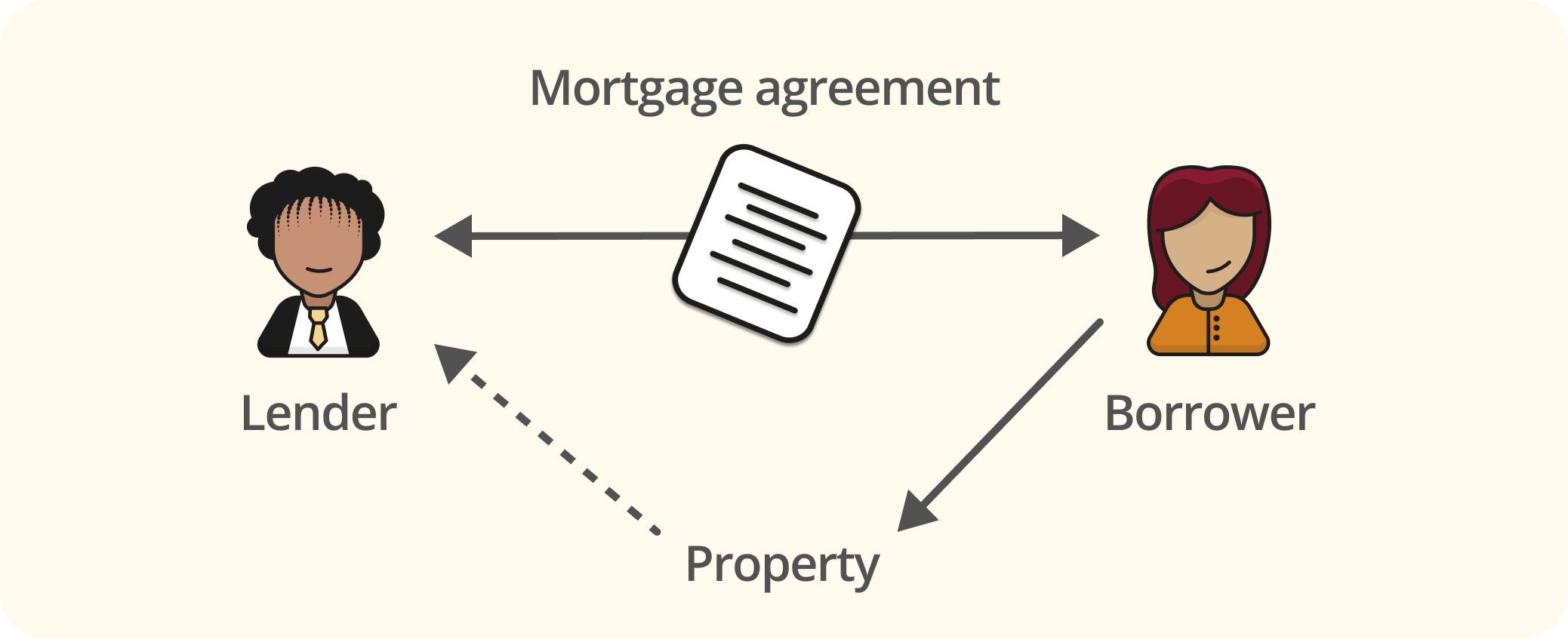

What is a mortgage?

A mortgage is an agreement between a borrower and a lender (generally a bank or building society) whereby the lender will loan money to the borrower so they can purchase property, and in exchange, the borrower will repay the loan over time plus interest (ie the extra amount paid on top of the debt already owed at a rate agreed by the borrower and lender) and provide some ‘security’ over assets they own until the loan is paid off.

The security which the borrower provides will generally give the lender certain rights over the legal interest in the property purchased by the borrower, until the loan debt is repaid, whilst the borrower retains the full beneficial interest that allows them to live there. If the borrower defaults on a mortgage repayment, then the lender may be entitled to exercise their rights over the property.

What are mortgage rates and why are they fluctuating?

