MAKE YOUR FREE Asset Purchase Agreement

What we'll cover

What is an Asset Purchase Agreement?

An Asset Purchase Agreement is a contract for the purchase of some of a business’s specific assets, in which the terms of the sale are set out. Asset Purchase Agreements are used to sell a business to another company when the new company intends to continue operating the business.

When should I use an Asset Purchase Agreement?

Use this Asset Purchase Agreement:

-

to buy or sell the assets of a business

-

to formalise an asset sale in a written agreement

-

to impose restrictions on the seller after the asset sale

-

for businesses based in England, Wales, or Scotland

Sample Asset Purchase Agreement

The terms in your document will update based on the information you provide

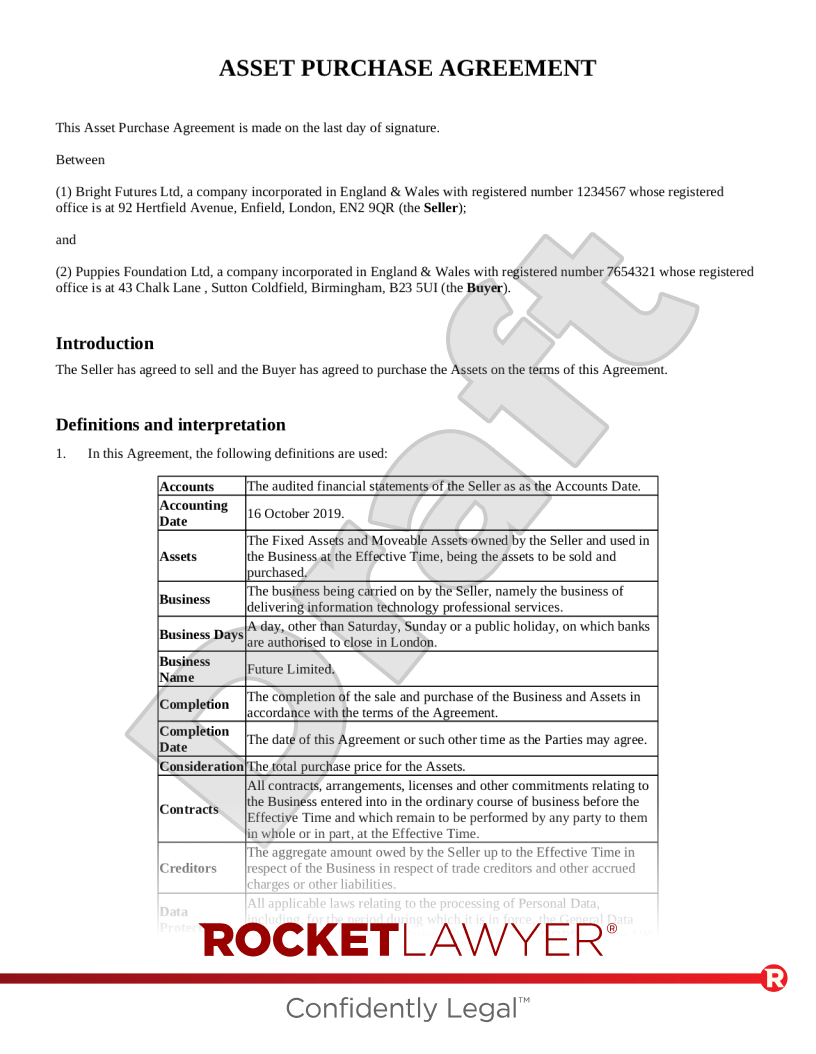

ASSET PURCHASE AGREEMENT

This Asset Purchase Agreement is made on the last day of signature.

Between

(1) , a company incorporated in with registered number whose registered office is at , (the Seller);

and

(2) , a company incorporated in with registered number whose registered office is at , (the Buyer).

Introduction

The Seller has agreed to sell and the Buyer has agreed to purchase the Assets on the terms of this Agreement.

Definitions and Interpretation

- In this Agreement, the following definitions are used:

| Accounts | The audited financial statements of the Seller as as the Accounts Date. |

|---|---|

Accounting Date | . |

Assets | The Fixed Assets and Moveable Assets owned by the Seller and used in the Business at the Effective Time, being the assets to be sold and purchased. |

Business | The business being carried on by the Seller, namely the business of . |

Business Days | A day, other than Saturday, Sunday or a public holiday, on which banks are authorised to close in London. |

Business Name | . |

Completion | The completion of the sale and purchase of the Business and Assets in accordance with the terms of the Agreement. |

Completion Date | The date of this Agreement or such other time as the Parties may agree. |

Consideration | The total purchase price for the Assets. |

Contracts | All contracts, arrangements, licenses and other commitments relating to the Business entered into in the ordinary course of business before the Effective Time and which remain to be performed by any party to them in whole or in part, at the Effective Time. |

Creditors | The aggregate amount owed by the Seller up to the Effective Time in respect of the Business in respect of trade creditors and other accrued charges or other liabilities. |

Data Protection Laws | All applicable laws relating to the processing of Personal Data, including, for the period during which it is in force, the General Data Protection Regulation (Regulation (EU) 2016/679) (GDPR) and the UK Data Protection Act 2018. |

