Private rented accommodation

Many students rent accommodation from a private landlord. Depending on the type of tenancy you have, your rights and responsibilities will be different.

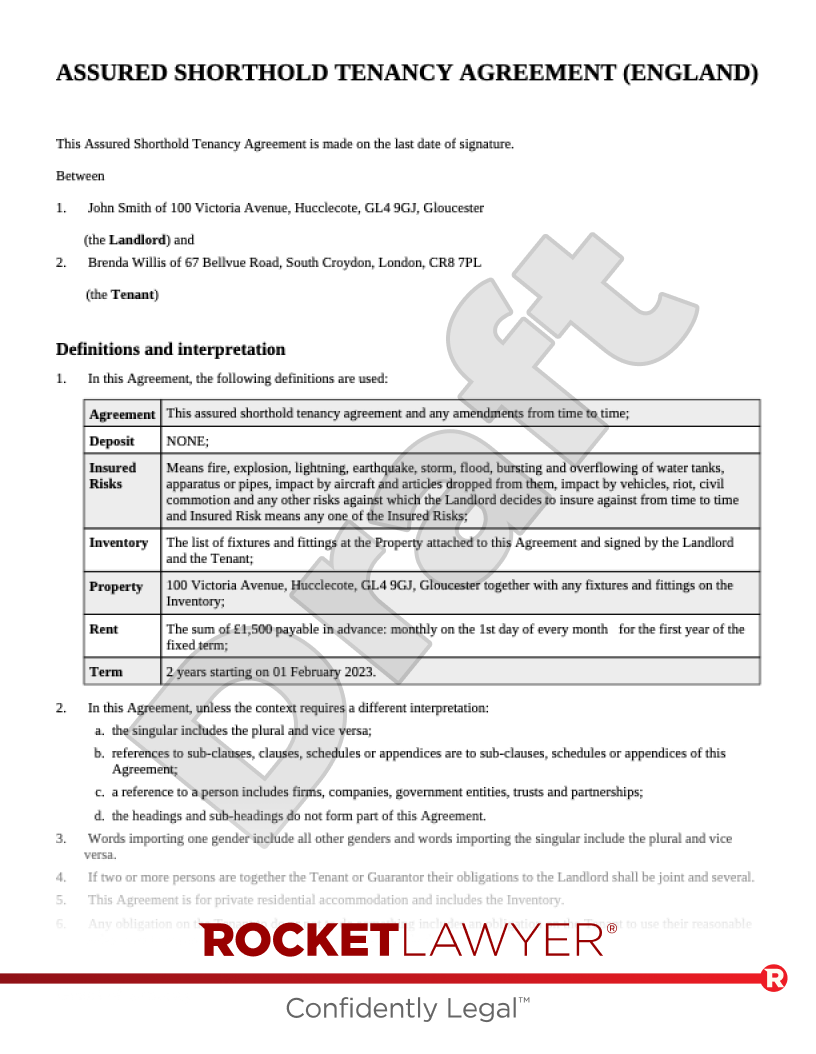

Assured shorthold tenancy in England

If the accommodation is self-contained (ie the landlord doesn’t live in the property with you) you most likely have an assured shorthold tenancy (AST), which can be short-term or long-term.

Under this type of Tenancy agreement, tenants are entitled to several rights regarding safety, property repairs, the fitness of the property for human habitation and eviction. For more information about your rights as an assured shorthold tenant, read Tenant's rights.

Many students choose to share accommodation with other students. Various types of tenancy arrangements can exist, including:

-

joint tenancies - all students sign a single tenancy agreement, have equal rights and responsibilities in the property and pay an individual contribution towards the rent

-

sole tenancies - each student has their own individual tenancy agreement with exclusive possession of a specific room, and pays rent individually. Failure to pay rent or eviction of one student tenant doesn't affect other student tenants' tenancies

-

sole tenancy signed by one student - one student signs a tenancy agreement for the whole property and sublets rooms to other students as lodgers (provided the landlord agrees to it)

Students who share accommodation often live in houses in multiple occupation (HMO). If the property you live in is an HMO, your landlord has extra responsibilities (eg specific fire safety obligations) and may need a licence for the property.

If you share a property with other full-time students only, you do not have to pay council tax. You will generally need to apply for a council tax exemption. If the people you house-share with are not all full-time students, you may qualify for a council tax discount.

