What is a joint venture?

A joint venture (JV) is a commercial collaboration where two or more businesses (the 'co-venturers') work together on a specific project or business activity. The key feature is that the parties remain separate legal entities while cooperating. JVs can be set up for a fixed period or a single purpose, such as developing a new product, entering a new market, or bidding on a large contract. Once the goal is achieved, the venture is often dissolved.

What are the benefits of a joint venture?

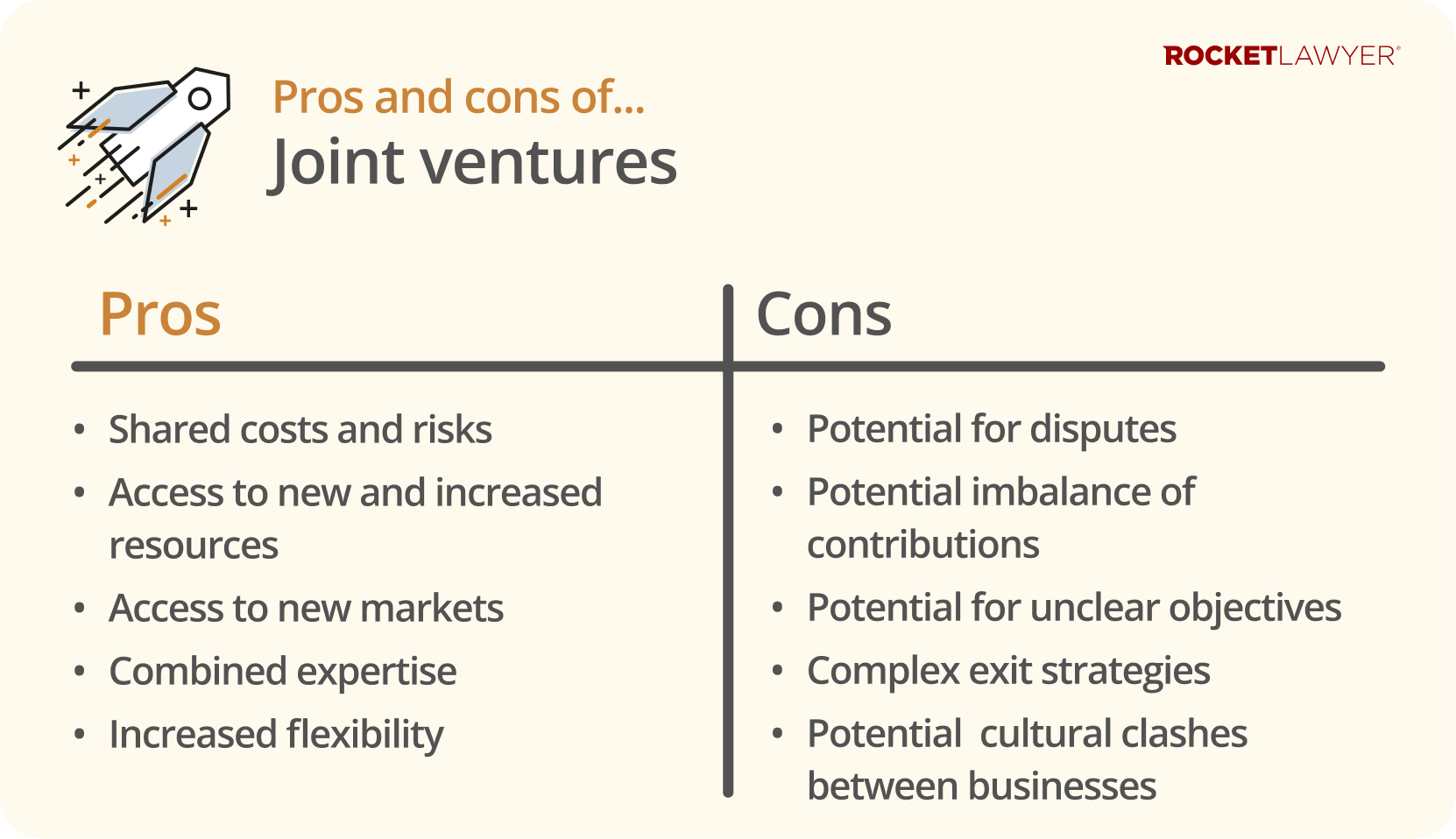

The main benefit of a joint venture is that it allows businesses to combine strengths and resources to pursue opportunities they couldn't tackle alone. Other key advantages include:

-

shared costs and risks - starting a new project can be expensive. A JV spreads the financial burden and risk among the partners

-

access to new markets - partnering with a business in a different region can provide an immediate entry point into a new geographical market

-

combined expertise - each partner brings unique skills, technology, and knowledge, leading to greater innovation and efficiency

-

increased resources - you gain access to your partner's staff, equipment, and distribution channels

-

increased flexibility - a JV is a flexible structure that can be tailored to a specific project and dissolved when it's complete, unlike a permanent merger

What are the risks of a joint venture?

