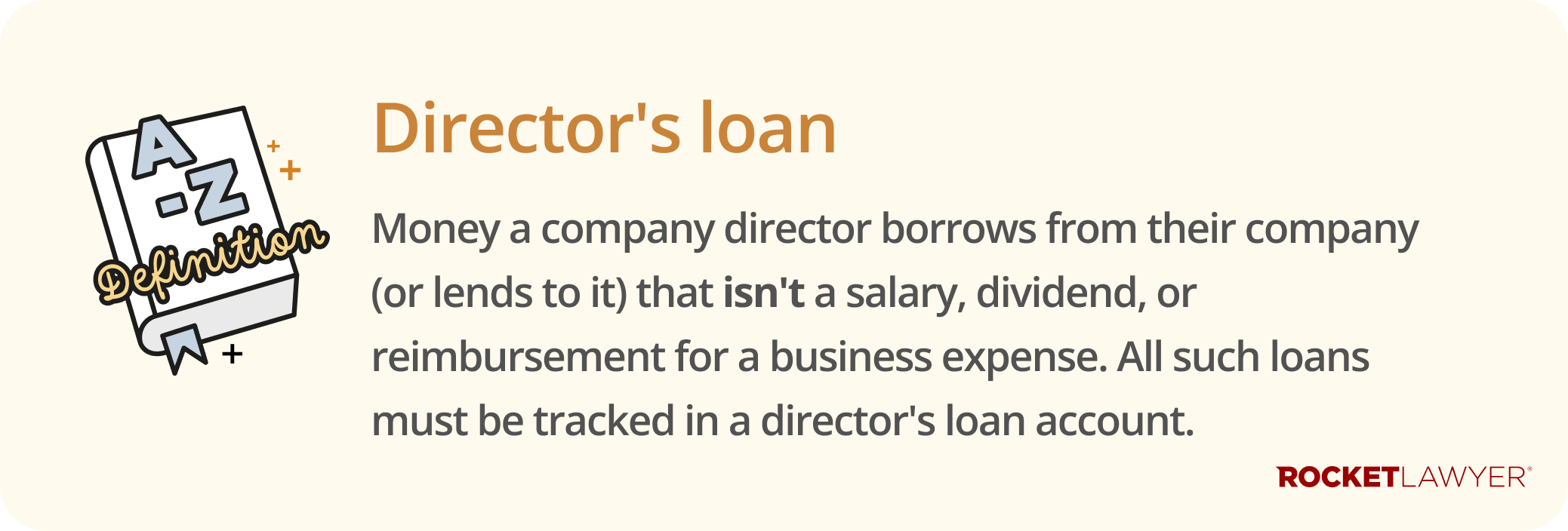

What is a director's loan?

A director's loan is any money a director takes from their company that isn't a salary, dividend, or expense repayment. It also covers situations where you (as a director) lend money to your company. It can even apply to assets that a director uses for personal reasons.

It's good practice to have a formal Loan agreement in place, as it clearly sets out the loan's terms, including any interest and the repayment schedule. This helps avoid any disputes and provides clarity for HMRC.

How is a loan different from a salary or dividends?

It's crucial to distinguish a director's loan from the other main ways you can take money from a company, as each method is treated very differently for tax purposes. The main differences relate to whether the money is a payment for services, a share of profits, or borrowed funds:

-

a salary is a regular payment for your services that's processed through payroll (PAYE), with income tax and national insurance (NI) deducted

-

a dividend is a payment of company profits to shareholders, which doesn't have to be repaid. It’s taxed differently from a salary

-

a director's loan isn't your money to keep, but is money you’ve borrowed from the company that you're legally required to pay back. Because of this, it's subject to its own unique set of tax rules

What is a director's loan account?

A director's loan account (DLA) is the official record kept in the company's accounts of all transactions between a director and the company. It tracks all the money a director has borrowed from or lent to the business.

The balance of this account shows whether the director owes the company money (the account is ‘overdrawn’) or if the company owes the director money (the account is ‘in credit’). This balance must be shown on the company’s balance sheet at the end of its financial year.

What happens if a director owes the company money?

If you borrow money from your company, your director's loan account is considered ‘overdrawn’. When this happens, both you and the business could face extra tax bills if the loan isn't handled correctly.

What tax does the company have to pay on directors’ loans?