Occupation contracts in Wales

From 1 December 2022, most residential properties in Wales are let out on occupation contracts under the Renting Homes (Wales) Act 2016. This means that if you’ve found a house or flat to rent, you will typically sign a Standard occupation contract with the landlord. This contract governs the relationship between you (as the ‘contract holder’) and your landlord and sets out your respective rights and responsibilities. For more information, read Tenant’s rights.

A dwelling can be rented to:

-

a single contract holder (ie one student over the age of 18) signing an individual occupation contract

-

joint contract holders (ie multiple students over the age of 18) signing one occupation contract. Each joint contract holder is fully responsible for all obligations under the contract

Under the Renting Homes (Wales) Act 2016, joint contract holders can leave the occupation contract without ending the whole contract. This means that one student can move out and leave the contract without the contract ending for all other student contract holders. New joint contract holders can also be added to a joint contract without the contact holders having to end the current contract and start a new one.

For more information, read Residential tenancies in Wales.

Sharing a home with your landlord

In England

In England, lodgers (as opposed to assured shorthold tenants) have limited rights in the property.

Some students prefer to rent a room directly in the landlord's property. This type of housing arrangement is known as a Lodger agreement, whereby the occupier (known as a 'lodger) has their own room but shares common facilities (such as a kitchen and bathroom) with the landlord. As opposed to assured shorthold tenants, lodgers have limited rights in the property. For example, they don’t have exclusive use of the room and can be evicted at any time.

In Wales

In Wales, the rights of a lodger depend on the type of contract they have. If their agreement with the landlord is an occupation contract, they will have greater protection. Under the Renting Homes (Wales) Act 2016 a lodger will not have an occupation contract if:

-

they share accommodation with their landlord under an agreement, and

-

immediately before they entered into an agreement with the landlord, the landlord occupied the property as their only or main home

However, such a lodger agreement can become an occupation contract if the landlord notifies the lodger that their contract is an occupation contract. For more information, read Residential tenancies in Wales.

Deposit and guarantor

As a condition of letting accommodations to students, most private landlords ask for a deposit and require a third party to act as a guarantor for rent payments.

A guarantor is someone - usually a parent or close relative - who agrees to pay for your rent if you don't pay it. The guarantee agreement between the guarantor and the landlord must be in writing. In the case of joint tenancies shared by several students, it's common for the guarantee to apply to all of the rent.

As for the deposit, under an AST, it must be protected in a Government-approved scheme, which ensures you’ll get your money back at the end of the tenancy. Your landlord must also provide you with certain prescribed information related to your deposit within 30 days of receiving it. For more information about deposits, read Deposit protection schemes.

University accommodation

Many universities in the UK give their students the possibility to live in halls of residence near or within the university campus. University halls can offer different types of accommodation, such as rooms in shared residences or individual studio flats.

Depending on the universities, accommodation in halls can be available for term-time or for the full calendar year, and rent is often due at the beginning of each term. The price for accommodation usually includes bills for heating and water. Students who live in university halls are automatically exempt from paying council tax.

Educational institutions offering students accommodation must provide safe and good quality accommodation and are required to belong to a Government-approved code that sets out safety, security and maintenance standards. These codes are the:

-

Universities UK/Guild HE Code of Practice for the Management of Student Housing (simply known as the ‘Student Accommodation Code’)

-

Accreditation Network UK (ANUK)/Unipol Code of Standards for Larger Residential Developments

Your university should tell you which code they have signed up to.

Halls of residence can also be managed by private companies that are not linked to a specific university. In such a case, the letting will usually take the form of a shorthold tenancy agreement and the private company should comply with the ANUK/Unipol Code of Standards for Larger Developments for student accommodation not managed and controlled by educational establishments.

How to find a student let?

Application to university halls of residence is usually made directly through the university website.

As for private rented accommodation, many students find it through a letting agent who can help student tenants (or student contract holders) find accommodation. Bear in mind that since 2019, under the Tenant Fees Act 2019, letting agents can only charge certain lawful fees in connection with a tenancy.

For more protection, it’s advisable to choose a letting agent that has signed up to a letting scheme, such as:

For more information on finding a rental property, read What to consider when renting residential property and follow our Moving in checklist for tenants.