What is IR35?

IR35 refers to the UK's off-payroll working rules. These rules apply when a worker or contractor provides their services to a client through an intermediary, rather than as a direct employee.

The purpose of IR35 is to identify disguised employees – individuals who work in a similar way to permanent employees but invoice for their services through their own company to be more tax-efficient.

If a contractor's working relationship with a client would be one of employment were it not for the intermediary, they are considered inside IR35. If this is the case, they must pay income tax and NICs similar to an employee.

If the relationship is genuinely one of self-employment, they are outside IR35.

What is an intermediary?

An intermediary is a party that arranges for or pays an individual to work for a third party (eg the ‘client’ or ‘end-client’). Consultants often provide their services through their own limited company, which is known as a personal service company (PSC).

Even if a consultant doesn't use a PSC and works directly as a sole trader, the client is still responsible for determining their employment status. If a consultant is later deemed to be an employee, the client may be held liable by HMRC for the misclassification.

Who is responsible for determining IR35 status?

For small businesses in the private sector, the responsibility for determining IR35 status remains with the contractor and their PSC. The rules requiring the client to make the determination do not apply.

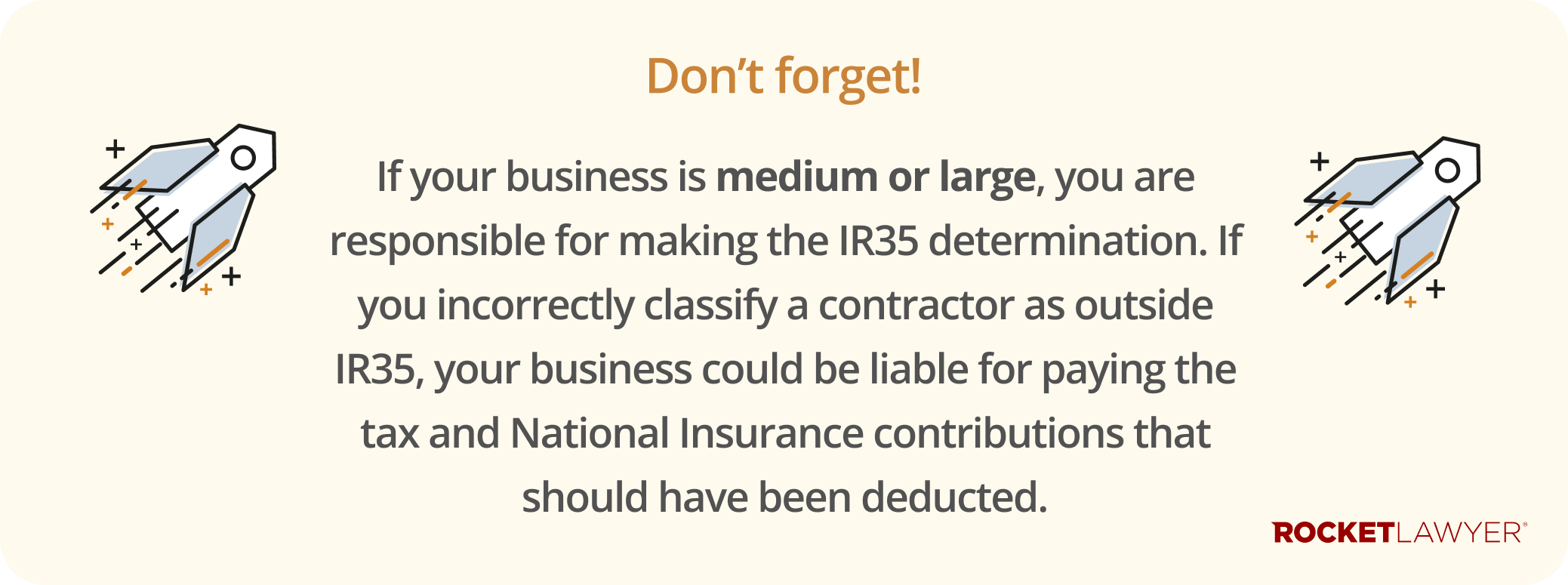

The rule requiring the client to determine status applies to all public sector clients (eg government departments, companies owned or controlled by the public sector, schools, and universities) and to private sector (including some charities) clients that are classed as medium or large. A private sector business is considered medium or large if it meets two or more of the following conditions:

-

it has an annual turnover of more than £10.2 million

-

it has a balance sheet total of more than £5.1 million

-

it has more than 50 employees

What if my company is part of a group?