Disclosure Letter | The letter from the Seller to the Buyer in agreed form, with the same date as this Agreement and described as the Disclosure Letter. |

Domain Names | All internet domain names used or owned by the Seller in connection with the Business. |

Effective Time | . |

Employees | The persons employed wholly or mainly in the Business at the Effective Time. |

Fixed Assets | All of the fixed plant and machinery, furniture, utensils, templates, tooling, implements, chattels and equipment wherever situated belonging to the Seller and used or intended for use in connection with the Business attached or fixed to the property as at the Effective Time. |

Goodwill | The goodwill, custom and connection of the Seller in relation to the Business, together with the exclusive right to use the Business Name, the Domain Names and the Website, telephone numbers, facsimile numbers and any other contact numbers reasonably required by the Buyer. |

Intellectual Property Rights | All trademarks, database rights, names, designs, copyrights, confidential information, customer databases, know-how, software, confidential information, trade or business secrets and any similar rights, whether registered or unregistered, used or licensed by or to the Seller. |

IT System | All computer hardware and software (including associated preparatory materials, user manuals and other related documentation) owned, used, leased or licensed by the Seller in relation to the Business. |

Liabilities | The liabilities of the Seller arising in the ordinary course in connection with the Business outstanding at the Effective Time. |

Moveable Assets | The loose plant, including moveable plant, machinery and equipment, fixtures and fittings, desktop computers, office equipment, spare parts and tooling used or intended for use in connection with the Business. |

Properties | The freehold properties and the leasehold properties set out in Schedule 1. |

Records | The books, accounts (including VAT records and returns), lists of customers and suppliers and all other documents, papers and records relating to the Business or any of the Assets. |

TUPE | Transfer of Undertakings (Protection of Employment) Regulations 2006. |

VAT | Value added tax chargeable under VATA 1994 and any similar replacement or additional tax. |

VATA 1994 | Value Added Tax Act 1994. |

Warranties | The warranties set out in Schedule 2. “Warranty” means any one of them. |

Website | The Seller’s website is to be found at . |

- In this Agreement, unless the context means a different interpretation is needed:

- including means “including without limitation”;

- words denoting the singular include the plural and vice versa and words denoting one gender includes all genders;

- reference to a Section, paragraph or Schedule of or to this Agreement (and the Schedules form part of this Agreement);

- reference to a statute or statutory provision includes any modification of or amendment to it, and all statutory instruments or orders made under it;

- reference to the time of day is to a time in London; and

- reference to writing or written includes faxes and email but not any other type of electronic communication.

- The headings in this document are for convenience only and do not affect the interpretation of this Agreement.

Agreement to Sell and Purchase

- Upon the terms of this Agreement and in order that the Business is transferred as a going concern, the Seller sells and assigns with title guarantee and the Buyer purchases with effect from and as at the Transfer the following Assets of the Seller:

- the Moveable Assets;

- the Fixed Assets;

- the right to use the Business Name;

- the Intellectual Property; and

- the Goodwill.

Consideration

- The total Consideration payable by the Buyer to the Seller for the Business (comprising the Assets) pursuant to this Agreement shall be £ UK pounds (the Purchase Price).

VAT

- The Consideration is exclusive of all and any VAT which may be payable.

- The parties intend that section 49(1) of VATA 1994 and paragraph 5 of the Value Added Tax (Special Provisions) Order 1995 shall apply to the transfer of the Assets under this Agreement.

- The parties consider and shall use all reasonable endeavours to procure that the transfer provided for by this Agreement is a transfer of the Business as a going concern and neither a supply of goods nor a supply of services for the purposes of VAT.

- If, notwithstanding clauses 9 and 10, VAT is chargeable in connection with the transfer of the Assets under the Agreement, the Buyer shall pay the amount that VAT immediately on receipt of the relevant invoice, together with a copy of the confirmation from HM Revenue & Customs that VAT is payable.

Completion

- Completion shall take place immediately on exchange of this Agreement at the registered office of the parties or such other place as the parties may agree.

- As soon as is reasonably practicable after the Effective Time, the Seller shall place the Buyer in effective possession and control of the Business and shall deliver to the Buyer:

- physical possession of all Assets which are capable of transfer by delivery and which are in the Seller’s possession including all discs, materials, documents and source code in whatever medium that embody the Intellectual Property Rights and the IT system;

- assignments in respect of any of the Assets and Intellectual Property Rights not capable of passing by delivery; and

- such documents to complete the sale and purchase of the Assets and vest title to the Assets in the Buyer.

- Risk in the Assets shall pass to the Buyer upon the Effective Time.

- To the extent that any items listed at clause 11 do not pass by delivery to the Buyer, those items shall be held by the Seller on trust for the Buyer pending any necessary legal assignment.

Period after Completion

- The Seller shall and shall procure that any necessary party shall execute any necessary documents and do all such acts and things as may reasonably be required on or subsequent to the Effective Time by the Buyer for securing to or vesting in the Buyer the legal and beneficial ownership of the Assets.

