What is stamp duty land tax?

Stamp duty land tax (SDLT), or simply ‘stamp duty’, is a tax you pay when you buy or transfer a freehold or leasehold property or land over a certain price.

It's a progressive tax, which means you pay different rates on different portions of the property's price. You only pay the rate for the part of the price that falls within each band.

What are the standard stamp duty rates for a main home?

When you buy the home you're going to live in (your 'main residence' or 'main home'), the standard SDLT rates (as of 1 April 2026) are:

-

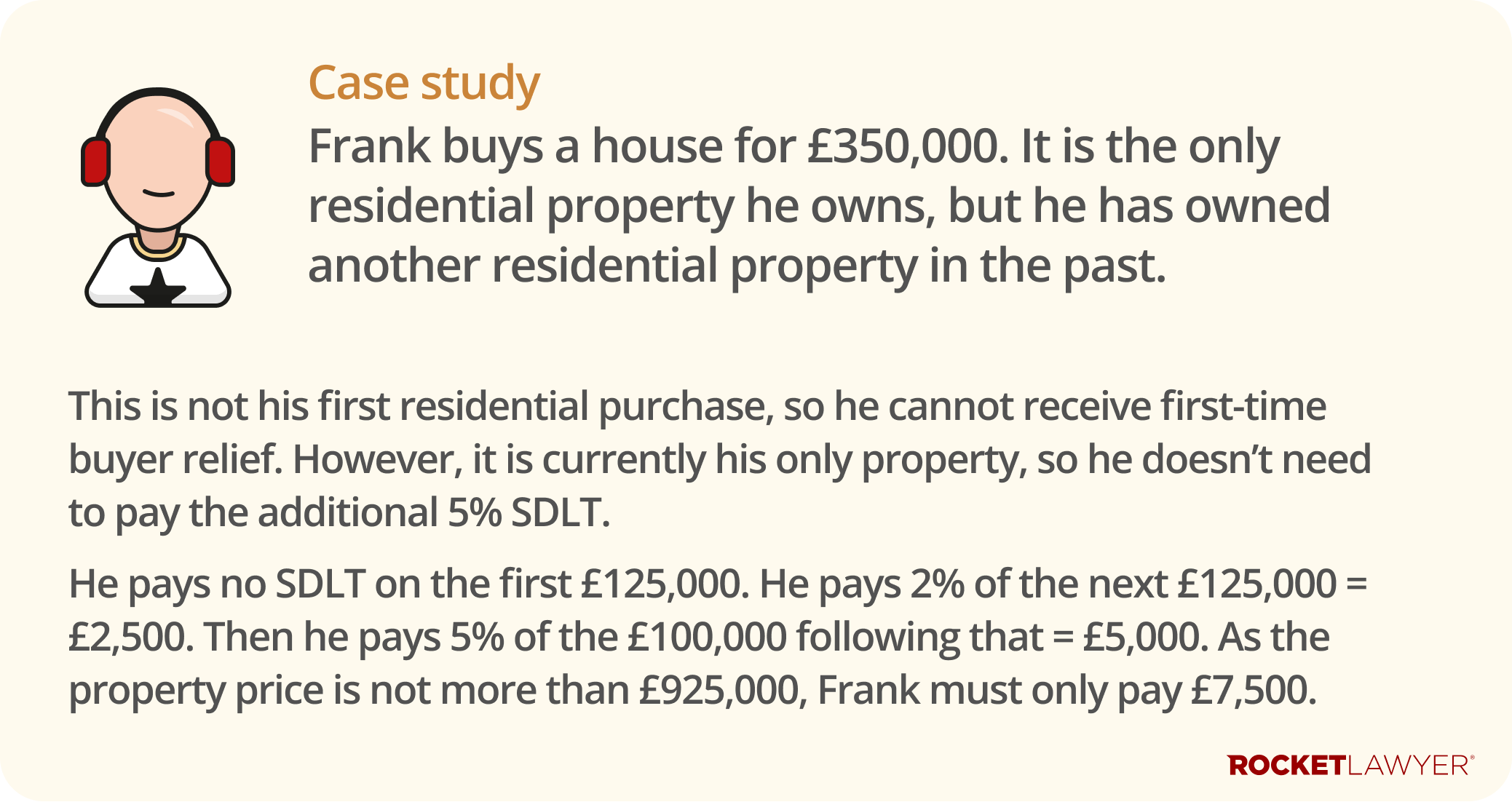

0% on the portion of the price up to £125,000

-

2% on the portion from £125,001 to £250,000

-

5% on the portion from £250,001 to £925,000

-

10% on the portion from £925,001 to £1.5 million

-

12% on the portion over £1.5 million

Are there different rates for first-time buyers?

