MAKE YOUR FREE Promissory Note

What we'll cover

What is a Promissory Note?

A Promissory Note is a legally binding document that records a loan between two parties (it can be one or more businesses or private individuals). Promissory Notes create an unconditional promise to repay all debts and help protect the parties involved by providing a record of the transactions and their repayment terms. The person lending the money is known as the ‘creditor’ or ‘lender’ and the person receiving the money is known as the ‘debtor’ or ‘borrower’.

When should I use a Promissory Note?

Use this Promissory Note when:

-

you want to create a legally enforceable contract for repayment of a sum of money (ie a debt) between yourself (ie the creditor) and the borrower

-

you know who owes the money (eg a private individual or a business)

-

the loan amount and the amount to be repaid are certain

-

the repayment period (ie the time the borrower has to repay the debt) has a fixed start and end date

Sample Promissory Note

The terms in your document will update based on the information you provide

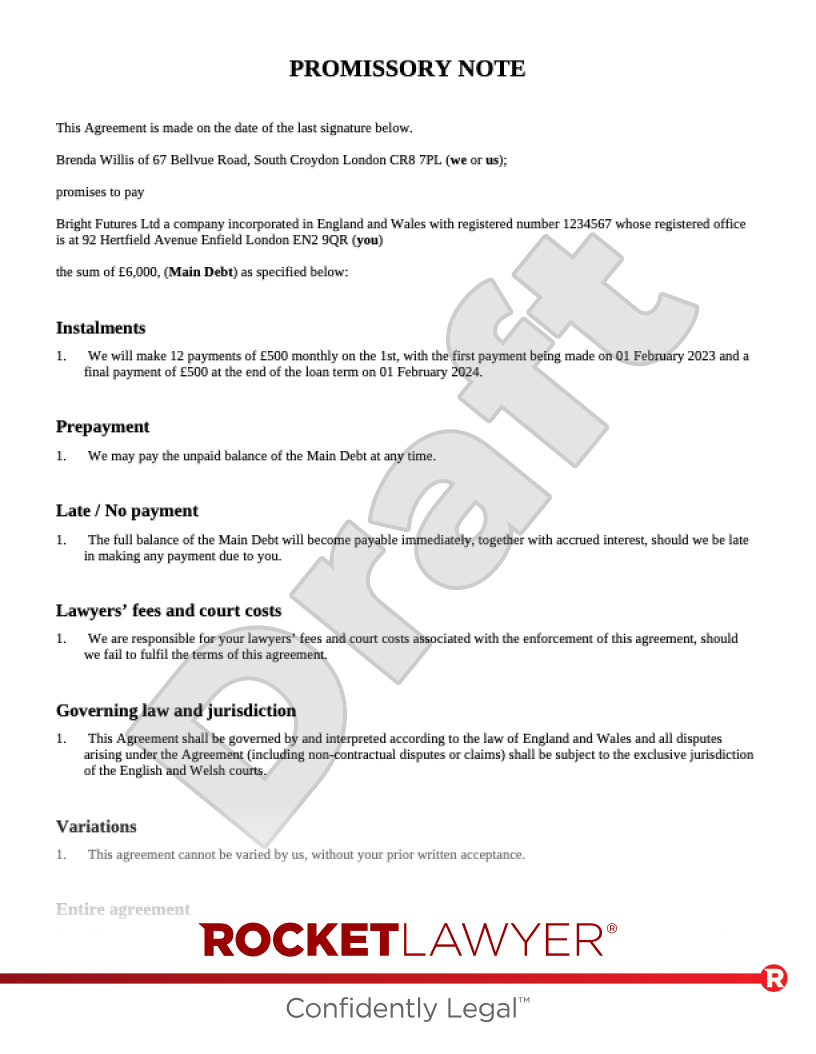

PROMISSORY NOTE

This Agreement is made on the date of the last signature below.

promises to pay

the sum of £, (Main Debt) as specified below:

Prepayment

- We may pay the unpaid balance of the Main Debt at any time.

Late / No payment

- The full balance of the Main Debt will become payable immediately, together with accrued interest, should we be late in making any payment due to you.

Lawyers’ fees and court costs

- We are responsible for your lawyers’ fees and court costs associated with the enforcement of this agreement, should we fail to fulfil the terms of this agreement.