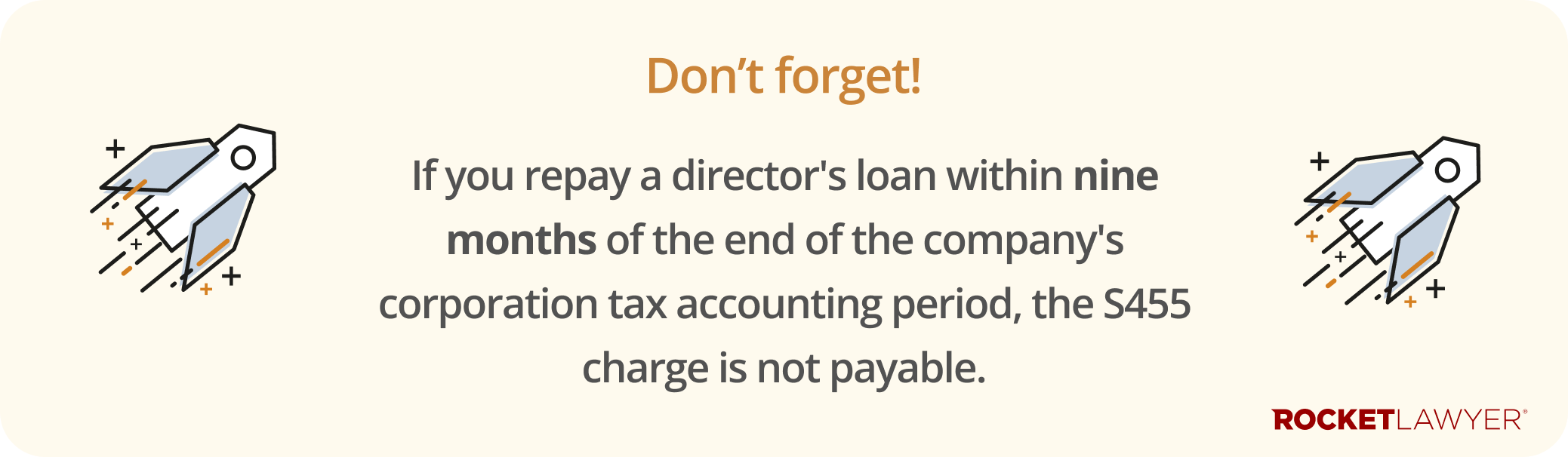

The company might have to pay extra tax if the overdrawn loan isn't repaid on time. This happens if the loan isn't paid back within nine months and one day of the company's corporation tax accounting period.

This tax is called the ‘S455 charge’. It’s a temporary corporation tax of 33.75% on the amount of the loan that is still outstanding after the deadline. The good news is that the company can get this tax back from HMRC, but only after you’ve fully repaid the loan. This can affect the company’s available cash in the short term. For more information, see the government’s guidance on director's loans.

What tax do directors have to pay on directors’ loans?

The loan may be treated as a ‘benefit in kind’. This is a term for any non-cash perk or benefit with a monetary value that you receive from your company. Common examples include private medical insurance or the personal use of a company car. Because these benefits have a value, HMRC considers them a form of income, and they are subject to tax.

Your director's loan is treated as a benefit in kind if:

-

the total amount you’ve borrowed exceeds £10,000 at any point during the tax year, and

-

you either pay no interest or pay interest below HMRC’s official rate

If the loan is a benefit in kind, the company must report it to HMRC on a P11D Form. You must then personally declare the benefit on your Self Assessment tax return and pay income tax on it. In addition to this, the company will also have to pay Class 1A NI on the value of the benefit.

For more information, see the government’s guidance on director's loans.

What happens if a company owes a director money?

The situation is different when your director's loan account is ‘in credit’, which means you have lent personal money to your company. In this case, the company won't have to pay corporation tax on the amount it receives from you.

If the company pays you interest on the loan, this interest is usually a tax-deductible business expense for the company. For you, this interest is personal income, which you must report on your Self Assessment tax return. Your company must deduct basic rate income tax from the interest payments before paying you. It then reports and pays this tax to HMRC each quarter.

What rules apply to directors’ loans?

Director's loans are subject to specific company law and tax rules to ensure they're handled transparently and fairly. This is part of a director's legal obligations to the company.

Getting shareholder approval

Generally, a loan to a director of more than £10,000 needs to be approved by the company's shareholders. This is done by passing a Shareholders' resolution. Failing to get approval when it's needed is a breach of the Companies Act 2006 and can have serious consequences for the director.

Even for loans under £10,000, it’s good practice to document the decision with a directors' resolution to ensure good governance and keep a clear record.

What is 'bed and breakfasting'?

The 33.75% S455 corporation tax charge on a director's loan can be avoided if the loan is repaid within nine months of the end of the company's corporation tax accounting period. This means there is no corporation tax to pay.

‘Bed and breakfasting’ is a term used to describe a situation where a director repays their loan just before the nine-month deadline to avoid the tax charge, only to borrow the same amount again shortly after. HMRC sees this as tax avoidance.

To prevent this, anti-avoidance rules are in place. If a director repays a loan of £5,000 or more but then borrows a similar amount again within 30 days, the tax relief on the repayment will be denied. For more information, see HMRC’s guidance on bed and breakfasting.

If you need to formalise the terms of a loan, you can make a Loan agreement. Do not hesitate to Ask a lawyer if you have any questions or need help navigating the rules on directors' loans.