- The Buyer will assume full responsibility for the Liabilities and the Creditors for the Effective Time.

License of Business Name

- The Seller hereby grants an irrevocable, worldwide, royalty free, transferable, exclusive licence to the Buyer to use the Business Name for any purpose that the Buyer sees fit.

Contracts

- The Seller shall, on and with effect from the Effective Time, assign to the Buyer all of the Contracts which are capable of assignment without the consent of the other parties.

- In the event that a Contract is not assignable, or cannot be assigned without liability or loss to the Seller, the Seller shall, at the option of the Buyer upon service of four (4) weeks notice:

- procure that the existing arrangements with the Seller be terminated and that the Seller be released from its obligations and that the Buyer be granted corresponding rights; and

- use all reasonable endeavours to procure that all relevant third parties waive the relevant provisions and otherwise deal with such Contracts as the Buyer may reasonably require.

Employees

- The parties agree that the sale pursuant to this Agreement will constitute a relevant transfer for the purposes of TUPE and, accordingly, that it will not terminate the contracts of employment of any of the Employees, which shall be transferred to the Buyer pursuant to TUPE with effect from the Effective Time.

- If any contract of employment of, or collective agreement relating to, any Employee is found or alleged not to have transferred to the Buyer at the Effective Time, the parties agree that they shall take all necessary steps to ensure that such contracts of employment or collective agreements shall have effect from the Effective Time as if originally made with the Buyer.

- The Buyer agrees that it shall be responsible for all costs, expenses, liabilities, claims, rights of action, compensation, awards, damages, fines, penalties, costs, expenses, interests arising from or in connection with the employment of the Employees, whether arising before or after the Effective Time.

Warranties

- The Seller warrants to the Buyer that each of the Warranties is true, accurate and not misleading at the date of this Agreement.

- Each of the Warranties is separate and, unless otherwise specifically provided, is not limited by reference to any other Warranty or any other provision in this Agreement.

Limitations on Claims

- The aggregate liability of the Seller for all claims shall not exceed .

- The Seller shall not be liable for a claim unless notice in writing of the claim, summarising the nature of the claim (in so far as it is known by the Buyer) and, as far as is reasonably practicable, the amount claimed has been given by the Buyer to the Seller:

- In the case of a claim made under the Warranties in Schedule 2, on or before the seventh anniversary of Completion; or

- in any other case, on or before the second anniversary of the Completion Date.

Data Protection

- The Buyer undertakes to comply with the Data Protection Laws in relation to its application to the Business and Assets after the Completion Date.

Further Assurance

- Each party (at its own cost) shall, and shall use its reasonable endeavours to procure, execute and perform all such further acts, deeds, documents and things as may be reasonably requested from time to time in order to implement all of the provisions of this Agreement.

Notices

- All notices or other communications under or in connection with this Agreement will be in writing and addressed to the other party.

- Notices will be sent:

- to the Seller at: , .

- to the Buyer at: , .

- Notices will be deemed received:

- by first-class post: 2 Business Days after posting;

- By airmail: 7 Business Days after posting;

- by hand: on delivery; and

- by facsimile: on receipt of a successful transmission report from the correct number.

- Either party may change the address or facsimile number to which such notices to it are to be delivered by giving not less than 5 Business Days’ notice to the other party.

Time of the Essence

- Each time, date or period referred to in this Agreement (including any time, date or period varied by the parties) is of the essence.

Expenses

- The parties agree to pay all of their own costs and expenses in connection with the negotiation, preparation and implementation of this Agreement (and any documents referred to in it).

Confidential Information

- Neither party shall, without the other party’s prior written consent (not to be unreasonably withheld), disclose:

- information pertaining to this Agreement, including, but not limited to the terms of the Agreement, the Purchase Price, the parties to this Agreement and the subject matter of this Agreement, as well as any written or oral information obtained about the respective parties that is not currently in the public domain;

- any business information or information relating to the customers, suppliers, methods, products, plans, finances, trade secrets or otherwise to the business or affairs or the other party; and

- any information developed by either party in performing its obligations under, or otherwise pursuant to this Agreement, subclauses a, b and c together being the Confidential Information.

- Neither party will use the other party’s Confidential Information except to the extent necessary or required to perform this Agreement.

- Disclosure of Confidential Information may be made to a party’s officers, employees and contractors, professional advisors, consultants and other agents if such disclosure is reasonably necessary, on the condition that the disclosing party is responsible for procuring that the relevant third party complies with its obligations under clause 17.

- Confidential Information does not include information which is:

- publicly available, other than as a result of this Agreement;

- lawfully available to a party from a third party who was not subject to any confidentiality restrictions prior to the disclosure of such Confidential Information; or

- required to be disclosed by law, regulation or by order or ruling of a court or administrative body.

- Each party agrees to indemnify the other against any and all harm suffered for any breach of confidentiality.

- On termination of this Agreement, all Confidential Information relating to or supplied by a party which is or should be in the other party’s possession will be returned to the other party or (at the first party’s option) destroyed and certified as destroyed.

- The confidentiality restrictions in this Agreement will continue to apply for a period of five years from the termination of this Agreement.

