Managing your partnership’s finances

Effective financial management is essential for the health of your business. This involves keeping accurate records of all income and expenditure, managing a business bank account, and preparing annual accounts according to the correct standards for your partnership type.

Accounting and bookkeeping for partnerships

All partnerships must keep detailed and accurate financial records of their business activities. This is not only good business practice but also a legal requirement for calculating your tax obligations. At a minimum, you should keep records of:

-

all sales and income

-

all business expenses

-

VAT records (if you are VAT registered)

-

PAYE records if you employ staff

-

any business assets bought or sold

These records must be kept for at least five years after the 31 January submission deadline of the relevant tax year.

For more information, read Accounting and bookkeeping.

Preparing annual accounts

General partnerships, limited partnerships (LPs), and Scottish limited partnerships (SLPs) don’t need to prepare annual accounts (unless the general partner is a limited company).

However, as limited liability partnerships (LLPs) have greater administrative burdens, they are required to prepare and file annual accounts with Companies House. The LLP’s designated members must prepare, sign and send annual accounts to Companies House each year, usually within nice months of the LLP’s financial year-end. Note that annual accounts are made public on Companies House. Depending on the size of the LLP, you may also be required to have your accounts audited.

For more information, read Annual accounts and tax returns.

Tax obligations for partnerships

One of the most important ongoing duties is managing your partnership’s taxes. The partnership itself does not pay tax, but it has reporting duties to HMRC, and each partner is individually responsible for paying tax on their share of the profits.

Filing the Partnership Tax Return

Regardless of partnership type, a Partnership Tax Return must be filed for the partnership itself. Who is responsible for registering the partnership for Self Assessments and filing the Partnership Tax Return depends on the partnership type:

-

general partnerships - this responsibility falls to the nominated partner

-

LLPs - this responsibility falls to the designated members

-

LPs - this responsibility falls to the general partners

Each year, the relevant person must file a Partnership Tax Return declaring the partnership's total income and profits, and how they have been allocated amongst the partners.

Failure to file a Partnership Tax Return in time can lead to penalties. Ask a lawyer to find out more.

Personal tax returns for partners

Each partner must complete individual Self Assessment tax returns on their share of profits and submit these annually to HMRC. This can be done online or using Form SA100 on or after 6 April, following the end of the tax year.

Partners will be charged income tax (at the applicable rates in England, Wales, and Scotland) and National Insurance on their share of the partnership's profits.

Failure to file a Self Assessment in time can lead to penalties.

VAT registration

If your partnership’s annual taxable turnover exceeds the VAT registration threshold (ie if your total taxable turnover over the past 12 months is the VAT threshold), you must register the partnership for VAT with HMRC.

Once registered, you are required to charge VAT on your goods or services, keep records of all VAT transactions, and submit regular VAT returns to HMRC, usually on a quarterly basis.

For more information, read VAT.

Partner duties and decision-making

The success of a partnership depends on the partners working together effectively. This is underpinned by both legal duties that apply automatically and the specific rules you set out in your own agreement.

