allocated (including via tronc). These records must be kept for three years and aspects of them must be made available to staff members who make written requests

The Act will also introduce harsher penalties and stronger enforcement opportunities for dealing with employers who breach the rules. For example, complaints may be taken to Employment Tribunals.

If you want help creating a tips policy for your business, you can use our Bespoke legal drafting service. Ask a lawyer if you have any questions or concerns about complying with the new laws.

How are tips and service charges taxed?

For tax purposes, mandatory service charges are treated like any other business income (ie income tax and other taxes, like corporation tax, will be due on this income like any other income).

Optional service charges will be treated like other tips. Money received as tips is treated as taxable income on which income tax should be paid. Precisely which tax liabilities are applicable to tips and who is responsible for paying these depends largely on how the tips are collected and processed. For instance:

-

when tips are received directly by a staff member (eg in cash) - these tips are never held by the employer, so the staff member who receives them is responsible for paying any income tax due, either via self-assessment (if the staff member already carries out self-assessment), via a personal tax online account, or directly to HMRC. Income tax will generally be due on these tips unless the earnings are covered by a staff member’s tax allowances

-

when tips are given directly to staff members, then informally pooled between staff members and distributed amongst themselves (eg at the end of a shift) - the amount a staff member receives in this situation is treated the same as other tips given directly to staff members (as set out in the point above)

-

when tips are taken by the employer (either by card or when cash given to staff members is collected) - income tax is due on the amount of these tips later given to staff members, but the employer is responsible for paying the income tax (eg via PAYE)

-

when tips are distributed via a tronc - income tax is due on these payments and the troncmaster is responsible for paying it. They should do under a PAYE scheme that’s independent of the employer’s PAYE scheme

Is National Insurance due on tips and service charges?

Whether National Insurance contributions (NICs) are due on tips or service charges depends on factors like how these payments were collected and whether the employer held (or controlled) them. For instance:

-

when tips are received directly by a staff member (eg in cash) - NICs are not due

-

tips are given directly to staff members, then informally pooled between staff members and distributed amongst themselves (eg at the end of a shift) - the amount a staff member receives in this situation is treated the same as other tips given directly to staff members (as set out in the point above)

-

when tips are taken by the employer (either by card or when cash given to staff members is collected) - NICs are due these as they are on regular wages

-

when tips are distributed via a tronc - whether NICs are due depends on whether the tronc allocates tips according to the employer’s rules or its own rules. If according to the employer’s rules, NICs are usually due; if according to its own rules, NICs are generally not due