When should businesses and individuals lend to each other?

There are a wide range of situations where businesses and individuals may want to lend or borrow money from each other instead of going to a financial institution. This method of lending can mean increased flexibility as to terms and fewer formalities needing to be settled before an arrangement is finalised.

Examples of when this type of lending may be appropriate include when a parent company decides to provide funding for one of its subsidiaries during hard times, or when a private individual wishes to help a family member who is setting up a new business and requires some capital investment.

What are loan agreements?

A Loan agreement is a standard type of document that sets out the terms of a loan and its repayment. It should be used whenever a substantial amount of money is involved, particularly if the lender and borrower are not very closely linked or wish to keep things on a more formal footing. This agreement is suitable for all types of small businesses, including companies, partnerships, LLPs, Scottish general partnerships, Scottish limited partnerships (SLPs), and sole traders.

Some of the key terms contained in a loan agreement include:

-

the amount of the loan

-

the date by which it needs to be repaid in full (along with any agreed instalment dates)

-

details of any interest payable.

It’s also possible to add security to a loan, in which case the borrower pledges their assets (such as a house or car) as collateral for the loan. It is recommended to Ask a lawyer for advice if entering into a secured loan, as some of the issues involved can be complex. For more information on secured loans, read Unsecured and secured loans.

What are promissory notes?

A Promissory note is essentially an unconditional written promise to repay a loan or other debts at a fixed or determinable future date.

Although legally enforceable, a promissory note is less formal than a loan agreement and is suitable where smaller sums of money are involved. However, its terms (which can include specific dates for repayment, interest rates, and repayment schedules) are more certain than those of an IOU (‘I owe you’).

In addition to facilitating business-to-business lending, promissory notes can also be used by private individuals who wish to formalise debts and loans between each other.