Governing law and jurisdiction

- This Agreement shall be governed by and interpreted according to the law of England and Wales and all disputes arising under the Agreement (including non-contractual disputes or claims) shall be subject to the exclusive jurisdiction of the English and Welsh courts.

Variations

- This agreement cannot be varied by us, without your prior written acceptance.

Entire agreement

- This agreement constitutes the entire agreement between us and overrides other oral or written agreements entered into, concerning this subject matter.

The parties have signed this Agreement the date(s) below:

About Promissory Notes

Learn more about making your Promissory Note

-

How to make a Promissory Note

Making a Promissory Note online is simple. Just answer a few questions and Rocket Lawyer will build your document for you. When you have all of the details prepared in advance, making your document is a quick and easy process.

To make your Promissory Note you will need the following information:

Party details

-

Your (ie the creditor’s) details (eg your legal structure, name and address).

-

If you are a partnership, LLP or company, who will sign the Promissory Note on its behalf?

-

-

The borrower’s details (eg their legal structure, name and address).

-

If the borrower is a partnership, LLP or company, who will sign the Promissory Note on its behalf?

-

Payments

-

What is the total loan amount?

-

In how many instalments will the debt be repaid? What amount are the instalments? Will the instalments be paid weekly, monthly or yearly?

-

If the instalments are paid weekly, on which weekday will they be paid?

-

If the instalments are paid monthly, will they be paid on the 1st, 15th or last day of the month?

-

If the instalments are paid yearly, on what date will they be paid?

-

-

On what date is the first instalment due?

-

On what date is the last instalment due?

-

What is the amount of the last instalment?

Security

-

Is the loan secured? If so, is it secured by:

-

A mortgage?

-

A deed of trust?

-

Other means? If so, by what means is the loan secured?

-

Interest

-

Will interest be claimed on the debt?

-

If so, what is the annual interest rate?

-

Jurisdiction

-

If either party is based in Scotland, will the laws of Scotland or the laws of England and Wales apply to the Promissory Note?

-

-

Common terms in a Promissory Note

A Promissory Note is an IOU whereby a creditor lends money to a business or private individual. As Promissory Notes are essentially legally binding promises, they will typically include sections on:

Party details

This section sets out the details of the creditor (referred to throughout the Promissory Note as ‘you’) and the borrower (referred to throughout the Promissory Note as ‘we’ or ‘us’) and the borrower’s promise to repay the sum borrowed in line with the terms of the Note.

Interest

If interest is payable, this section sets out the yearly interest rate for the sum borrowed.

Instalments

This section sets out details relating to the repayment of the sum borrowed. Specifically:

-

the number of instalments and their frequency

-

the amount repayable per instalment

-

when the instalments will be paid

-

the date of the first instalment

-

the date and amount of the last instalment

Application of payments

If interest is payable, this section sets out the yearly interest rate of the sum borrowed.

Prepayment

This section sets out that the borrower may pay the unpaid balance of the borrowed sum at any time (ie before the last instalment date).

Late/no payment

This section sets out that, if the borrower is late repaying the loan or doesn’t pay an instalment, the entire sum becomes payable immediately. This includes all interest accrued on the debt.

Collateral

If the loan is secured, this section sets out that the sum borrowed under this Promissory Note is secured and how (eg by mortgage).

Lawyers’ fees and court costs

This section sets out that the borrower is responsible for the creditor’s lawyers’ fees and court costs, if the borrower fails to fulfil the terms of this Promissory Note.

Governing law and jurisdiction

This section sets out whether the legal system of England and Wales or Scotland must be used to resolve any disputes in relation to this Promissory Note. This means that, if any issues arise under the Promissory Notes, they must be handled with regard to the laws and/or in the courts of either England and Wales or of Scotland. For more information, read Jurisdiction and international contracts.

Variations

This section sets out that the Promissory Note cannot be varied by the borrower without the creditor’s permission. Such permission must be obtained in advance and in writing.

Entire agreement

This section incorporates a boilerplate clause into the Promissory Note, which prevents the borrower and creditor from being liable for anything not expressly set out in this Promissory Note.

If you want your Promissory Note to include further or more detailed provisions, you can edit your document. However, if you do this, you may want a lawyer to review or change the Promissory Note for you, to make sure it complies with all relevant laws and meets your specific needs. Ask a lawyer for assistance.