If you're a first-time buyer, you can get a discount (known as 'relief'). To qualify, you (and anyone you're buying with) must have never owned a home anywhere in the world.

First-time buyers pay:

-

0% on the portion of the price up to £300,000

-

5% on the portion from £300,001 to £500,000

Note that if the property price is more than £500,000, you cannot claim this relief and must pay the standard SDLT rates listed in the section above.

What about buying an additional property?

If you're buying a property that means you'll own more than one (like a buy-to-let or a second home), you'll have to pay a higher rate of SDLT.

These higher rates apply to any additional residential property bought for £40,000 or more. The rates are:

-

5% on the portion of the price up to £125,000

-

7% on the portion from £125,001 to £250,000

-

10% on the portion from £250,001 to £925,000

-

15% on the portion from £925,001 to £1.5 million

-

17% on the portion over £1.5 million

What if I'm replacing my main home?

This is a common situation where the rules for additional properties can be confusing.

If you buy a new main residence, but there's a delay in selling your previous main residence, you'll own two properties for a short time. Because of this, you'll have to pay the higher SDLT rates (including the 5% surcharge) when you buy your new home.

However, you can claim a refund for this surcharge from HMRC if you sell or give away your previous main residence within three years of buying your new one. You must apply for this refund within 12 months of selling your old main residence.

What if I'm a non-UK resident?

If you're not a UK resident, you'll typically be required to pay a 2% surcharge in addition to the standard SDLT rates (or the higher rates for additional properties). You're generally considered a non-UK resident if you were outside the UK for at least 183 days (ie six months) in the 12 months before the purchase.

What about SDLT for non-residential property?

SDLT also applies to non-residential (or 'commercial') and 'mixed-use' properties. Non-residential property includes things like offices, shops, factories, and agricultural land. Mixed-use property has both residential and non-residential parts (eg a flat connected to a shop).

When you buy a freehold non-residential property, the SDLT rates are:

-

0% on the portion up to £150,000

-

2% on the portion from £150,001 to £250,000

-

5% on the portion over £250,000

The rules are different if you're buying a new non-residential or mixed-use leasehold property. In this case, you pay SDLT on two different figures:

-

the lease premium (ie the purchase price for the lease). This is taxed using the same non-residential rates as above

-

the Net Present Value (NPV) of the rent you'll pay. The NPV is the total value of the rent over the life of the lease

These two calculations are done separately and then added together to get your total SDLT bill.

The SDLT rates for the NPV are:

-

0% on the NPV up to £150,000

-

1% on the portion of the NPV from £150,001 to £5,000,000

-

2% on the portion of the NPV above £5,000,000

If you're buying an existing lease (known as an 'assigned' lease), you typically only pay SDLT on the price you pay for the lease itself (ie the premium), not on the NPV of the rent. Ask a lawyer to find out more.

Are there any exemptions from SDLT?

In some situations, you don't have to pay SDLT or file a return. The most common exemptions are:

-

property is transferred as part of a divorce or the dissolution of a civil partnership

-

property is left to you in a will

-

property is a gift, and there's no mortgage to take over

-

the total price is less than £40,000

For more information, see the government’s guidance on SDLT reliefs and exemptions.

When do I have to pay SDLT?

You have 14 days to file an SDLT return and pay the tax. This deadline runs from the effective date of the transaction, which is usually the day you complete the purchase (when you get the keys).

Your lawyer or conveyancer will almost always handle this for you. They'll submit the return to HMRC, pay the tax on your behalf (using the money you've given them), and then add this service to their final bill. However, it's important to remember that as the buyer, you are the one ultimately responsible for making sure it's paid on time.

Do any other taxes need to be paid when property is sold?

SDLT is a tax on buying property, but other taxes can apply when you sell a property. The most common are:

-

capital gains tax (CGT) - this is a tax on the profit you make when you sell an asset that has increased in value. You don't usually pay it when selling your main home, but it's often payable if you sell a second home, a buy-to-let property, or commercial property

-

annual tax on enveloped dwellings (ATED) - this is an annual tax payable mainly by companies that own UK residential property valued at more than £500,000. If a company sells a property, it may also have ATED-related capital gains to consider. For more information, see the government's guidance on ATED

For more information, including on how to apply for refunds and special SDLT rates, see the government's guidance on SDLT. You can also use the government's SDLT calculator to estimate the amount you'll need to pay. If you have any questions about a property purchase, do not hesitate to Ask a lawyer.