What is chargeback?

‘Chargeback’ refers to the process that allows consumers to challenge and recover payments made from their debit and credit card accounts when things go wrong (eg if goods or services paid for are not delivered).

Rather than being a legal right, chargebacks form part of the rules of a card scheme (ie a payment system, like Visa, Mastercard, or American Express). They are governed by the relevant set of rules.

A consumer who wishes to dispute a transaction must contact their card issuer to make a chargeback claim in accordance with that issuer’s processes.

It should be noted that chargeback is separate from consumer protections under Section 75 of the Consumer Credit Act 1974, which only relate to credit card purchases over £100. For more information on this specific protection, read The Consumer Credit Act.

When can chargeback be used?

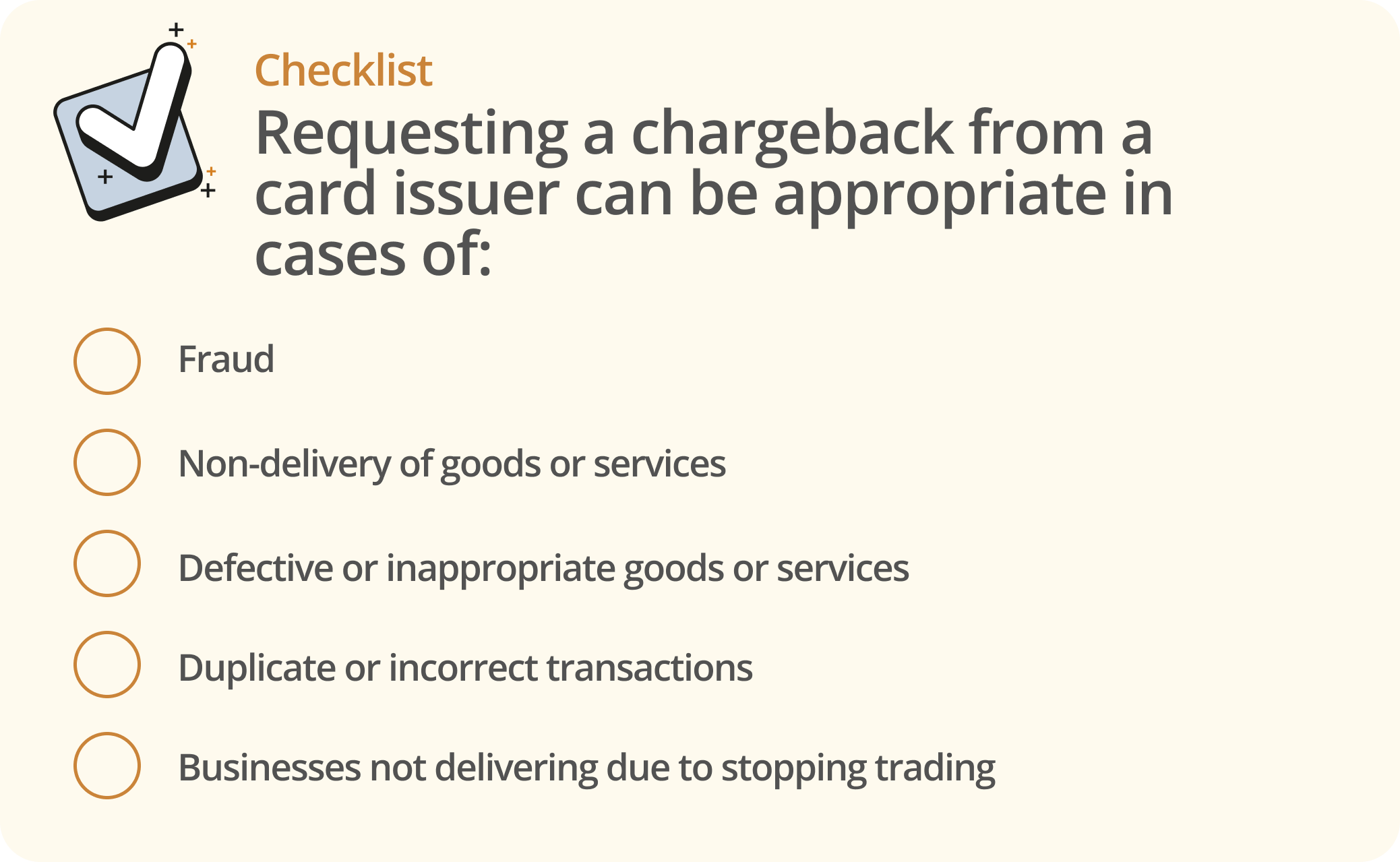

Some of the possible situations that chargeback may cover include when:

-

a business fails to deliver goods or services (eg because it’s gone into administration)

-

goods are defective or not as described

-

a transaction amount was incorrect or duplicated

-

if the transaction was fraudulent

-

a transaction was fraudulent

It should be noted that chargeback schemes’ requirements vary by card scheme (eg Visa will have different rules to Mastercard), so the circumstances under which schemes can be used may differ.

What are the conditions of chargeback?

Unlike the Section 75 protections for credit card purchases, there is usually no minimum amount that applies to disputed transactions.

There is generally a time limit of 120 days in which to claim chargeback. This normally starts on the day on which the consumer becomes aware of the problem. Additionally, claims must usually be made within an overall time limit of 540 days from the initial date of the transaction.

Once again, because chargeback schemes vary, conditions and restrictions may differ.

How are disputes resolved?

According to the Financial Ombudsman Service, card issuers should attempt chargeback if the cardholder has challenged a transaction and the situation aligns with the relevant card scheme’s rules.

If a request is not pursued when it would have been good practice to do so, or a similar issue applies – for example, if the card issuer refuses to process a chargeback or fails to make a successful attempt – the cardholder can complain to the Financial Ombudsman Service.

For more information, read the Financial Ombudsman Service’s guidance on chargeback complaints.

Can chargeback be used with PayPal transactions?

If you have an issue with a purchase that would usually prompt a chargeback request and you paid via debit card or charge card (or via credit card if section 75 does not apply) it’s often worthwhile requesting a chargeback. Whether your chargeback request will be actioned may depend on an individual card scheme’s rules. You should request the chargeback via your card provider as usual, rather than via PayPal.

PayPal also has its own internal Resolution Centre that you can utilise to seek resolution for payment disputes.