What is stamp duty?

SDLT (often simply referred to as ‘stamp duty’) is a form of taxation that applies to freehold or leasehold property that is purchased or transferred in exchange for payment. The purchaser or recipient of the property must generally pay the correct amount of stamp duty to HMRC within 14 days of completing the purchase and they must submit an SDLT return. Even if no stamp duty payment is due, an SDLT return should usually be submitted. Late returns can incur penalties (see the Government's guidance for further information).

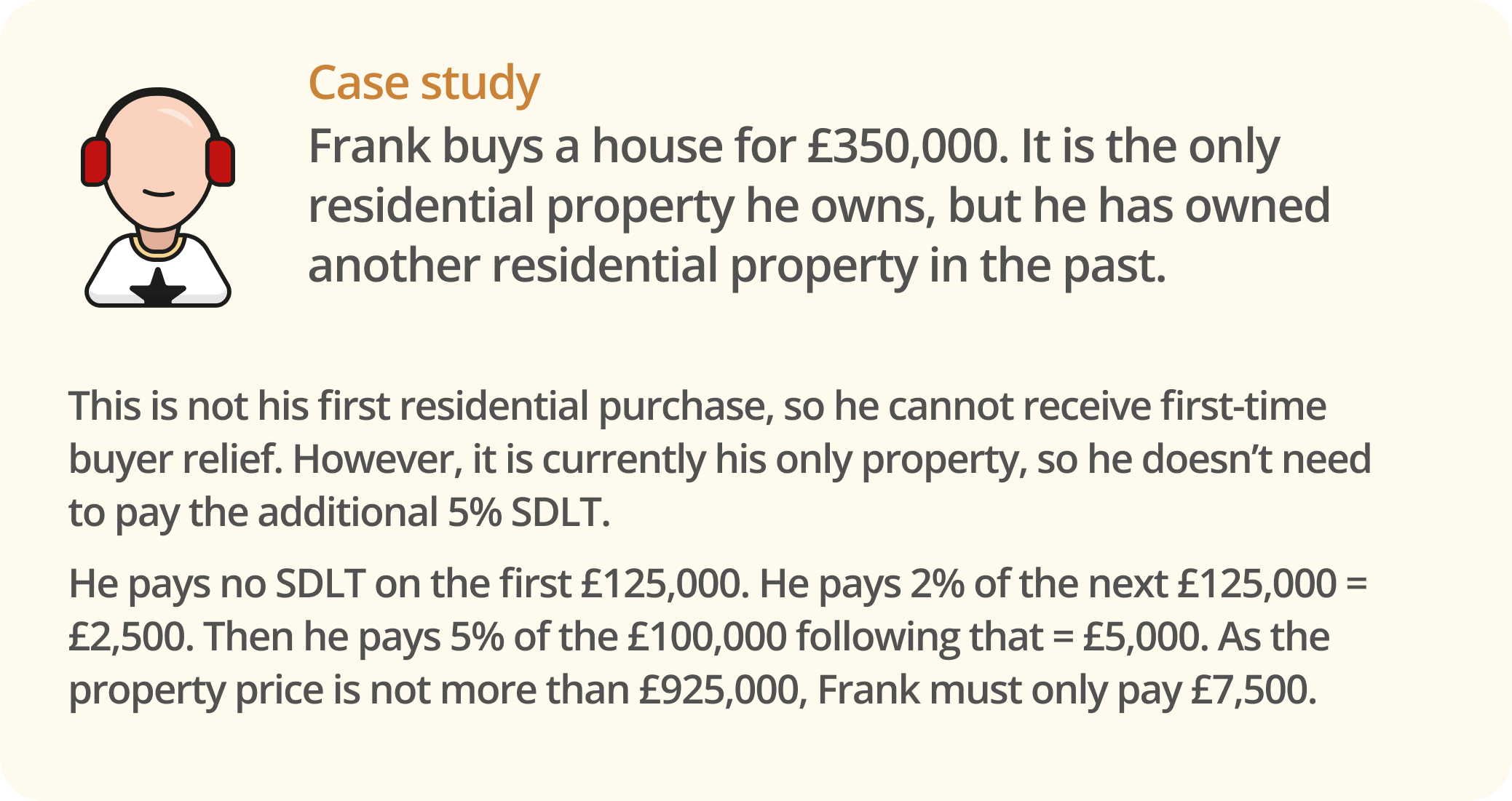

What are the standard stamp duty rates?

The standard SDLT rates usually apply when you’re buying a property that’s not your first home or if you’re buying your first home for more than £500,000.

As of 6 April 2025, the SDLT base threshold is £125,000 for residential property. This means that property that is purchased for less than £250,000 (or which is worth less than this amount if it is being transferred in a manner other than outright purchase, for example, when two people marry) is not liable for SDLT.

