What is a share purchase?

A share purchase is the process of buying a company by acquiring its shares. Unlike an asset purchase, where a buyer picks specific assets, a share purchase means the buyer takes control of the entire corporate entity. The company continues to exist with its own legal identity, but simply with a new owner. This means all of its history (both good and bad) is transferred to the buyer. This includes all assets, employees, contracts, and, crucially, all liabilities, whether they are known or have not yet been discovered.

In other words, a share purchase constitutes the purchase of a company’s operating business, but none of the existing contracts with the company change. If a shareholder sells their shares in a company, then they achieve a complete break in the relationship between them and the company.

What are share purchase agreements?

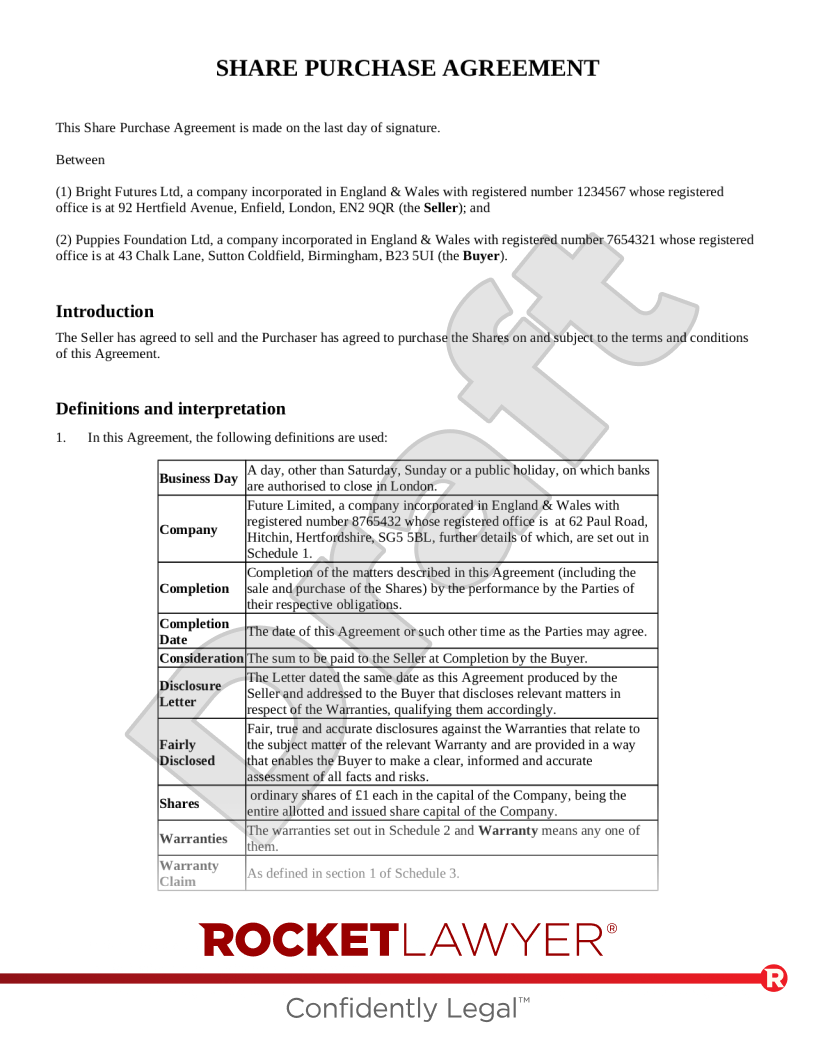

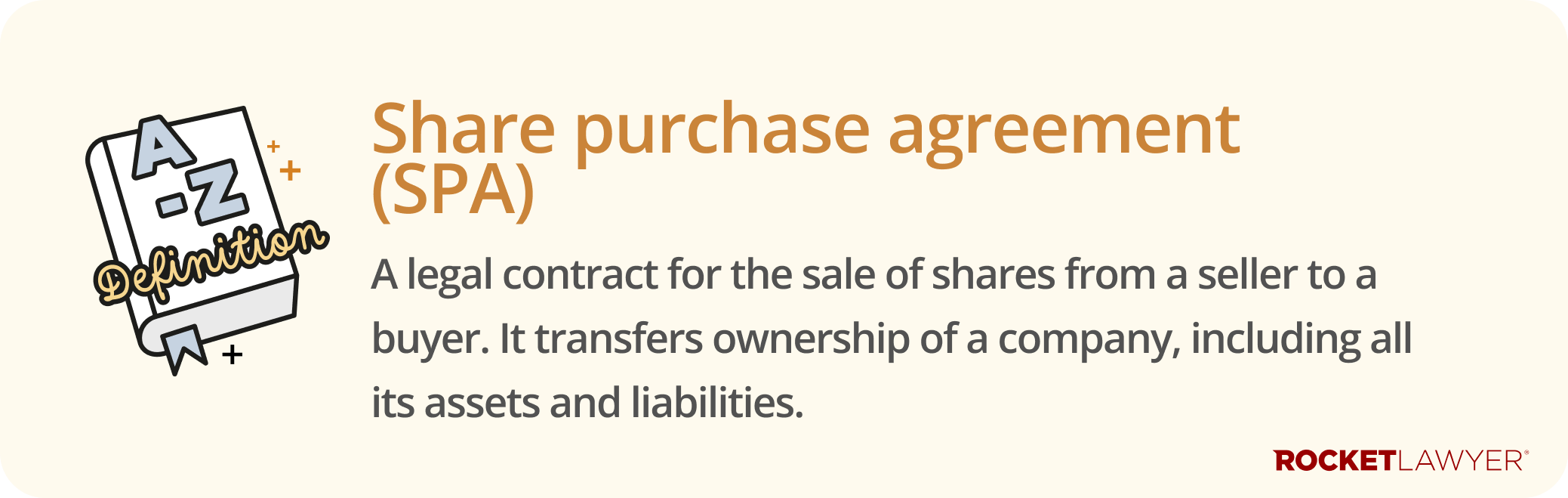

A Share purchase agreement (SPA) is a legally binding contract that formalises the sale of shares from a seller to a buyer. It sets out all the agreed terms, including the price, the number of shares being sold, and the date the transfer will happen (known as 'completion'). The SPA's main job is to protect both parties. For the buyer, it includes vital promises from the seller about the state of the business. For the seller, it clearly defines the limits of their future liability. It’s the single source of truth for the entire deal.

A typical SPA will deal with the following matters:

Selling the shares

Once the shares in the target business have been transferred, ownership will pass to the buyer. The buyer is likely to want to appoint new directors, auditors, etc, and may also want to remove the current officers.

Warranties

Warranties are contractual statements made by the seller on completion relating to the target business. They have two purposes:

-

to 'flush out' any information which the buyer ought to know and which could affect the value of the company, or even the buyer’s decision to buy the business

-

to give the buyer some comfort in the event that the business is not as the seller represented to them (eg the company may have some hidden problem or litigation)

While warranties are beneficial, the party giving them must be able to stand by them. When a buyer purchases shares, any warranties given by the seller are given personally by them. For more information, read Warranties in share purchase agreements.

Restrictive covenants

Restrictive covenants prevent the seller from competing with the buyer for a limited time once the sale is finalised. They may include:

-

non-competition clauses that prevent the seller from setting up a business in competition with the buyer

-

non-solicitation clauses that prohibit the seller from soliciting the buyer’s customers or suppliers

