What is VAT?

Value added tax (VAT), introduced under the Value Added Tax Act 1994, is a tax added to most goods and services sold by VAT-registered businesses. It is technically a tax on consumers rather than businesses and is therefore known as an indirect tax. A business must charge VAT on all taxable supplies it sells if it is VAT-registered.

VAT added to your sales is known as output VAT, while VAT you pay on business purchases is referred to as input VAT. You pay the difference between the two to HMRC.

Note that when a business purchases goods or services from other businesses, VAT can be claimed back from the total purchase amount.

What are the different VAT rates?

HMRC sets different rates depending on what you sell. As a business owner, you must apply the correct rate:

-

the standard rate (20%) applies to most goods and services

-

the reduced rate (5%) applies to items like home energy and children’s car seats

-

the zero rate (0%) applies to most food and children’s clothing. You don't charge VAT, but must still record these sales in your VAT accounts

-

exempt items like insurance or health services do not count towards your VAT turnover

Note that different rules apply to digital products like apps or e-books. For more information on how to handle these, read VAT on digital services.

Do I need to register for VAT?

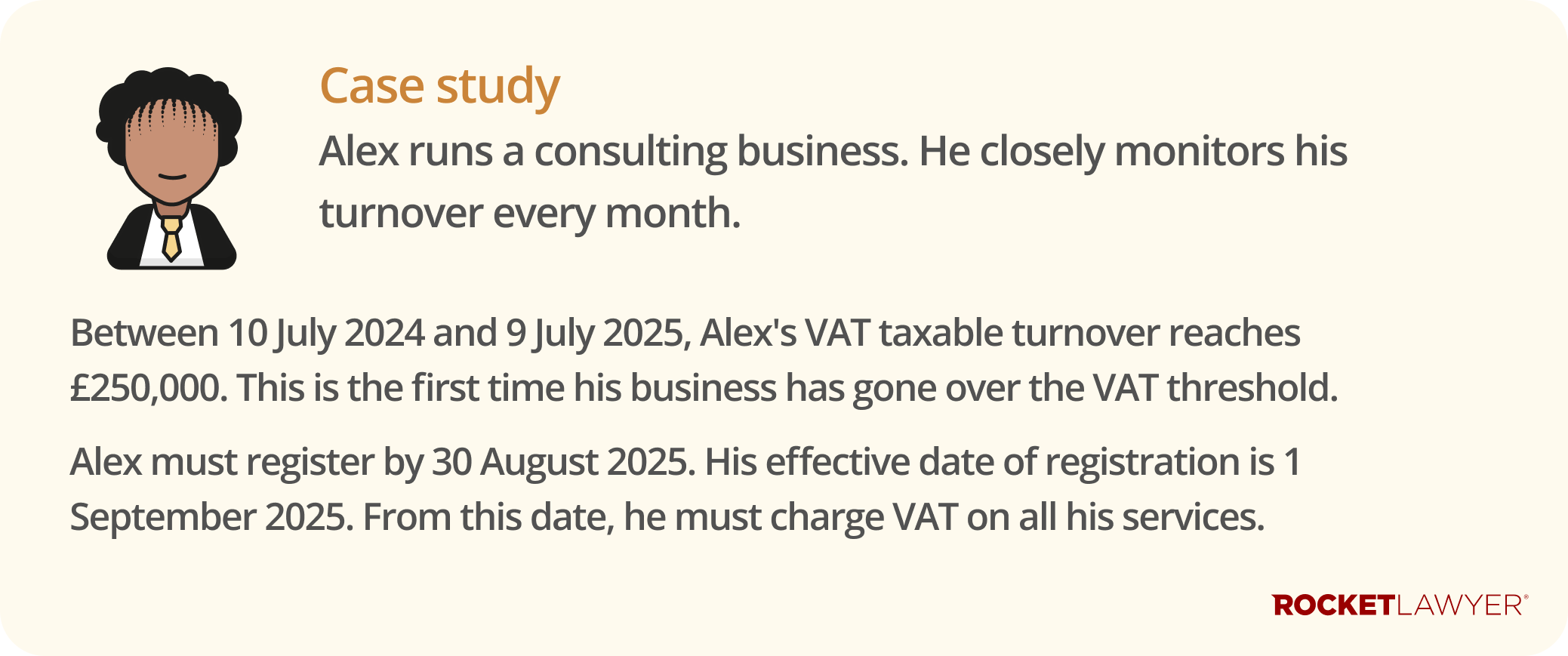

You must register for VAT with HMRC if your business’s total taxable turnover is more than £90,000 over any rolling 12-month period.

You also need to register if you expect your turnover to go over this £90,000 threshold in the next 30 days alone.