General

- No amendment or variation of this Agreement shall be effective unless agreed in writing and signed by or on behalf of the parties, or by their authorised representatives.

- Each provision of this Agreement is severable. If any provision of this Agreement (wholly or partly) is or becomes illegal, invalid or unenforceable, that shall not affect the legality, validity or enforceability of any other provision of this Agreement. Where any provision of this Agreement is found to be unenforceable, the Buyer and the Seller shall will make reasonable efforts to replace such a provision with a valid and enforceable substitute provision, the effect of which, is as close as possible to the intended effect of the original invalid or unenforceable provision.

- No failure or delay by a party to exercise any right or remedy provided under this agreement or by law shall constitute a waiver of that or any other right or remedy, nor shall it prevent or restrict the further exercise of that or any other right or remedy. No single or partial exercise of such right or remedy shall prevent or restrict the further exercise of that or any other right or remedy. A waiver of any right or remedy under this Agreement or by law is only effective if it is in writing.

- This agreement may be executed in any number of counterparts, each of which when executed and delivered (receipt by email shall constitute delivery) shall constitute a duplicate original, but all counterparts together constitute the one agreement.

- This Agreement shall be binding on, and ensure for the benefit of, each party and their respective successors and assigns.

- Neither party shall without the prior written consent of the other party (such consent not to be unreasonably withheld) assign this Agreement either in whole or in part.

- This Agreement and the documents referred to in it constitute the entire agreement and understanding between the parties and supersede all previous agreement between the parties in relation to such matters.

- This Agreement shall be governed by and construed in all respects in accordance with the laws of England and Wales. Each of the parties irrevocably submits to the exclusive jurisdiction of the English and Welsh courts.

The parties have signed the Agreement on the date(s) below:

| _________________________________ | _________________________________ |

| _________________________________ | _________________________________ |

SCHEDULE 1 - ASSETS AND VALUES

The Assets included in the sale pursuant to this agreement and their respective values are as follows:

SCHEDULE 2 - WARRANTIES

Information Supplied

- All information contained in this Agreement, all matters contained in the Disclosure Letter and all other information relating to the Business given by or on behalf of the Seller to the Buyer, its advisers or agents are true, accurate and complete and are not misleading.

- There is no information that has not been Disclosed, which, if Disclosed, might reasonably affect the willingness of the Buyer to buy the Business (comprising the Assets) on the terms of this Agreement.

The Seller

- The Seller has all necessary power and authority, and has taken all necessary corporate action, to enable it to enter into and perform this Agreement and all agreements and documents entered into, pursuant to the terms of this Agreement.

- The Assets are sold by the Seller to the Buyer with such title as is available to the Seller.

Ownership of the Assets

- No option, right to acquire, mortgage, charge, pledge, lien (other than a lien arising by operation of law in the ordinary course of trading) or other form of security or encumbrance or equity on, over or affecting the Assets is outstanding and, apart from those set out in this agreement, there is no agreement or commitment to give or create any of them, and no claim has been made by any person to be entitled to any of them.

Records

- All records:

- have been fully, properly and accurately prepared and have at all material times, been fully, properly and accurately maintained and are properly written up to date;

- are in the possession of the Seller;

- constitute an accurate record of all matters that ought to appear in them; and

- do not contain any material accuracies or discrepancies.

Accounts

- The Accounts have been properly prepared in accordance with generally accepted accounting principles applied in the United Kingdom and in accordance with applicable laws and regulation in the United Kingdom.

- The Accounts have been audited by an auditor or firm of accountants qualified to act as auditors in the United Kingdom.

- The Accounts give a true and fair view of the state of affairs of the Business as at the Accounts Date and of the profit or loss of the Business for the financial year ended on that date.

- Since the Accounts Date, the Business has been carried on in the ordinary and normal course so as to maintain it as a going concern.

- Since the Accounts Date, there has been no material reduction in the value of the Fixed Assets specified in the Accounts, to the extent still owned by the Seller.

Title to the Assets

- The Assets comprise all assets now used in the Business and that are necessary for the continuation of the Business as now carried on.

- The Seller has good title to each Asset and each Asset is legally and beneficially owned by the Seller.

- There are no encumbrances over any of the Assets, and the Seller has not agreed to create any encumbrances over the Assets or any part of them.

The Contracts

- The Contracts are the only contracts entered into, or which will have been entered into before the Effective Time or by or on behalf of the Seller in connection with the Business which at the Effective Time, will remain to be performed in whole or in part.

- The Contracts are valid and binding and no act or omission has occurred which would constitute a breach of any Contract.

Condition of the Assets

- Where relevant, the Fixed Assets and Movable Assets:

- are in good repair, condition and working order and will continue to be capable of doing the work for which they were designed;

- have been regularly and properly maintained; and

- are used exclusively in connection with the Business.

Employees and Agents

- No person is employed or engaged in the Business (whether temporary or permanent and whether under a contract of service or contract for services) other than the Employees.

- The Employees are all employed by the Seller and work wholly or mainly in the Business.