Mortgage rates are interest rates imposed on borrowing money to buy a house. However, the way mortgages work isn’t that simple.

There is no one set mortgage rate, as these rates vary from lender to lender, depending on their pricing schemes and risk appetites. In addition, because there is no one set mortgage rate, these rates can fluctuate monthly, typically based on the base interest rate set by the Bank of England (ie the ‘Bank Rate’), especially for variable-rate and tracker-rate mortgages.

Chris Aubeeluck, Head of Business Development at Osbornes Law, says, “In the UK, consumers or borrowers are protected by the Financial Conduct Authority (FCA) who ensures that mortgage contracts are fair, including all the changes associated with it, and for lenders to conduct thorough affordability assessments to its customers.”

Many factors contribute to mortgage rates' fluctuation, including inflation, housing market conditions, global and political events, government policies, and a country's overall economic performance.

1. Inflation

Inflation is the rise in prices over time and the rate of inflation measures how quickly prices are increasing. If the Bank of England raises the Bank Rate to combat the variables causing inflation, it will also raise mortgage rates. However, inflation does not dictate the rise in mortgage rates and other factors can also cause the Bank of England to increase the Bank Rate.

2. Overall economic performance

By considering the principle of supply and demand, we will understand how economic performance affects mortgage rates. When an economy is performing well – with people having higher wages and more disposable income for housing mortgages – there will be an uptick in mortgage loans, which could push lenders to increase their mortgage rates as well.

3. Housing market conditions

Regardless of the Bank Rate, lenders can increase mortgage rates in times of strong housing demand because they simply have more borrowers than capital to lend out. This allows them to manage their capital (ie the net financial resources that a bank owns which act as a safeguard against unexpected losses) and risk (ie the risk of financial loss or financial instability) carefully.

“Just like manufacturing industries, whose main drivers of success and profitability are pricing schemes and cost management, lenders can also raise or lower their mortgage rates despite the stability of the Bank of England’s base rate to make a profit – highly driven by increased overhead costs,” says Leon Huang, CEO at RapidDirect.

Common types of mortgages

Because of the fluctuations in mortgage rates, consumers or borrowers can choose between different types of mortgage rates that best suit their risk appetites when it comes to monthly payments:

Fixed rate mortgage

A fixed rate mortgage allows you to pay a fixed monthly amount based on an initial interest rate for a certain period, typically two to five years, no matter what happens to the market or overall economic conditions. However, after the fixed rate period ends, you will pay based on a standard variable rate (ie the base interest rate set by a particular lender which may change year-on-year) for the remaining period, which is typically consistently higher than the fixed rate. This is the most common type of mortgage loan as it generally provides the borrower with a higher level of stability, especially when there is economic uncertainty.

One disadvantage of a fixed rate mortgage is that while you pay a fixed amount for a specific period, you may also miss out on savings when the future standard variable mortgage rate becomes lower than your fixed rate.

Tracker rate mortgage

In a tracker mortgage, you will generally pay the Bank Rate plus an additional fixed percentage on top of this as set by the lender every month for between two to five years. You can also consider a tracker mortgage as a type of variable rate mortgage because your monthly payments will increase or decrease if the Bank Rate goes up or down. It’s known as a ‘tracker’ mortgage because it tracks the Bank Rate and varies respectively.

After the initial tracker rate mortgage period, you will likely be subject to a standard variable rate mortgage.

Standard variable rate mortgage

Standard variable rate mortgages (ie ‘SVR mortgages’) are another type of variable rate mortgage and are usually the most expensive option, as standard variable rates are set by each lender based on the Bank Rate and are typically higher than the Bank Rate.

Most borrowers will often end up paying a variable rate for the rest of their loan term without a switch (ie changing your existing mortgage deal to a different deal with the same lender) or remortgage deal (ie replacing your existing mortgage deal for a new one with a different lender) once their fixed term mortgage ends. Their monthly interest payments will fluctuate depending on the Bank Rate and the lender.