If your business is part of a larger group, the size test applies to the entire group, not just your individual company. If the group as a whole meets the medium or large criteria, the off-payroll rules will apply to every business within it.

What about recruitment agencies?

If you use a recruitment agency, they are part of the payment chain. For engagements with medium or large clients, the agency is often the fee payer responsible for deducting tax. While this responsibility doesn't apply to small business clients, it's useful to understand the agency's role in the process.

For more information, see the government’s guidance on the off-payroll working rules for agencies and do not hesitate to Ask a lawyer if you have any questions.

Overseas engagements

The off-payroll working rules are for UK tax, so location matters. The rules generally don't apply if a client is based wholly overseas with no UK connection. Similarly, if a contractor you engage is a non-resident and performs all their work outside the UK, they are unlikely to have a UK tax liability under IR35.

How is IR35 status assessed?

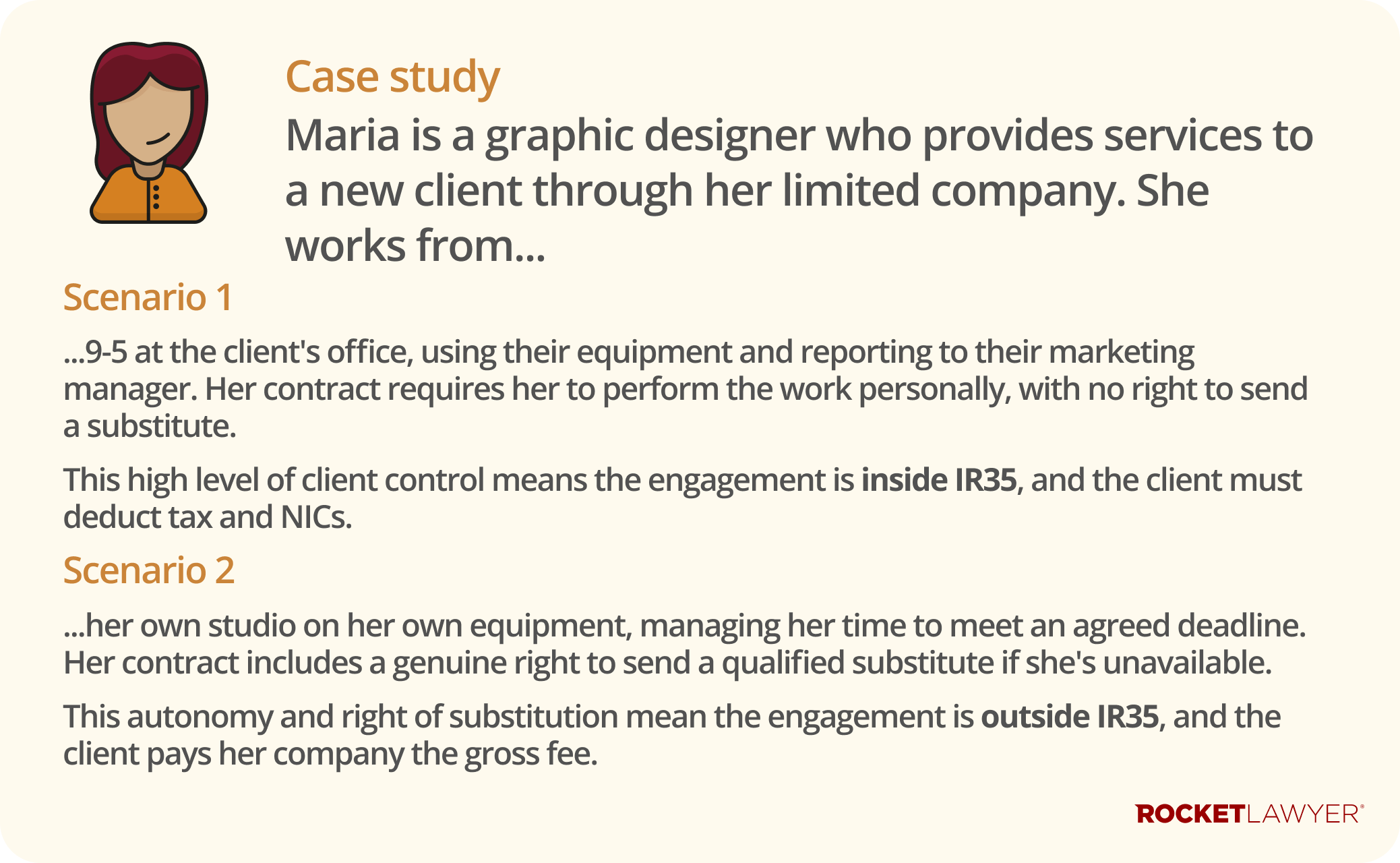

An IR35 assessment determines the worker's true employment status for a specific engagement. This involves looking beyond any written contracts to the reality of the day-to-day working arrangement. The key question is always: ‘Would the worker be considered an employee if the intermediary (eg the PSC) did not exist?’

HMRC's Check Employment Status for Tax (CEST) tool is available online to help with this process. Any assessment, whether using the CEST tool or not, should be based on the following key tests.

How much control does the client have?

This test considers the degree of control the client has over how, when, and where the work is done. If the client directs the worker's daily tasks, sets their working hours, and requires them to work at a specific location, this points towards an employment relationship (ie inside IR35). A genuinely self-employed contractor typically has a high degree of autonomy.

Can the worker send a substitute?

A genuine right of substitution is a strong indicator of self-employment (ie outside IR35). This means the contractor can send another qualified person to complete the work in their place. For the right to be genuine, it must be unrestricted by the client, and the contractor (not the client) must be responsible for paying the substitute. If the worker must provide the service personally, this points towards employment.

Is there a mutuality of obligation (MOO)?

Mutuality of obligation refers to the expectation that the client will continue to offer work and the worker will accept it. This obligation exists in an employment relationship. In a self-employed engagement, the client is not obliged to offer further work once a project is complete, and the contractor is not obliged to accept it. A lack of MOO is a strong indicator of being outside IR35.

Other factors

Other important questions to consider include:

-

who takes on the financial risk? A self-employed contractor typically bears financial risks (eg correcting their own errors at their own cost), while employees do not