- The Seller has disclosed:

- copies of all service contracts, policies, notices of termination and other documents (whether binding or not) which apply to the Employees, identifying which applies to which employee;

- full particulars of the current terms of employment or engagement and benefits of all Employees, whether or not recorded in writing, or implied by custom or practice or otherwise;

- copies of all agreements or arrangements with any trade union, employee representative or body of employees or their representatives (whether binding or not) and details of any such unwritten agreements or arrangements which made affect Employees;

- details of any Employee who has given or received notice to terminate their employment or who intends or is likely to terminate their employment as a result of this Agreement; and

- all such particulars are accurate and complete in all respects.

- The Seller has provided the Buyer with the information required under regulation 11 of TUPE in relation to each of the Employees.

- The Seller has not offered, promised or agreed to any future variation in any contract of employment of any one of the Employees or any other person employed by the Seller in respect of whom liability is deemed by TUPE to pass to the Buyer.

- The Seller is not engaged or involved in any dispute, claim or legal proceedings with any of the Employees or any other person currently or previously employed by or engaged in the Business, and so far as the Seller is aware, there is no event which could give rise to such dispute, claim or proceedings.

- There are no agents or distributors of the Seller engaged in any work related to the Business.

- The Seller has not (nor has any predecessor or owner of any part of the Business) been a party to any relevant transfer for the purposes of TUPE affecting any of the Employees or any other persons engaged in the Business and no event has occurred which may involve such persons in the future being a party to such a transfer. No such persons have had their terms of employment varied for any reason as a result of or connected with such a transfer.

Litigation

- The Seller is not engaged in, subject to, or threatened by any:

- litigation, administrative, mediation or arbitration process in relation to the Business or the Assets or any of them; or

- is the subject of any investigation, inquiry or enforcement proceeds by any governmental, administrative or regulatory body.

Solvency of the Seller

- The Seller is solvent and able to pay its debts as they fall due.

- No order has been made, petition presented or resolution passed for the winding-up of the Seller, nor has any receiver been appointed in respect of the Business or the Assets.

Compliance

- All applicable laws and regulations, orders, provisions, directions and conditions relating to the Assets or the conduct of the Business (including VAT) have been duly complied with in all respects.

- All necessary licences, consents, permits, agreements, arrangements and authorities have been obtained to enable the Seller to carry on the Business.

Intellectual Property

- All Intellectual Property is either:

- in the sole legal and beneficial ownership or the Seller, free from all licences, charges or other encumbrances; or

- the subject of binding and enforceable licences from third parties in favour of the Seller:

- of which no notice to terminate has been received;

- all parties to which have fully complied with all obligations in those licences; and

- in relation to which no disputes have arisen or are foreseeable.

- In either case, nothing has been done, or omitted to be done which would jeopardise the validity, enforceability or subsistence of any Intellectual Property or any such licences.

Property

- The information set out in Schedule 1 of this Agreement and any particulars of the Properties are true, complete and accurate.

IT

- The Seller is the owner of the IT System, free from encumbrances and all other rights exercisable by third parties.

- The Seller has obtained all necessary rights from third parties to enable it to make exclusive and unrestricted use of the IT System. Such rights are freely transferable to the Buyer.

- The IT system is functioning properly and is not defective in any respect.

Tax

- All documents to which the Seller is a party and which relate to the Business, in the enforcement of which the Buyer may be interested, have been duly stamped.

- The Seller has not opted to tax (or elected to waive exemption), or will before Completion, opt to tax any of the Properties.

- The Seller is a registered and taxable person for the purposes of the VATA 1994.

About Asset Purchase Agreements

Learn more about making your Asset Purchase Agreement

-

How to make an Asset Purchase Agreement

Making your Asset Purchase Agreement online is simple. Just answer a few questions and Rocket Lawyer will build your document for you. When you have all the information about the sale prepared in advance, creating your document is a quick and easy process.

You’ll need the following information:

The seller and the buyer

-

What are the seller’s name, address, website address, and company number?

-

Who is the seller’s signatory? This is the person who will sign the Agreement on the company’s behalf.

-

At which address will the seller receive any notices or other communications regarding the Agreement?

-

What are the buyer’s name, address, website address, and company number?

-

Who is the buyer’s signatory?

-

At which address will the buyer receive any notices or other communications regarding the Agreement?

The target business

-

What is the name of the company whose assets are being purchased?

-

What is the target company’s accounts date (ie its year-end date)?

-

What kind of business is the target engaged in?

The assets

-

Which types of assets are being sold? For example, freehold or leasehold properties? Stock? Contracts? Goodwill? Intellectual property rights?

-

If goodwill is being sold, what is the monetary value placed on the business’s goodwill?

-

What is the value of each category of assets involved in the transaction?

-

Are employees being transferred as part of the asset sale?

-

Is the seller selling the assets with full or limited title guarantee (ie do they own the assets outright and have full knowledge of the ownership of the assets, or not)?

Restrictions

-

Will the seller be restricted from setting up a business that competes with the target? If so:

-

For how many years?

-

Within which areas (eg countries, markets, or postcodes) does the restriction apply?

-

Will the seller be restricted from soliciting the buyer’s employees and workers? If so, for how many years?

-

Will the seller be restricted from dealing with the buyer’s customers? If so, for how many years?