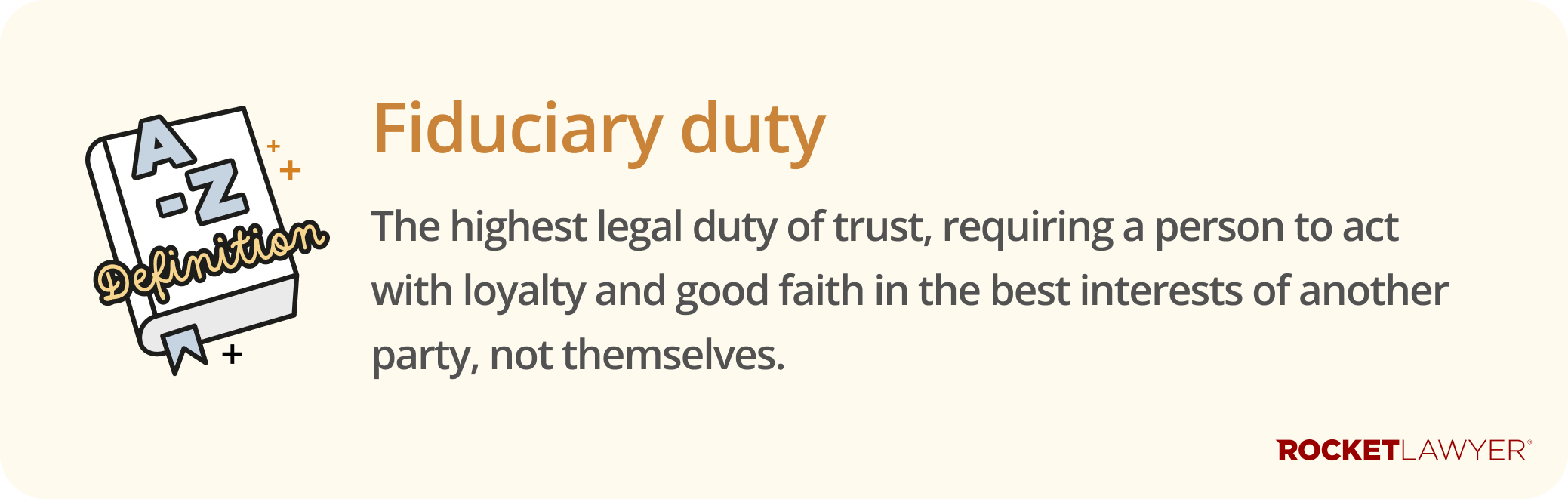

Partners’ fiduciary duties

All partners, regardless of the partnership type, owe a legal fiduciary duty to each other and the business. This is a duty of the utmost good faith and loyalty. It legally requires you to:

-

act honestly and in the best interests of the partnership

-

avoid any conflicts of interest

-

not make a secret profit from your position as a partner

-

account to the firm for any benefits derived from its business or property

These duties apply automatically, even if you don't have a written Partnership agreement or LLP agreement.

Decision-making and management roles

Your partnership or LLP agreement should be your primary guide for how the partnership is run. It is essential for defining how decisions are made (eg by majority vote or unanimous consent), the specific roles and responsibilities of each partner, and the process for resolving any disputes.

In a general partnership or LLP, all partners usually have the right to be equally involved in management unless your agreement states otherwise. Unless a partnership agreement states otherwise, most decisions can be taken by a majority of partners; however, unanimity is required for any fundamental changes, such as when admitting a new partner.

In a limited partnership, only the general partners manage the business. Limited partners are legally prohibited from taking part in management; if they do, they risk losing their limited liability status.

Identity verification

Since 18 November 2025, the Economic Crime and Corporate Transparency Act 2023 requires certain individuals associated with partnerships to verify their identity with Companies House. This is compulsory for:

-

all individual members of LLPs

-

individual people with significant control (PSCs) of LLPs

This will be expanded at a later date to:

-

individual general partners (or the individual registered officer of a corporate general partner) of LPs and SLPs

-

corporate members of LLPs and corporate general partners of LPs/SLPs

New appointees must verify their identity before their appointment is registered, while existing individuals have a 12-month transition period, with their deadline linked to the next confirmation statement filing. For a full breakdown of the identity verification process, read Company roles and appointments.

Ongoing compliance and reporting

Beyond taxes, certain partnerships have ongoing reporting obligations (eg to Companies House to ensure their public records are up to date and accurate).

Requirements for general partnerships

General partnerships have the fewest compliance obligations. There are no annual filing requirements with Companies House. You only need to inform HMRC of any changes, such as a change in the partnership’s name, address, or partners. This will be the responsibility of the nominated partner.

Note that special rules apply if all of the partners are corporate bodies (eg partners who are private limited companies). In these circumstances, the partnership becomes a qualifying partnership (QP) for purposes of accounting disclosure rules. This means that although it is a partnership, it must prepare and file public accounts as if it were a limited company.

Requirements for LPs

The general partners are responsible for the administrative duties of an LP. While LPs do not need to file annual accounts, they must notify Companies House of any changes, including:

-

changes to the partnership name, address, or nature of the business

-

changes to the partners (eg if a partner leaves or a new one joins)

-

changes to a partner’s liability (eg if a limited partner becomes a general partner)

-

changes to a limited partner's capital contribution

-

the LP closing

If you fail to notify Companies House of these changes, you may be committing an offence.

Note that special rules apply if all of the LP’s general partners are corporate bodies. In these circumstances, the LP becomes a QP for purposes of accounting disclosure rules and must draw up and file accounts as if it were a limited company.

Requirements for LLPs

LLPs have the most significant ongoing compliance duties, similar to those of a limited company. The designated members are responsible for ensuring the LLP files the following with Companies House:

-

annual accounts - these must be filed every year and will be made public

-

annual confirmation statements - this confirms the information held on the public register is correct and must be filed every year

-

notifications of any changes (so Companies House can update its central register) - you must report any changes to the LLP’s registered office address, members' details, or your PSCs

Requirements for Scottish general partnerships

Like their English counterparts, Scottish general partnerships generally do not have to register with Companies House. However, if all the partners are corporate bodies (eg limited companies), the partnership becomes a Scottish qualifying partnership (SQP) and must register and report information on their PSCs. For more information, read the government’s guidance on the PSC regime for SQPs.

Requirements for Scottish limited partnerships (SLPs)

The general partners of an SLP have the same duties as those in a standard LP to report any changes to partners or their capital contributions. In addition, SLPs must maintain a register of their PSCs and notify Companies House of any changes to this register.

Successfully running a partnership requires ongoing attention to your financial, tax, and legal duties. While many of these obligations are set by law, a comprehensive and well-drafted Partnership agreement or LLP agreement is the most important tool for managing your internal operations and the relationship between partners.

If you need to formalise your arrangement or have specific questions about your duties, Ask a lawyer.