Where do I start when ending a partnership?

Before taking any action to dissolve a partnership, the first thing you should do is consult your partnership agreement or LLP agreement. A well-drafted agreement will contain clauses explaining what happens in either scenario: when a partner leaves or when the entire business is to be closed. Following the terms of your agreement is the surest way to handle the process smoothly and avoid disputes.

How can a partnership be ended?

A partnership can be ended in several ways, either by choice or automatically by law.

Dissolution by agreement

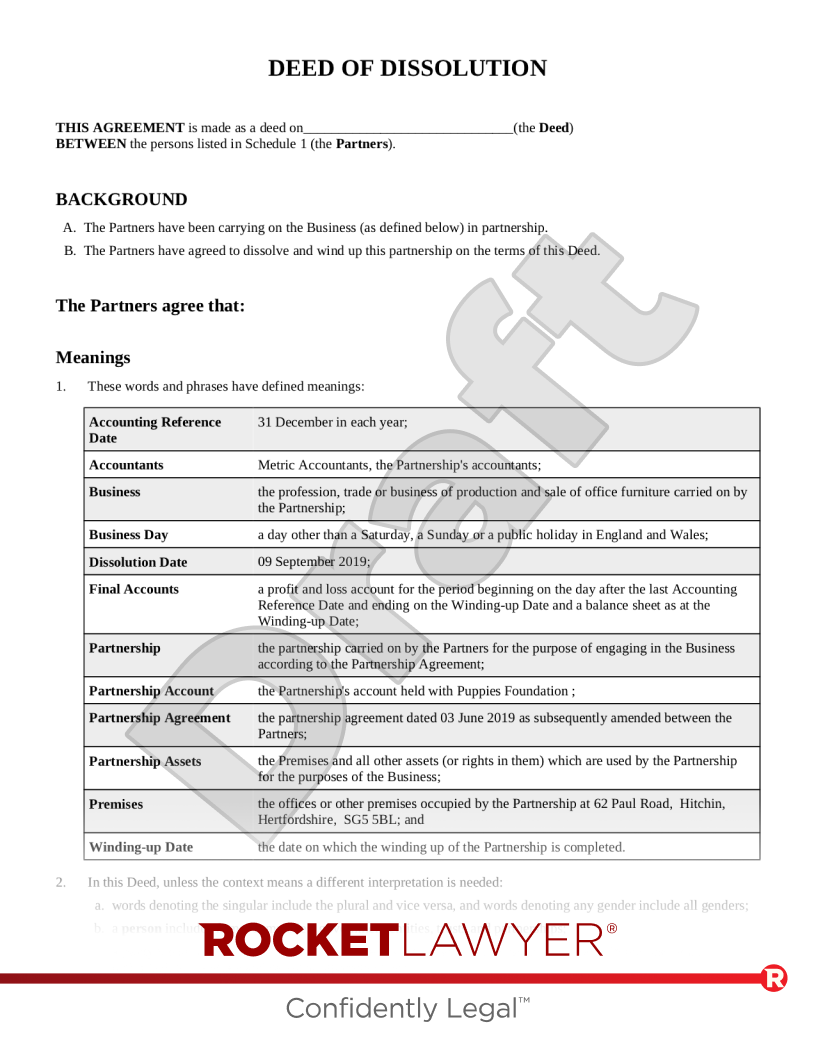

The most common method for ending a partnership is when all partners agree to dissolve the business. Partners can use a Dissolution of partnership deed to formally document the terms of the closure, including the date the business will cease trading and how its assets and liabilities will be divided during the winding-up period.

When a partner leaves or retires

By default, under the Partnership Act 1890, if a partner in a general partnership leaves or retires, the entire partnership is automatically dissolved. This would legally require the business to be wound up.

However, most partnerships prevent this by including a ‘buy-sell’ clause in their partnership agreement. This clause allows the remaining partners to buy the departing partner's share and continue the business seamlessly under a new arrangement.

Automatic dissolution

A partnership can be automatically dissolved by law due to certain events. However, the rules differ significantly for each structure.

