What is VAT?

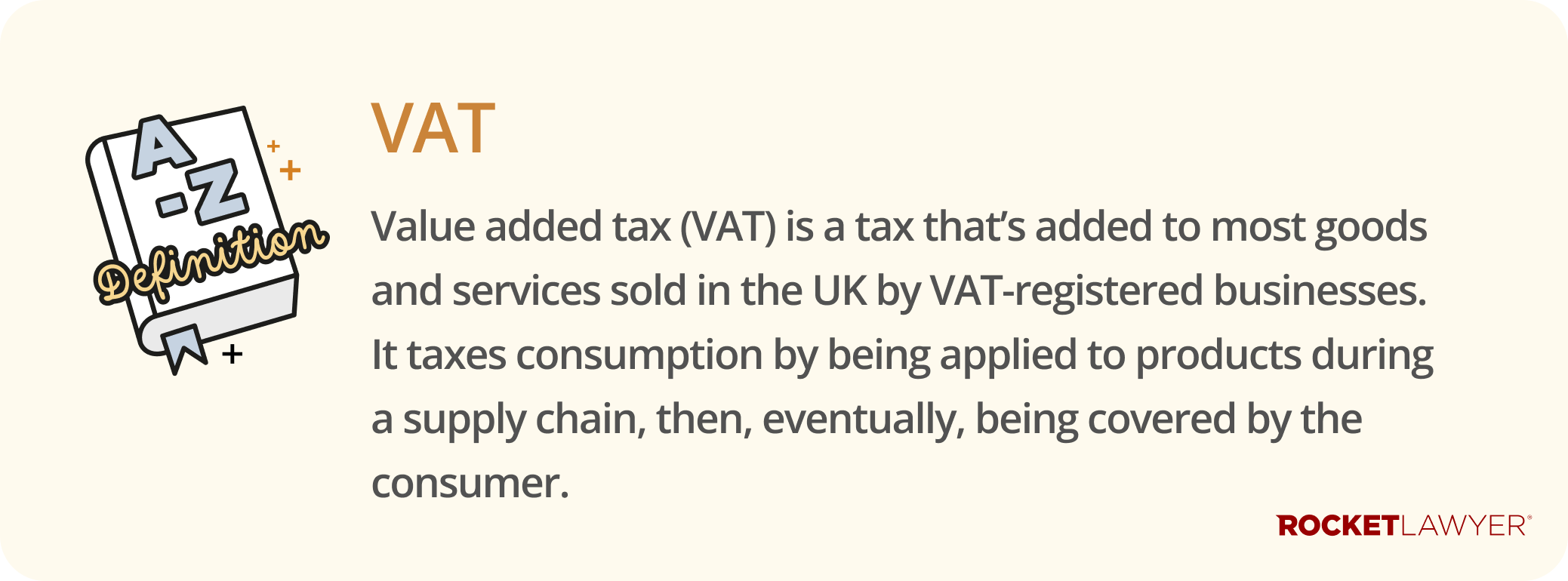

VAT is a consumption tax levied on most goods and services provided by registered businesses in the UK. VAT is considered an indirect tax because the tax is paid to the government by the seller (the business) rather than the person who ultimately bears the economic burden of the tax (the consumer). For further information, read VAT.

What is considered digital services?

A digital e-commerce business model supplies digital products wholly online without needing a direct physical presence in the markets in which the business operates. The following are examples of digital e-commerce services:

-

provision of digitised products including ebooks, software, software upgrades and digital applications (ie apps)

-

services provided on an electronic website or a webpage

-

provision of databases (such as search engines, text, information and automated distance learning services)

-

services automatically generated and supplied by a computer via the internet or an electronic network

-

downloads of music, films, games and gambling games via the internet

Therefore businesses who sell apps such as smartphone games, ebooks, online gaming businesses, streaming services and digital access to products that are subscribed to, are considered digital services for VAT purposes.

How does VAT apply to digital services?

As a consumption/sales tax, VAT can apply to all forms of transactions in digital e-commerce. The main focus points are:

-

considering whether the services are provided to a business (B2B) or a final consumer (B2C) as this will determine who is responsible for accounting for VAT on the services

-

where the services were supplied

-

where they were 'effectively enjoyed'

B2B digital e-commerce between EU businesses

If the customer is a business and is located in the EU, it is the customer who has the liability to account for VAT. To determine the location of the business, it's usually where the business is registered and has its head office or the country where it has fixed premises and staff receiving the services.

If the customer provides their VAT number, they are treated as a business customer. If the customer does not provide a VAT number, the supplier must receive alternative evidence to prove that they are a registered business in order to be treated as a business customer.

B2C digital e-commerce within the EU

VAT is due in the consumer's location (where they have a permanent address of usual residence). So VAT applies to where the customer uses or consumes the digital services.

The rate of taxation depends on the location of the consumer, not the location of the supplier. On a B2C basis, the supplier is responsible for accounting for VAT on the supply to the tax authority and at the rate applicable in the consumer's EU member state.

For example, if your customer resides:

-

in the UK, then UK VAT is due

-

in an EU member state, then VAT will be due in that country according to its rate and rules and you'll be required to either register in that member state or register for the MOSS (special accounting schemes for business services)

B2B/B2C digital e-commerce outside of the EU

If an EU business is supplying digital services to a business or consumer outside of the EU then no EU VAT is charged. However, if the service is effectively used and enjoyed in an EU country, that country can decide to levy VAT.

Electronically supplied publications

Special VAT rules apply to electronically supplied publications, with certain electronically supplied publications being eligible for a zero rate of VAT.

The following products (provided they are supplied electronically) are entitled to this zero rate of VAT:

-

books

-

booklets

-

brochures

-

pamphlets

-

leaflets

-

newspapers

-

journals and periodicals (including magazines)

-

children’s picture and painting books

There are certain products that are not included in the publications eligible for the zero rate of VAT, which include:

-

e-publications where more than half of the publication is devoted to advertising, audio or video content

-

audiobooks (this zero rate of VAT only applies to electronic versions of books that can be read or looked at)

-

supplies of intellectual property (even if supplied electronically) are not considered e-publications

-

plans or drawings for industrial, architectural, engineering, commercial or similar purposes (even if supplied electronically)

What if a zero-rated e-publication is supplied alongside a non-zero rated product?

Where a zero-rated e-publication (eg an e-book) is supplied together with a non-zero product (eg a printed book), it will need to be determined if the supplier is supplying the products in one, single supply or in multiple supplies.

Generally, a single supply will be made where one element of the supply is the principal element to which all other elements are ancillary. Multiple supplies are made where the various elements of the supply are distinct and independent.

A single supply may be indicated by:

-

a single price

-

the supply of the products being advertised as a package

-

the different components not being available separately

-

the different components being delivered at the same time

-

the customers believing that what they are getting is a single supply

Multiple supplied may be indicated by:

-

separate pricing or invoicing

-

the items being available separately

-

there being a time differential between parts of the supply (eg the products being delivered at different times)

-

the elements of the supply not being dependent on one another or connected

For more information, read the government's guidance.