-

-

Legal tips for making a Promissory Note

Make sure a Promissory Note is the right document for your situation

This Promissory Note should be used for less formal loans, where there are certain levels of trust between the parties and which involve smaller sums of money. Where the loan is larger and involves substantial debts, and/or the parties are not very familiar with one another, a Loan agreement should be used.

Consider whether the Promissory Note requires collateral

Consider the specifics of the borrower’s situation and the sum of money they are borrowing. Depending on the circumstances, you may consider that it is necessary to take security in the form of collateral to ensure the repayment of the loan. You may wish to secure a loan under a Promissory Note if you are unsure as to the borrower’s financial position and you want to ensure that you can recover the money lent.

Consider whether you want to charge interest on the loan

Interest is typically charged by creditors to make the risk attached to lending money (ie the borrower not repaying the borrowed sum) worthwhile. Any interest must be set as an annual percentage (known as interest ‘per annum’ or ‘p/a’). For more information, read Loans between companies and Calculating interest on commercial debt.

Understand when to seek advice from a lawyer

Ask a lawyer for advice:

-

if you want to take security

-

on debt recovery procedures

-

on recovering debt for organisations based outside England, Wales and Scotland

-

if you intend to enter into loans with individuals or small businesses more than merely occasionally, as you may need a credit licence

-

Promissory Note FAQs

-

What is included in a Promissory Note?

This Promissory Note template covers:

-

the parties to the note

-

the amount to be repaid (ie the debt)

-

the date by which the debt is to be repaid

-

whether interest is payable and if so how much

-

other terms and conditions used in contracts for loans

-

-

Why do I need a Promissory Note?

You need a Promissory Note if you want to ensure that a debt will be repaid. Promissory Notes are a form of IOU (‘I Owe You’), an unconditional written promise to repay money owed at a future date. A Promissory Note properly records the transaction and repayment terms and binds the party that owes the money.

-

Are Promissory Notes legally binding?

While Promissory Notes are different to loan agreements, they are legally binding and enforceable. This means that, if the borrower fails to repay the loan, the creditor can take active steps to enforce the Promissory Note and the terms contained within it.

-

What is the difference between a Promissory Notes and an IOU?

Promissory Notes fall between formal loan agreements and more informal IOUs.

IOUs simply acknowledge a debt and the amount the debtor has to repay. An IOU is not legally binding. On the other hand, Promissory Notes include a legally binding promise to repay the debt (by a specified date).

-

What is the difference between a Promissory Note and a loan agreement?

Promissory Notes and Loan agreements set out debt repayment terms and are legally binding documents. The difference between the two is that loan agreements contain more extensive, specific terms and usually include security, whereas Promissory Notes are usually unsecured. Typically, Promissory Notes should be used when the debt is relatively small and a loan agreement should be used when a large debt is owed.

For more information, read Loan agreements and promissory notes.

-

What are the payment options available?

You can choose to set a date when the loan must be repaid or to order the payment in instalments. This Promissory Note allows you to clearly state the time of each instalment and the last date on which the final payment is to be made.

-

When is a loan secured?

A secured loan is a loan secured by a mortgage or trust deed or valuable item. In this Promissory Note, you can choose to secure the loan of money by a collateral agreement (ie a guarantee or security for payment of the loan). For more information, read Unsecured and secured loans.

-

Can I claim interest on the debt?

Yes, this Promissory Note allows you to set out the interest rate and therefore claim contractual interest on the debt. For more information on claiming interest, read Calculating interest on commercial debts.

-

What happens if the borrower fails or is late to repay the debt?

If the borrower fails to or is late to repay the debt, the full balance of the total amount becomes payable immediately. This includes any accrued interest (ie interest due) as set out in the Promissory Note.

-

Can a Promissory Note be signed electronically?

Promissory Notes can be signed electronically.

This Promissory Note can be signed electronically using RocketSign.

For more information on e-signatures, read Electronic signatures.

Our quality guarantee

We guarantee our service is safe and secure, and that properly signed Rocket Lawyer documents are legally enforceable under UK laws.

Need help? No problem!

Ask a question for free or get affordable legal advice from our lawyer.