SDLT will generally be charged on property purchased above this value. As of 6 April 2025, the SDLT rates are:

-

for any portion of the price/value up to £125,000 = 0%

-

for any portion of the price/value up to £125,001 and £250,00 = 2%

-

for any portion of the price/value between £250,001 and £925,000 = 5%

-

for any portion of the price/value between £925,001and £1.5 million = 10%

-

any portion of the price/value above £1.5 million = 12%

You must usually pay an additional 5% of the price/value of your purchase in SDLT if you purchase a residential property whilst you already currently own another residential property. This additional 5% usually does not apply if you are buying a residential property to replace your current main residence.

These rates apply both to sales and transfers of freehold property and to purchases of new leases of a leasehold property. Purchases of leases can involve more complex calculations. Read the Government’s guidance for more information.

See the Government’s guidance for up-to-date SDLT rates, for information on special rates of SDLT, and to access the SDLT calculator.

How much stamp duty will I pay if I am buying my first home?

If you are buying your first home you can claim a first-time buyer relief on stamp duty land tax. As of 6 April 2025, you will qualify for this tax relief if you are purchasing the property:

-

as your first home (a residential property) and any other people you are buying with are also buying their first home

-

for £500,000 or less, and

-

after 30 September 2021

If you are eligible for this tax relief, when you purchase your property you will need to pay SDLT at rates of:

-

for the portion of the purchase price up to £300,000 = 0%

-

for the portion of the purchase price between £ 300,001 and £500,000 = 5%

Note that, although 5% will still sometimes be charged when the relief applies, you will still be paying less SDLT than you would without the relief. If your new house price is over £625,000 the standard rules apply (see below).

What happens if I sell my main residence and move into a new property as my main residence?

If you buy a new main residence but there’s a delay in selling your previous main residence, you’ll have to pay the higher stamp duty rates (ie including the additional 5%, described above) as you’ll own two properties.

If you sell or give away your previous main residence within 3 years of buying your new residence, you can apply for a refund of the higher rate SDLT that you paid.

In this situation, you must generally apply for any repayment within 12 months of the sale of your old main residence.

What if property is being bought by non-UK residents?

A 2% SDLT surcharge usually applies when non-UK residents buy residential property (regardless of whether they already own property).

This surcharge applies to almost all SDLT payments and is separate from the 5% SDLT surcharge that applies to second homes and additional residential property purchases (this will also need to be paid if applicable). This means that the top SDLT rates can increase to a maximum of 17% for some non-UK resident buyers.

For the purposes of SDLT, a non-UK resident is someone who is not present in the UK for at least 183 days (ie 6 months) during the 12 months before the property purchase.

See the Government's guidance for more information on this SDLT surcharge and when it applies and to access the SDLT calculator.

What happens when property is transferred or left in a will?

There is generally no stamp duty to pay in respect of inherited property that has been left in a will.

Property which is transferred as a gift during someone’s lifetime is liable for stamp duty if there is an outstanding mortgage; SDLT will be applied to the value of the remaining mortgage.

For stamp duty liability on other types of property transfer, see the Government's guidance.

How does stamp duty affect shared ownership property?

When purchasing a shared ownership property via a shared ownership scheme run by a public body (eg a housing association or local housing authority), there are two options available for paying SDLT:

-

market value election - stamp duty is paid based on the total value of the property, which covers any future additional equity share purchased

-

staged payment - this involves an initial SDLT payment on the ‘lease premium’ (the amount you paid for the lease) if it falls above the SDLT threshold (ie £125,000 under the standard rates set out above). There is usually an additional 1% SDLT payment due if the total rent over the life of the lease (called the 'net present value') is over £125,000

For more information on stamp duty and shared ownership, see the Government's guidance.

Are there any exemptions?

Normally, even if SDLT does not need to be paid because the price of a property falls below the threshold, an SDLT return must be filed. However, there are certain situations in which SDLT doesn’t need to be paid and a return doesn’t need to be filed. These include when:

-

a freehold property is purchased for less than £40,000

-

property is transferred due to divorce or dissolution of a civil partnership

-

property is left in a Will

-

no money or payment changes hands (ie the property is a gift and there’s no mortgage involved)

For further information on SDLT exemptions and reliefs, see the Government's guidance or Ask a lawyer for assistance.

Do any other taxes need to be paid when property is sold?

Some other fairly common taxes may need to be paid when a property is sold. For example:

-

Capital Gains Tax (CGT) - this is a tax charged on profits made when somebody sells an asset that has increased in value. It may be applicable if, for example, you sell a second home. For more information, read Capital gains tax

-

Annual Tax on Enveloped Dwellings (ATED) - often, if a company sells residential property in the UK that’s worth more than £500,000, they must pay ATED and complete an ATED return. For more information, read the government’s guidance on ATED