-

Will the seller be restricted from soliciting the buyer’s suppliers? If so, for how many years?

-

Will the seller be restricted from using the target’s intellectual property rights?

Limitations of liability

-

What limit is being set on the seller’s liability in respect of warranty claims?

The Asset Purchase Agreement

-

What is the purchase price being paid for the target’s assets?

-

What date will the Agreement start? Immediately after it’s signed or after completion?

-

If the buyer and/or the seller are based in Scotland, will the Agreement be governed by the laws of England and Wales or the laws of Scotland?

-

-

Common terms in an Asset Purchase Agreement

Asset Purchase Agreements set out the terms of the sale of a business’s assets from one company to another. To do this, this Asset Purchase Agreement template includes the following terms and sections:

This Asset Purchase Agreement is made on the last day of signature…

The Agreement starts by clearly identifying the buyer and the seller and by highlighting the date of the Agreement.

Introduction

This term explicitly states the purpose of the contract: agreeing to an asset sale and its terms.

Definitions and interpretation

This definition table assigns specific meanings to key terms used throughout the Agreement. When these terms (eg ‘Assets’, ‘Effective Time’, or ‘Stock’) are used capitalised throughout the Agreement, they carry the meaning they’re given in this table.

The table also contains some key details of the purchase, for example, the target business’s name and the date that the Agreement is to be effective (ie either after the Agreement is signed or after completion).

Agreement to sell and purchase

This section sets out how certain categories of assets will be transferred under the Agreement. These are essentially those assets that are required to sell the business as a going concern (eg still operating). They include the right to use the business’s name and ownership of stock. Assets transferred under this section are transferred with either full or limited title guarantee and generally without other formalities needing to be met.

Consideration

The total purchase price that the buyer is paying for the assets is set out here.

VAT

This section explains how VAT relevant to the sale is to be dealt with. For example, the purchase price does not include VAT and any VAT that is payable should be paid by the buyer.

Completion

This section starts by stating that completion (eg when the transfer of assets is made by the execution of necessary documents) of the sale will take place immediately on exchange of the Agreement (ie when it is signed). This means that completion will occur at the same time that signing is completed.

The section then explains what should happen after the Agreement starts. For example, the seller should put the buyer in control of and deliver to them various assets, where necessary by completing relevant documentation. It provides that any assets not passed to the buyer by delivery will be held on trust by the seller for (ie for the benefit of) the buyer until these assets can be legally transferred using formal procedures.

Period after completion

This section sets out a requirement for the seller to, after completion, do anything reasonably necessary to transfer the assets to the seller (eg by executing certain documents). The section also explains that the buyer takes responsibility for certain liabilities and debts that the business holds (eg liabilities arising in the ordinary course of business) after completion.

Licence of business name

In this section, the seller grants the buyer exclusive permission (ie an exclusive licence) to use the business’s name.

Contracts

This section deals with which of the business’s contracts will be transferred (eg assigned) from the seller to the buyer. Those capable of being assigned without another (ie third) party’s permission are to be assigned after the Agreement’s start date. Those not capable of being assigned must be dealt with in a certain way, for example, the seller may with the buyer’s agreement attempt to have contracts ended.

Employees

This section explains how the buyer will take over the seller’s employment relationships. For example, employees of the business will have their Employment contracts transferred from the seller to the buyer as a transfer under The Transfer of Undertakings (Protection of Employment) Regulations 2006 (TUPE). For more information, read Transfer of undertakings.

Warranties

Rules on how the Agreement’s warranties (set out in ‘Schedule 2 - Warranties’) operate are set out here. For example, that the warranties are separate from each other and should not limit each other.

Limitations on claims

This section contains a limitation of liability, in which the seller’s liability for (ie obligation to cover) the costs of legal claims relevant to the Agreement is capped at a specified amount and by other procedural requirements.

Data protection

The buyer promises in this section to abide by data protection laws when it takes over the business and assets.Restrictive covenants

This section contains any restrictions imposed on the seller in relation to what they may do after the sale. For example, non-compete or non-solicitation covenants.

Further assurance

This section contains a commitment by both parties to do any other necessary acts (eg executing documents) required to implement this Agreement.

Notices

This section explains how and to which addresses any notices or other communications relative to this Agreement should be sent.Time of the essence

The presence of this clause, stating that times and dates contained in this Agreement are ‘of the essence’, essentially means that these times are to be considered serious and binding obligations under this contract. Breaching them (eg by being late to abide by an obligation) may lead to serious consequences, for example, the other party being entitled to end the Agreement.

Expenses

The parties commit here to paying their own expenses in relation to negotiations and similar related to the Agreement.

Confidential information

This section sets out how the parties should deal with each other’s confidential information when they handle it as a part of the transaction. For example, it must not be disclosed except in certain circumstances. The parties provide each other with an indemnity against losses suffered due to any breaches of that party’s confidentiality. The confidentiality terms are intended to apply for 5 years after the Agreement is ended, if it is ended.