However, with an SVR mortgage, you are not locked into a specific deal. You can generally switch or remortgage your loan or make early repayments without an additional charge.

Rob Gold, VP of Marketing Communications at Intermedia, says, “Proper communication is crucial in ensuring that both parties are aware of the conditions, pros, and cons of each type of mortgage rate, especially when the rate needs to be changed after a specific period. Lenders must set up effective communication tools with their borrowers to seamlessly relay and communicate important contract and business data.”

How mortgage rates may change in 2025

The current Bank Rate as set by the Bank of England is 4.25% as of 8 May 2025. From a 16-year high of 5.25%, it was reduced to 5% in August 2024, 4.75% in November 2024, and 4.50% in February 2025.

This is good news for those with tracker rate and variable rate mortgages, as monthly repayments have lowered by 0.25% since November 2024. However, further cuts from 4.50% aren’t likely to happen soon due to inflation rates predicted to increase to 3.7% in the middle of 2025 – well above the Bank of England’s Monetary Policy Committee’s (MPC) inflation target of 2%.

While interest rates remained at 4.50% in March, Bank of England Governor Andrew Bailey reiterated that they are on a ‘gradual declining path’. This may also mean lower mortgage rates or monthly payments for home buyers in the latter half of 2025, when the inflation rate is predicted to drop back to around 2%.

Andrew Bates, COO at Bates Electric, says, “Energy prices, including gas and electricity prices, are also key factors in managing a country’s overall inflation rate because of their direct impact on transportation and the production of essential goods and services.” He adds, “When energy prices fluctuate, so does the cost of making a product, which is then passed to the price consumers pay.”

Impact of mortgage rate fluctuations on homebuyers

The impact of mortgage rate fluctuations on homebuyers is mainly on their gain or loss, depending on the mortgage rate they are presently using.

“For homebuyers, carefully monitoring your calendar, the time frame of your repayments, and your fixed rate payment periods, if applicable, will help save you from losses when it comes to mortgage rate changes, especially when you’re transitioning from fixed rate to variable rate or looking for better deals through remortgages,” says Jacob Barnes, Co-Founder of FlowSavvy.

Homebuyers currently on a fixed rate mortgage won’t see an impact on their monthly repayments; however, those who have taken out a higher fixed rate mortgage in the past year would not benefit from the recent cuts on the Bank Rate.

If a homebuyer is on an SVR mortgage, the recent Bank Rate cuts would have likely positively impacted their monthly repayments. However, lenders may or may not have passed the reduced cuts to their borrowers. Where this is the case, borrowers on an SVR mortgage may want to consider remortgaging to save more money.

Those on a tracker rate mortgage are likely assured of a 0.25% cut on their monthly mortgage payments due to the 4.75% to 4.50% decrease in the Bank Rate from November 2024 to February 2025.

John Grant, Founder & CEO at Premier Bidets, says, “Homebuyers aiming for smart financial moves must consider not only their current financial capacity, but their risk appetites and long-term financial plans as well.” He adds, “Before deciding, they should seek tools and platforms that can easily help compare the pros and cons of each lender, as well as the cost-savings and opportunity loss for each type of mortgage rate computation.”

Outlook for homebuyers

Homebuying is a significant investment and risk for those seeking a permanent home in an age of a housing crisis, unpredictable inflation, and mortgage rates.

While factors like inflation, global events, and overall economic performance are things homebuyers have no control over, understanding mortgage rate fluctuations and the pros and cons of each type of mortgage will help in assessing your mortgage payment gains or losses – taking into consideration your present financial condition, the amount of risk you’d want to take on for your home loan, or your long-term plans for your mortgage payments.

This article does not make or seek to make personal advice or any recommendations regarding financial products or services which are regulated by the Financial Conduct Authority (FCA). Nor does Rocket Lawyer provide any advice or services relating to any FCA regulated activities, as we are not regulated or authorised to give advice by the FCA.