A general partnership can be automatically dissolved if:

-

it was formed for a fixed term or specific project that has ended

-

it becomes illegal to operate, or

-

any partner dies or goes bankrupt (subject to provisions to the contrary in a partnership agreement)

A limited partnership (LP) and a Scottish limited partnership (SLP) can be automatically dissolved if:

-

it was formed for a fixed term or specific project that has ended

-

it becomes illegal to operate, or

-

the sole or last remaining general partner dies or goes bankrupt (this does not apply to limited partners)

Limited liability partnerships (LLPs) are not subject to automatic dissolution by law. As separate legal entities, they must be formally closed down through Companies House

Involuntary striking off by the registrar (for LLPs)

An LLP can be brought to an end by the registrar of Companies House without the members applying for it. This process, known as involuntary striking off, typically happens if an LLP fails to meet its legal obligations. The main reasons for this are:

-

if the LLP is no longer active - this is usually triggered when an LLP fails to file its annual accounts or confirmation statement. The registrar will attempt to communicate first, but if there is no response, a notice is published in the Gazette, and the LLP can be dissolved after two months

-

if the LLP was registered on a false basis - if the registrar believes that misleading, false, or deceptive information was provided during the LLP's initial registration, they can take action to strike it off. To do this, a notice is published in the Gazette, and the LLP can be struck off and dissolved in as little as 28 days if a valid reason not to do so is not provided

-

if the LLP fails to maintain an appropriate address - if an LLP's registered office is changed to a 'default' address (ie not an appropriate registered address) by Companies House, and the members fail to provide a new, appropriate address within 28 days, the registrar can begin the strike-off process

When will the dissolution be effective?

The date that a partnership dissolution legally takes effect depends on the specific event that triggers it. It's important to identify this date as it is crucial for finalising accounts and notifying HMRC. The effective date is determined as follows:

-

by agreement - if all partners agree to dissolve the business, the effective date is the date specified in your Dissolution of partnership deed. If no date is set, it is typically the date the agreement is finalised by all partners

-

by notice - if a partner gives notice to dissolve a partnership that has no fixed end date (a 'partnership-at-will'), the dissolution takes effect on the date mentioned in the notice. If no date is specified, it takes effect on the day the notice is communicated to the other partners

-

by expiry of a fixed term - if the partnership was created for a set period (eg five years) or for a single project, it is automatically dissolved when that term ends or the project is completed

-

by death or bankruptcy - for a general partnership or a sole general partner in an LP, the dissolution is effective immediately on the date of the partner's death, or the date a bankruptcy order is made against them

-

for an LLP striking off - it's important to distinguish between ceasing to trade and legal dissolution. For an LLP, the final dissolution only occurs when it is formally struck off the Companies House register, and the notice is published in the Gazette, which is typically at least three months after the application is made

The formal process of ending a partnership

Once the decision to dissolve the partnership has been made, you must follow a formal process to wind up its affairs.

Notifying interested parties

It is vital to publicise the dissolution to prevent any partner from being held liable for debts incurred after they have left. You must inform:

-

HMRC - to settle final tax obligations

-

customers and suppliers - to settle accounts and cancel contracts

-

employees - you must follow the correct procedures for ending their employment

-

the Gazette - placing a notice in the relevant official Gazette (eg the London or Edinburgh Gazette) provides public notice of the dissolution

Winding up finances and assets

The partnership’s finances must be formally wound up. This involves preparing final accounts to establish the business's financial position, settling all outstanding business debts and liabilities, and then distributing any remaining assets among the partners according to the terms of your partnership or LLP agreement (or equally, if no agreement exists).

Final tax obligations

You must inform HMRC that the partnership has ceased trading. The nominated partner, general partner, or designated member must file a final Partnership Tax Return. Each partner must also file a final personal Self Assessment tax return, declaring their share of the final period’s profits or losses.

You will also need to deregister for VAT if applicable.

Requirements for notifying Companies House

For partnerships registered with Companies House, there are additional steps to formally close the business or remove it from the register.

For general partnerships

As general partnerships are not typically registered with Companies House, there are no notification requirements for them when the business ends.

For limited partnerships (LPs and SLPs)

Ending an LP is decided by the general partners only. While there is no legal requirement to notify Companies House, it is good practice to do so by filing Form LP6. This places a notification on the public record, but be aware that the partnership’s name will remain on the live index of names.

For limited liability partnerships (LLPs)

An LLP can be formally removed from the Companies House register through the 'striking off' process. To do this, a majority of members must sign and submit Form LL DS01. You can only apply if the LLP has not traded, sold stock, or changed its name in the last three months. You must notify all members, creditors, and employees of the application within seven days. If there are no objections, the LLP will be struck off the register around three months later.

Ending a business partnership is a formal process that requires careful attention to legal, financial, and tax obligations to ensure a clean break for all partners. While your partnership or LLP agreement sets out the initial rules, a Dissolution of partnership deed is the key document for formally recording the terms of the closure and protecting you from future liabilities.

If you need to formally end your partnership or have specific questions about the process, do not hesitate to Ask a lawyer. If you wish to sell your business, consider using our Business sale and purchase service.