General

This section deals with various other points of law that govern how this Agreement operates. For example:

-

requiring that any variations to the Agreement are in writing and signed

-

explaining that this Agreement may be executed and delivered across various events

-

restricting how the parties can deal with the Agreement (eg preventing them from assigning their rights or obligations under the Agreement to others without the other party’s permission)

-

stating that this Agreement is the entire agreement, ie the Agreement contains all of the agreement between the buyer and the seller (ie there are no additional terms). This helps avoid confusion if, for instance, other terms were in contemplation during negotiations

-

specifying which country’s legal system must be used to resolve any disputes. This is the Agreement’s jurisdiction. This is necessary as the legal systems of England and Wales and of Scotland are different

Signatures

The body of the Agreement is followed by spaces for the parties to sign and date the Agreement to make it legally binding.

Schedule 1 - Assets and values

This schedule sets out exactly which assets are being transferred under this Agreement and their value.

Schedule 2 - Warranties

This schedule contains the various warranties (ie promises) that the parties are making to each other under and in relation to the Agreement. These include warranties on:

-

information supplied - for example, that all relevant information has been disclosed and that information that has been given is true

-

the seller - for example, that they own the relevant assets and have the authority to perform their obligations under the Agreement

-

ownership of the assets - for example, if the assets are being sold with full title guarantee, the seller promises here that they are free from any third party rights (eg beneficial interests under a trust)

-

records - for example, that records provided are accurate and up to date

-

accounts - for example, that since the end of the business’s last accounting year, it has been carrying on business as usual

-

title to the assets - for example, that the assets to be transferred under the Agreement comprise all of those necessary for the buyer to continue the business

-

the contracts - for example, that there are no relevant contracts not included in those being transferred under the Agreement

-

condition of the assets - for example, that fixed and moveable assets are in good repair and properly maintained

-

employees and agents - for example, that the seller has disclosed specified relevant information about the business’s employees

-

litigation - for example, that the seller is not currently engaged in any legal disputes relevant to the business being sold

-

solvency of the seller - for example, that the seller is solvent and has not passed a winding up resolution

-

compliance - for example, that the seller holds all licences and similar required for the business’s operation

-

intellectual property - for example, that the seller owns or holds enforceable licences to use all relevant intellectual property rights

-

property - for example, that details provided about properties transferred under the Agreement are accurate

-

IT - for example, that the seller has the rights to use any transferred IT system

-

tax - for example, that any relevant documents that the seller is party to have been stamped (eg have received acknowledgement that stamp duty has been paid)

-

stock - for example, that the stock being transferred under the Agreement is adequate for the business’s purposes

Schedule 3 - Stock valuation

This schedule sets out the procedures that should be followed when establishing the value of any stock transferred under the Agreement. For instance, after the Agreement is executed, the buyer should follow a set procedure to create a valuation of the stock at this time, which the seller may accept or dispute.

Schedule 3 or 4 - Employees

If any employees are being transferred as a part of the sale, their details must be included in this schedule.

If you want your Asset Purchase Agreement to include further or more detailed provisions, you can edit your document. However, if you do this, you may want a lawyer to review the document for you (or to make the changes for you) to make sure that your modified Asset Purchase Agreement complies with all relevant laws and meets your specific needs. Use Rocket Lawyer’s Ask a lawyer service for assistance.

-

-

Legal tips for buyers and sellers

Make sure you understand your commitments under this Agreement

Asset Purchase Agreements are complex and powerful legal documents. You are making multiple serious and often long-lasting legal commitments when you enter into one. It’s particularly important, therefore, that everyone involved understands all terms of an Asset Purchase Agreement. To achieve this, read your Agreement carefully alongside the information provided on this page, and Ask a lawyer if you have any questions.

Be transparent during the sale process

Honesty is extremely important in commercial transactions. Multiple terms of this Agreement contain promises by the parties related to the truthfulness and completeness of various pieces of information exchanged as part of the sale process (eg accounts or information about employees). The consequences of breaching these promises can be severe. It’s important to provide all necessary information in an accurate, complete, and not misleading manner. For example, make sure an appropriate disclosure letter is used.

Understand when to seek advice from a lawyer

In some circumstances, it’s good practice to Ask a lawyer for advice to ensure that you’re complying with the law and that you are well protected from risks. You should consider asking for advice if:

-

you're unsure about the warranties being made

-

you're unsure of the restrictions being imposed on the seller

-

you need help with due diligence

-

you need help making a disclosure (eg help writing a disclosure letter)

-

you will have affected transferring under the asset sale

-

you want to include bespoke terms in an Asset Purchase Agreement (eg extra or amended warranties)

-

you need help with tax considerations

-

Asset Purchase Agreement FAQs

-

What is included in an Asset Purchase Agreement?

This Asset Purchase Agreement template covers:

-

which assets are being sold

-

categories of assets including goodwill, freehold and leasehold properties, fixed assets, stock, intellectual property, and IT systems

-

the purchase price for the assets

-

warranties

-

restrictions on the seller post-completion

-

notices

-

employees being transferred

-

stock valuation

-

how the transaction is to be completed

-

-

Do I need an Asset Purchase Agreement?