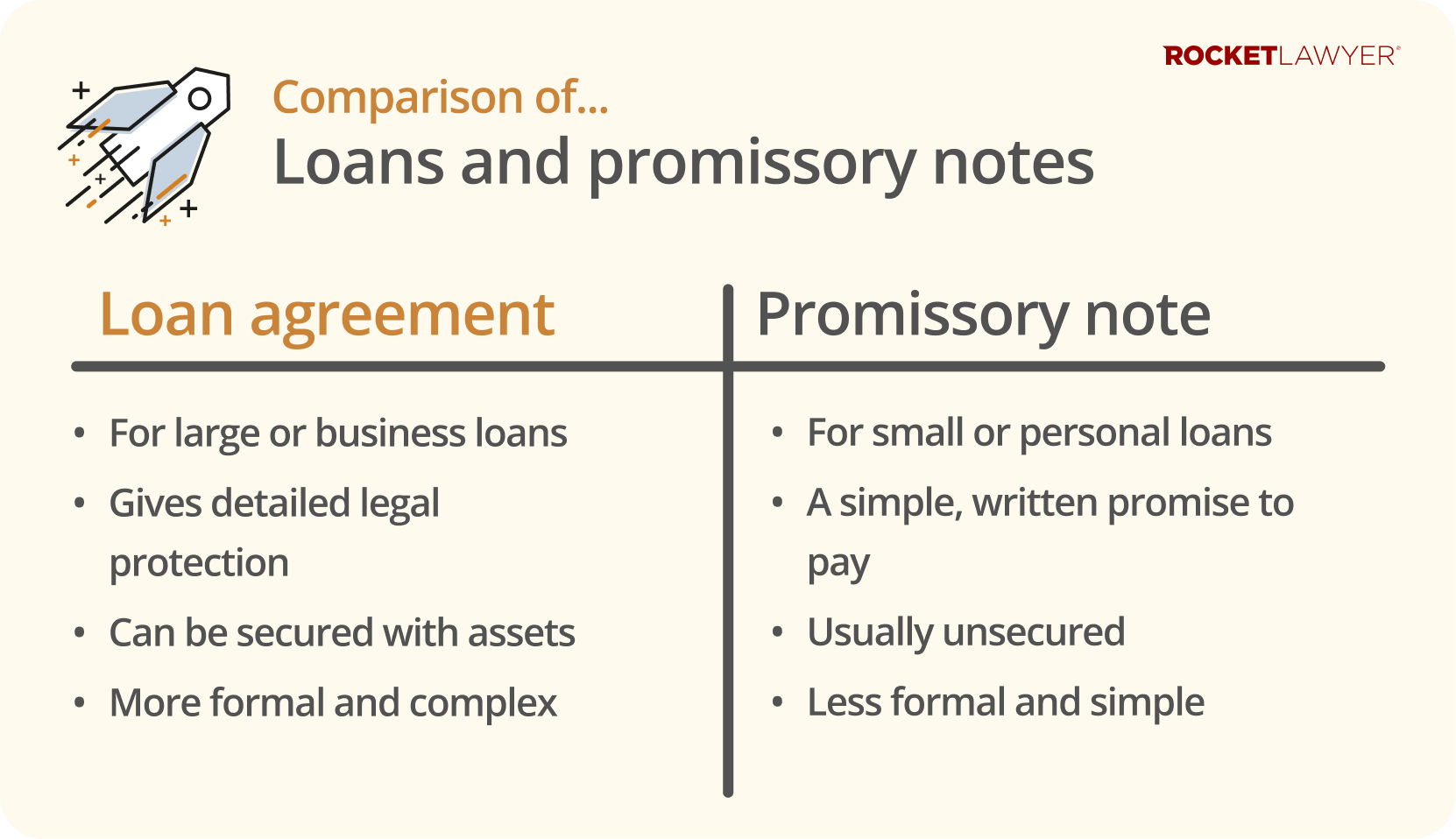

Should I use a loan agreement or a promissory note?

Both loan agreements and promissory notes are legally binding and enforceable documents that set out terms for the repayment of debts. However, a loan agreement normally contains more specific and stringent terms, with greater obligations and restrictions placed on the borrower. It also often includes elements of security (eg putting up a house as collateral), whereas a promissory note is typically unsecured.

As a general rule, if a relatively small amount of money is involved and there is a great deal of trust between the lender and borrower (or ‘debtor’), a promissory note should suffice. However, if there is a substantial debt involved and the two parties are not overly familiar with each other, a loan agreement is more advisable.

A Loan agreement should be used when both parties are businesses or when an individual is loaning money to a business. A Promissory note should be used when both parties are individuals (such as family members or friends).

What are loan notes?

A loan note is a type of debt instrument that businesses use to borrow money, often from multiple investors rather than a single bank. When a business issues loan notes, it is essentially creating a series of certificates that represent a debt it owes to the noteholders. These noteholders then receive regular interest payments until the debt is repaid on a set date.

Loan notes are popular with startups and growing businesses because they offer more flexibility than traditional bank loans. They are often transferable, which means an investor can sell their note to someone else.

Some companies use convertible loan notes, which give the investor the right to turn their debt into shares in the company later on. This can be a useful way to raise capital without immediately giving away equity or needing to pay back a large cash sum.