On their face, restrictive covenants are particularly important for the buyer, as immediate competition by the seller could harm the new business or significantly impair it. The covenant in question must be no more than adequate to protect the business interest, the reasonableness of the duration or scope of any restraint being tied to the nature of the interest in question.

What are the advantages of a share purchase?

Business continuity

A key advantage is the seamless continuation of the business. Since the legal entity of the company doesn't change, there's minimal disruption. All existing contracts (with employees, suppliers, and customers), licences, and permits typically remain in the company's name and continue as before. This avoids the often complex process of having to reassign or renegotiate these agreements.

No third-party involvement

Because the company's assets and contracts remain with the company, there is no need to get consent from third parties to transfer them, which is often required in an asset sale. The only thing being transferred is the ownership of the shares themselves. This can make the administrative process of the sale much simpler, quicker, and more discreet than an asset purchase.

No liability for debts

At completion, the seller will have no liability for the debts of the business, which become the responsibility of the new owners. This is because a company has a separate legal personality from its directors and shareholders. By comparison, if there is an asset sale, then, with a few exceptions (eg employees), the seller will keep all the current liabilities of the business, unless he can negotiate with the buyer to take them over with the business.

Potential tax benefits

A share purchase can be more attractive for sellers from a tax perspective. The proceeds from selling shares are often subject to capital gains tax, and sellers may be able to benefit from tax reliefs such as Business Asset Disposal Relief, which can significantly reduce the amount of tax they have to pay.

What are the disadvantages of a share purchase?

Inheriting outstanding problems and liabilities

This is the most significant risk for the buyer. When you buy the shares, you buy the company's entire history, including all its current and future liabilities. This means the buyer becomes responsible for everything, including company debts, any ongoing litigation, tax disputes, and even problems from the past that haven't been discovered yet. Unlike an asset sale, you cannot leave unwanted liabilities behind with the seller.

The risks require extensive due diligence

Because the buyer inherits all potential problems, they must conduct a thorough and costly investigation into every aspect of the company before committing to the purchase. This process, known as 'due diligence', is a critical step to uncover any hidden risks, but it adds significant time and expense to the transaction.

Due to this increased risk to the buyer (compared to the risk level associated with asset purchases), warranties are often included in an SPA to protect the buyer. For more information, read Warranties in share purchase agreements.

What are the key stages of a share purchase?