If your turnover is less than £90,000, you can choose to register for VAT. This is known as a voluntary registration and allows you to reclaim VAT on business purchases, which is particularly useful if you deal mostly with other VAT-registered businesses. For more information on why you might do this, read Reclaiming VAT.

How do I register for VAT?

You can register for VAT online on the government website. Under certain circumstances, you may register by post using form VAT1. These circumstances include where:

-

a local authority, parish, or district council is registering for VAT

-

you’re registering divisions or business units of a body corporate under separate VAT numbers

-

you cannot apply online (eg due to a disability)

Once the application is submitted, it usually takes around 30 working days to receive your certificate.

What happens after I register for VAT?

Once your registration is successful, HMRC will issue you a 9-digit VAT registration number and a VAT certificate. As a VAT-registered business, you must follow specific rules to stay compliant with HMRC, including:

-

applying the correct VAT rate to every product or service you sell

-

displaying your unique VAT registration number clearly on every Invoice

-

logging the VAT you pay on business-related expenses so you can offset these costs

-

accounting for any VAT due on goods you bring into the UK from abroad

-

filing a VAT return with HMRC (usually every three months) to report your total sales and purchases

-

settling any outstanding tax balance with HMRC by the required deadline

How do I add VAT?

When a business is VAT registered, it is typically required to add VAT when invoicing a client for services and maintain a record of the VAT charge to be included in VAT returns. This process ensures that your output VAT (the tax you collect on behalf of the government) is recorded correctly. You should use professional software or a template to ensure all mandatory information is included on your VAT invoices.

Pricing and calculations

Prices can be inclusive or exclusive of VAT. When charging VAT on goods or services, you need to make a calculation. This also applies when you’re working out the amount of VAT you can reclaim on items you sold inclusive of VAT. It is essential to clearly communicate to your customers whether the price you quote is the final amount or if tax will be added on top.

To work out a VAT-inclusive price at the standard rate (20%), multiply the price exclusive of VAT by 1.2. For example, if your net service price is £100, multiplying it by 1.2 gives you a total price of £120. This calculation ensures the correct 20% tax is added to the customer's bill.

To work out a VAT-exclusive price at the standard rate (20%), divide the price including VAT by 1.2. This is often necessary when you receive a receipt that shows only the total amount paid, and you need to log the original price for your records. For example, if a total bill is £120, dividing it by 1.2 reveals the net price to be £100.

What is Making Tax Digital for VAT?

All VAT-registered businesses must follow the Making Tax Digital (MTD) rules. This means you must keep specific digital records and use compatible software to submit your VAT returns to HMRC. You cannot use HMRC’s old online portal for these submissions unless you have an official exemption. Businesses below the VAT threshold can still choose to join the MTD service voluntarily.

Keeping digital records

Under MTD, you must digitally store your business name, address, VAT registration number, and details of the VAT scheme you use. For every transaction, you must record the 'tax point', the value excluding VAT, and the amount of VAT charged. You must ensure that all VAT records, including receipts and invoices for the year, are digitised and backed up securely. Generally, you must keep these records for at least six years.

Exemptions from MTD

The Making Tax Digital rules don’t apply to every organisation. For example, if a business uses the VAT GIANT service (such as government departments or NHS Trusts), they follow different procedures. You may also be exempt if your business is subject to an insolvency procedure or if you have an exemption (eg if you cannot use digital tools due to age or disability). For more information, see the government’s guidance on applying for an exemption from MTD for VAT.

What are the different VAT schemes?

HMRC offers several alternative accounting schemes designed to simplify the administrative burden for small businesses. Each scheme has specific eligibility criteria and potential benefits for your cash flow.

Depending on your industry and how you manage your finances, you may find one of the following options more beneficial than the standard method:

-

the flat rate scheme - you pay a fixed VAT percentage to HMRC. You cannot reclaim VAT on most purchases; however, bookkeeping is simplified. This scheme is only available if your turnover is £150,000 or less

-

cash accounting scheme - you account for VAT when money actually changes hands, aiding cash flow if customers pay late. This scheme is only available if your turnover is £1.35 million or less

-

annual accounting scheme - you submit one return per year instead of four and make advance payments. This scheme is only available if your turnover is £1.35 million or less

-

margin and retail schemes - margin schemes allow you to pay VAT only on your profit (common for second-hand goods), while retail schemes calculate VAT based on daily takings rather than individual sales

For more information, see the government’s guidance on VAT schemes.

If you’ve reached the threshold and need to issue professional documents, you can make an Invoice to ensure you're charging VAT correctly. If you're unsure how these rules apply to your specific trade, do not hesitate to Ask a lawyer if you have any questions.