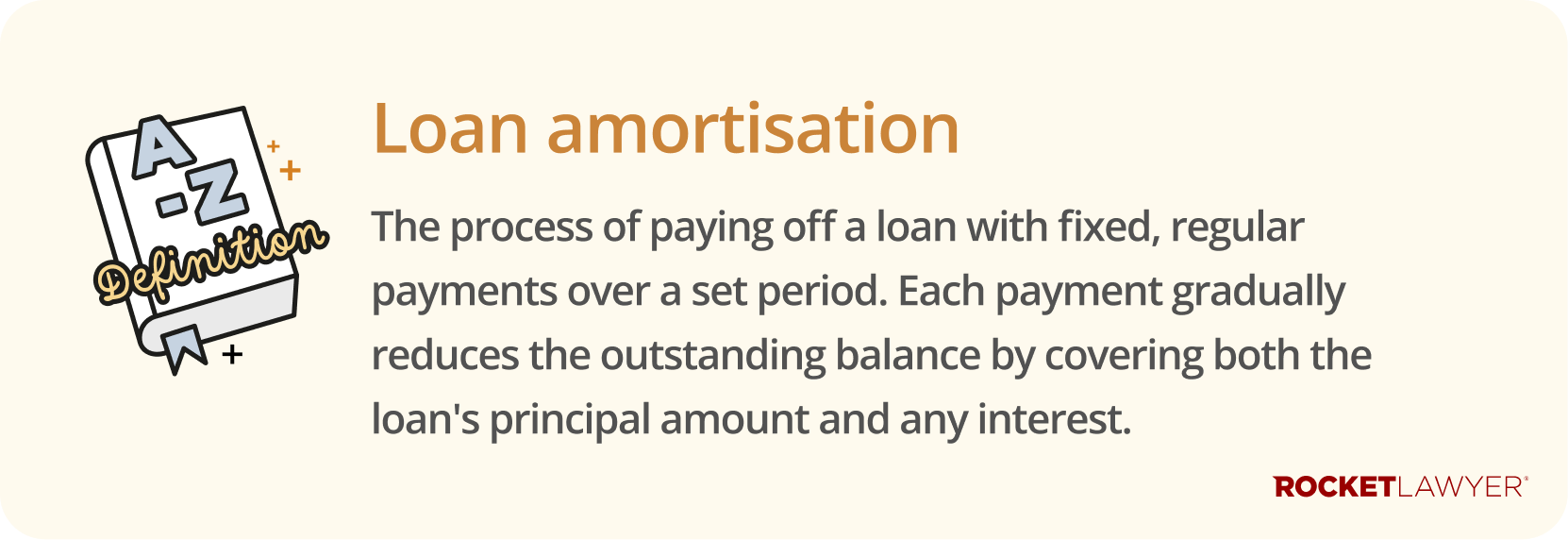

What is loan amortisation?

Amortisation refers to the repayment of the principal amount of a loan ahead of its final maturity date (ie the date on which final repayment is due). Amortising loans generally require the borrower to make repayments on loans on prearranged dates. This will usually be specified in the loan agreement and will be the same amount each time. These are known as amortisation payments.

The required amount of each can be worked out by dividing the total amount by the number of amortisation payments. The amortisation amount may not equal the total amount, and thus, there might be some money due on the maturity date that the borrower will have to pay to satisfy repayment of the loan. This final payment is sometimes called a balloon payment.

For example, you borrow £1,500 on 31 December 2025, with a maturity date of 31 December 2026. On the first of each month, you are required to pay an amortising payment of £100. After 1 December 2026, you will have a £300 outstanding balance, which you will pay as a balloon payment on the maturity date.

What are debentures?