A share purchase follows a structured process to ensure all legal and financial details are handled correctly. It's not just a single event but a journey with several critical stages that must be navigated in the right order.

Initial negotiations and heads of terms

Once a buyer and seller have agreed in principle, they often first outline the deal in a Heads of terms document. This sets out the main points of the agreement, like the price, payment structure, and a proposed timeline. While mostly not legally binding, it establishes a clear roadmap and shows a serious commitment from both sides to proceed with the deal.

Due diligence

This is the buyer's formal investigation. The buyer and their professional advisers will meticulously review the company's financial, legal, and operational health to verify the seller's claims and uncover any potential risks. The findings from this stage are crucial as they will directly impact the final terms and promises included in the SPA.

For more information, read Due diligence.

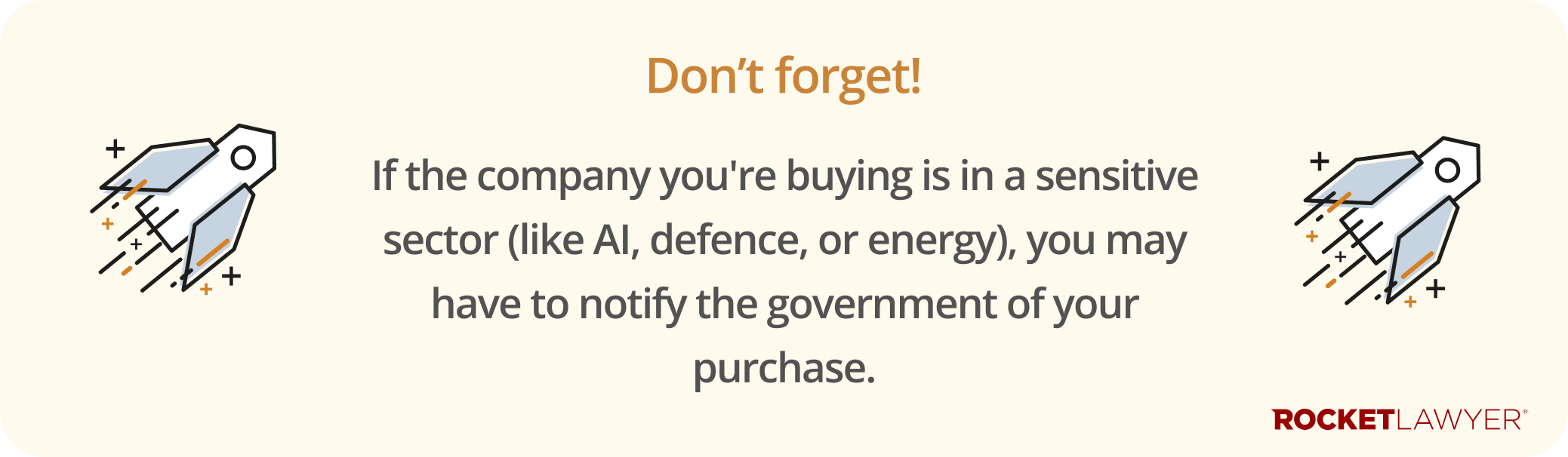

National security notification requirements

Business acquisitions, including share purchases, may require mandatory notification or qualify for voluntary notification to the government under the National Security and Investment Act 2021. Notification enables parties involved in an acquisition to attempt to obtain clearance for their acquisition from the government, removing the risk of their challenging it later on.

An acquisition qualifies for voluntary notification if:

-

the acquisition is of an interest or right in (or in relation to) a certain type of asset or entity (eg a company via share purchase)

-

the asset or entity has a connection with the UK

-

a certain level of control (eg ownership) over the asset or entity is transferred (eg via voting rights), and

-

the acquisition was completed after 12 November 2020

An acquisition of an entity that qualifies for voluntary notification under the criteria above may also require mandatory notification if the entity operates within 17 specified areas of the economy that pose a risk to UK national security (eg artificial intelligence (AI), computing hardware, communications, energy, or transport).

For more information, see the government’s guidance on acquisitions that could harm national security.

Post-completion requirements

After the deal is officially closed, several important administrative tasks must be completed to legally finalise the transfer of ownership. The buyer is typically responsible for these steps, which include:

-

paying tax - the buyer must pay Stamp Duty on the share transfer. This is usually due within 30 days of completion. The Stock transfer form cannot be legally recognised until the duty is paid

-

updating statutory books - the company’s internal legal records (its 'statutory books' or registers) must be updated to show the new shareholder's details and remove the seller's

-

filing at Companies House - the company must notify Companies House of the change in ownership and any changes to the board of directors or the person with significant control (PSC). This is typically done in the company’s next confirmation statement

These steps are essential to ensure the buyer is formally recognised as the new owner and the company remains compliant with UK law.

If you are ready to proceed with a sale, you can make your Share purchase agreement and/or use our business sale or purchase service to assist in buying and selling company shares.

Remember that you can always Ask a lawyer for help with your specific situation.