An Asset Purchase Agreement helps to set out and finalise all of the agreed terms and conditions of the sale of a business’s assets. Setting out the terms of a sale in a formal, written document helps the parties avoid disputes down the line. It also ensures that both parties know how to proceed during the sale and beyond (eg by setting out warranties, limitations of liability, and restrictive covenants).

An Asset Purchase Agreement is the appropriate document to use if you only want to buy specific assets of a business instead of the entire company that runs it. You can usually use these assets to carry on some of the business’s activities without taking on all of the seller company’s liabilities.

For more information, read Asset purchase agreements.

-

What assets can be bought and sold with this Asset Purchase Agreement?

This Asset Purchase Agreement can be used to cover sales of a business’:

-

goodwill

-

fixed assets (eg equipment)

-

moveable assets (eg vehicles)

-

contracts

-

stock

-

business information

-

records

-

third-party rights

-

intellectual property rights (eg trade marks used for branding)

-

IT systems

-

-

What are warranties in an Asset Purchase Agreement?

Warranties are statements of fact or promises that a party gives to another party to assure them that certain conditions are true. For example, promises that information and records are accurate or that a party has the necessary rights to enable it to perform its obligations under a contract.

Warranties are important in Asset Purchase Agreements as they reduce the risks that a buyer is exposed to as a result of the transaction. If a warranty turns out to be untrue and this causes the buyer to sustain losses (eg the reduction in an asset’s value), the buyer may make a legal claim against the seller for damages (ie compensation).

It is up to the buyer to ensure that they fully understand the consequences of completing an asset purchase. Warranties help buyers to achieve this by acting as an information-gathering mechanism and assisting in any due diligence carried out prior to completing the asset sale.

-

What is consideration?

Consideration is something of value that’s exchanged for something else under a contract. In this Asset Purchase Agreement, the consideration provided by the buyer is the purchase price payable in exchange for the assets they’re purchasing. It's important that the true value of assets is reflected in the Agreement when completing an asset sale. It's usual for the parties to obtain a valuation of the business’s assets through completion accounts. This is a process that allows the purchase price to be adjusted later on during the sale (eg post-completion) in the event that the value of the assets changes.

-

What are restrictive covenants?

The buyer involved in an asset sale may want to impose restrictions on the seller after the sale is completed. Common restrictions include the seller agreeing not to be involved in any competing business and not to solicit (eg hire or sell to) the seller’s customers, suppliers or employees for a specified period of time.

It is important to ensure that any restrictions imposed are reasonable and not unjustifiable restraints of trade. Otherwise, restrictions risk being unenforceable. To ensure terms are reasonable, it is helpful to limit restrictions in terms of scope (geographically and functionally) and time. The usual duration of restrictions is 1 to 5 years.

For more information, read Non-solicitation and restrictive covenants.

-

What is limitation of liability?

Limitation of liability clauses limit the amount one party has to pay another party if that party suffers loss because of a breach of contract by the first party. It is usual for a seller to limit its liability under an Asset Purchase Agreement, especially in relation to the warranties. The buyer usually accepts this limitation as a term of the Agreement.

For more information, read Limitation of liability clauses.

-

What is the difference between a share sale and an asset sale?

If a buyer buys a company (ie the target company) by means of a share sale and purchase (eg using a Share purchase agreement), the buyer takes ownership of shares in the target company. The buyer will acquire the target company with all of its assets and liabilities.

By contrast, if a buyer buys a business as a going concern (ie while it‘s operating and making a profit) by means of an asset sale and purchase, the individual assets of the business concerned will be transferred to the buyer along with the goodwill of the business. This means that the buyer can decide which assets in the target company it will purchase and can leave behind any liabilities, for example, debts and pending litigation.

-

Do I need a disclosure letter?

If a seller is making warranties that they know to be untrue or conditional (eg possibly untrue), they will need to disclose this to the buyer in a disclosure letter. This helps prevent any claims for breach of warranty, as in delivering the disclosure letter the seller discloses against the warranty and makes the buyer aware of the facts before the Agreement that contains the warranty is executed.

From the buyer's perspective, disclosure letters help them to collect information from the seller relating to the warranties. This information may not have been provided during due diligence. It's important for the buyer to obtain effective disclosure, as this will allow them to negotiate and adjust the purchase price of the assets before completion, or even restructure the sale as a share sale, if appropriate (eg if a disclosure letter informs them about a significant upcoming legal claim).

Ask a lawyer if you need help creating a disclosure letter.

-

What do I need to do after I sign the Agreement?

After completion, there are a few additional steps that the buyer must take to ensure they are compliant with the law and that their purchase is properly executed. These include:

-

paying stamp duty and Stamp Duty Land Tax (SDLT), if applicable

-

paying VAT, if applicable. VAT is chargeable on the transfer of most assets used in a business, assuming that the seller is a taxable person

-

assigning or novating the benefits and/or burdens of contracts with the business’s customers and suppliers

-

carrying out administrative matters, for example, handling insurance, payroll, VAT, and pensions matters

-

Our quality guarantee

We guarantee our service is safe and secure, and that properly signed Rocket Lawyer documents are legally enforceable under UK laws.

Need help? No problem!

Ask a question for free or get affordable legal advice from our lawyer.