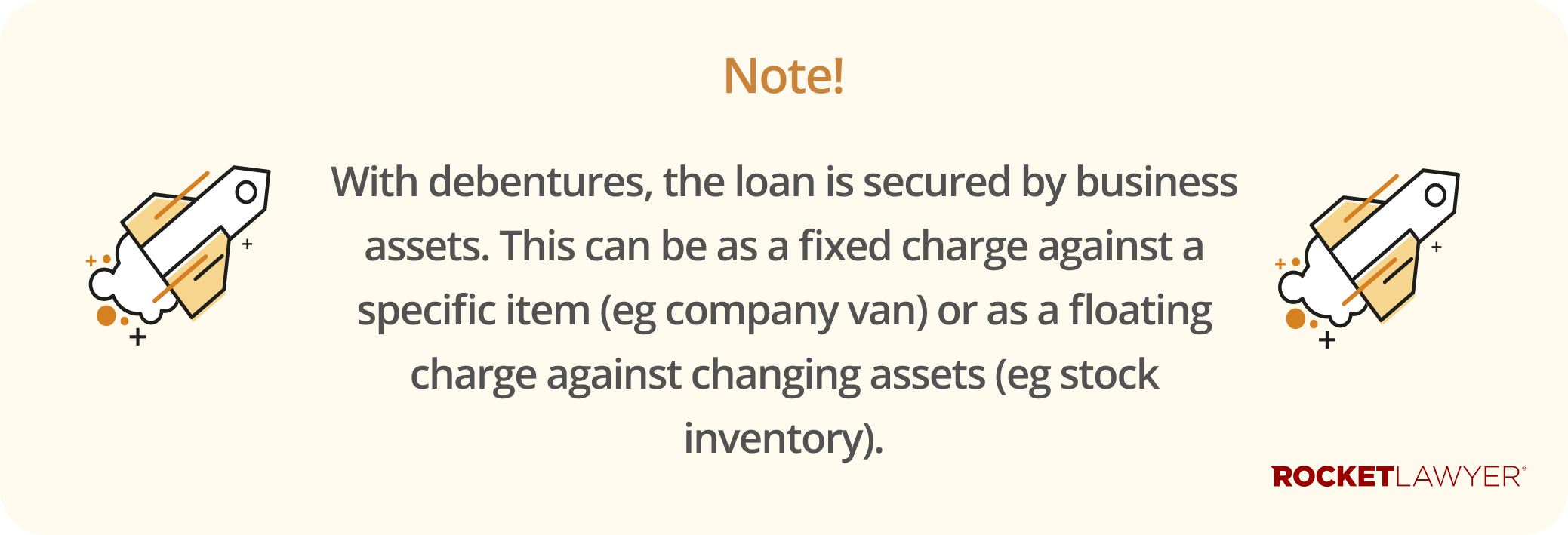

A debenture (also known as a ‘fixed and floating charge’) is another type of written agreement between a lender and a borrower, which is filed at Companies House. A debenture gives the lender security over the assets related to it and prioritises the lender over unsecured creditors in respect of those assets.

If you default on your loan, your lender can claim against your business assets. These can include things such as business laptops and mobile phones, property, and machinery. It doesn’t include any personal property. Once agreed and signed, the debenture must be filed at Companies House within 21 days to be valid. Otherwise, the lender is not prioritised and becomes a regular unsecured creditor.

It’s important to understand the difference between fixed charge and floating charge debentures:

-

fixed charge debentures - the loan is secured against a specific asset such as a car, equipment, or property. If the loan is not paid back, the lender has the right to ownership of that asset

-

floating charge debentures - the loan is secured against an asset with a variable value (eg a business’s inventory). The asset’s value may change during the duration of the loan period. Once the debt is repaid, the borrower regains full control of the asset.

Other types of debentures that you may come across include:

-

secured debentures - the lender leverages a borrower’s assets to provide security against a loan

-

unsecured debentures - these are not secured against any of the borrower’s assets. Unsecured debentures are rare in the UK business environment

-

redeemable debentures - on a specific and agreed date, the borrower is legally bound to repay the lender. This can be done in one lump sum or in instalments over an agreed term (eg a fixed-term loan)

-

irredeemable debentures - there is no specific redemption date, and these debentures continue until the borrower’s company is liquidated (eg a business bank overdraft)

What is a personal guarantee?

A personal guarantee is made between a borrower and a lender. In this agreement, the borrower agrees to be personally responsible for paying back a loan should their business be unable to make repayments.

A personal guarantee provides additional security to the lender. Because of this, the lender may be more willing to agree to the loan. The risk increases for the borrower, who will be personally liable for the debt if the business cannot pay back the loan.

Some examples of when a lender might request a personal guarantee include:

-

invoice finance agreements

-

asset leasing arrangements

-

trade supply arrangements

For more information, read Unsecured and secured loans. If you need to formalise a debt, you can make a Loan agreement or Promissory note, or you can have a bespoke document drafted for your specific needs. Do not hesitate to Ask a lawyer if you have any questions.