-

is the worker part of the organisation? If a worker is integrated into the client's business (eg they have a company email or manage staff), this points towards employment

-

who provides the equipment? A contractor using their own significant equipment is a strong indicator of self-employment, whereas a client providing the tools suggests employment

For more information, including on other considerations, read IR35 status determination.

What is the status determination process?

Once the key factors have been assessed, a determination must be made. The required process and responsibilities depend on the size of the end-client.

For medium and large clients

If you are a medium or large business engaging a contractor, you are legally required to follow a formal process:

-

take reasonable care - you must take care when making your determination. Simply using a tool without considering the specific facts of an engagement is not enough

-

issue an IR35 status determination statement (SDS) - you must provide a formal written statement to the contractor (and the agency you contract with, if relevant). The SDS must state your decision, whether the engagement falls inside IR35 (meaning the contractor is considered an employee for tax purposes), or outside IR35 (meaning the contractor is considered self-employed for tax purposes), and the reasons for it

-

handle disagreements - you must have a process to handle disputes. If a contractor challenges your SDS, you have 45 days to review your decision and either confirm it with reasons or issue a new one

-

keep records - you must keep detailed records of your determinations, the reasons for them, and any fees paid

For contractors working with small clients

If you are a contractor or PSC providing services to a small business, the responsibility for determining your IR35 status rests with you. While you don't issue a formal SDS to your client, you must still perform due diligence for each engagement:

-

assess your status - you should conduct a thorough assessment for each contract using the same key tests (control, substitution, etc)

-

keep detailed records - it is crucial to keep records of your status decision for each contract and the evidence and reasoning behind it. This will be vital if HMRC ever investigates your tax affairs

-

pay the correct tax - if you determine that your engagement is inside IR35, you are responsible for paying the correct income tax and NICs on your earnings from that contract, often referred to as a 'deemed salary'

Who deducts and pays the tax?

Regardless of who makes the determination, if an engagement is found to be inside IR35, the responsibility for deducting tax and NICs and paying them to HMRC falls to the fee payer. The fee payer is the entity that pays your PSC. In a direct engagement, this may be the client, but if there is an agency in the chain, the agency is often the fee payer.

If you need to formalise your decision, you can make an IR35 status determination statement. If you need help assessing a contractor's status or handling a disagreement, do not hesitate to Ask a lawyer.