While JVs offer significant benefits, they also come with risks that you need to manage carefully. A primary risk is the potential for disputes between the partners, especially if objectives aren't perfectly aligned from the start. Other potential disadvantages include:

-

unclear objectives - leading to disagreements over the venture's direction

-

an imbalance of contributions - where one partner feels they're putting in more work or resources

-

cultural clashes - between different business management styles, causing friction

-

complex exit strategies - which can make dissolving the JV difficult and contentious

What are the different types of joint ventures?

A joint venture isn't a legal structure in its own right; it's a commercial arrangement that must adopt a legal form. The choice of structure is a critical decision that affects everything from liability to governance. The two main approaches are structural JVs and contractual JVs.

Structural (or equity) JVs

A structural JV involves creating a new, separate legal entity to carry out the project. The co-venturers each own a stake (ie equity) in this new entity. This is a common choice for long-term, complex, or high-value projects.

The main vehicles for a structural JV are:

-

a private limited company (LTD) - the parties form a new company and become its shareholders. This is the most common structure as it creates a distinct legal personality and provides limited liability, meaning the co-venturers' assets are protected from the JV's debts. The venture is governed by the company's Articles of association and a detailed joint venture agreement (or a specific JV shareholders' agreement).

-

a limited liability partnership (LLP) - an LLP also has a separate legal personality and offers limited liability to its members. It combines the liability protection of a company with the operational flexibility of a partnership, and it is governed by an LLP agreement

Contractual JVs

A contractual JV does not involve creating a new legal entity. Instead, the relationship is governed entirely by a contract between the existing businesses. This structure is often used for shorter, more straightforward projects with a clearly defined scope, like a specific marketing campaign or a single construction project.

The entire venture is run according to a Collaboration agreement. A key risk is that if the arrangement isn't carefully managed, it could be legally deemed a general partnership, exposing the parties to unlimited liability for the venture's debts.

Note that a joint venture can also arise from contractual agreements such as Distribution agreements, Sales agency agreements, and intellectual property licences.

Ask a lawyer if you have any questions about the different types of JVs.

How do you start a joint venture?

Forming a successful joint venture is a multi-stage process that requires careful planning long before any final contracts are signed. The process can be broken down into two main phases: the groundwork and the formal agreement.

Phase 1: the groundwork

This preparatory phase is crucial for building a solid foundation for the JV. Rushing this stage is a common reason why ventures fail. Before drafting any final contracts, you should consider the following key actions:

-

define the business case - before approaching partners, be clear on your objectives. What is the scope of the project? What are the goals? What is the financial model?

-

select your partner and conduct due diligence - finding the right partner is critical. Once you have a potential partner, you must conduct due diligence. This is an investigation into their business to verify their financial stability, reputation, resources, and commercial standing. It also helps identify any potential liabilities

-

sign preliminary agreements - during negotiations, you'll share sensitive information. It's vital to have a Non-disclosure agreement (NDA) in place. You should also draft Heads of terms or a Letter of intent. These aren’t usually legally binding, but they set out the key commercial terms of the proposed JV, creating a clear roadmap for the final contract

Phase 2: choose the structure and finalise the agreement

With the groundwork complete and both parties ready to proceed, the next phase is to formalise the venture by taking two key legal steps:

-

choose your legal structure - you must decide whether to form a structural JV (creating a new company or LLP) or a contractual JV (working together under a contract). A structural JV is better for long-term projects where you want the protection of limited liability, while a contractual JV is often simpler for shorter, well-defined projects

-

draft the master JV agreement - this is the final, legally binding contract that governs the joint venture. The specific document you create will depend on the structure you've chosen, as each agreement serves a distinct purpose:

-

a joint venture agreement (or JV shareholders' agreement) - use this for a structural JV. It's a detailed contract that governs the relationship between the shareholders, the board of directors, funding, profit distribution, and exit strategies

-

a Collaboration agreement - use this for a contractual JV. Because there is no separate business, this agreement must be very comprehensive, defining each party's responsibilities, liabilities, and how intellectual property will be handled

-

an LLP agreement - use this if you've structured your JV as an LLP. It outlines the rights and duties of the members, profit sharing, and how the LLP will be managed

-

During this stage of your joint venture, you should get legal advice to ensure you are legally protected.

How do I exit a joint venture?

The process for ending a joint venture should be clearly defined in your initial agreement. This is often called the 'termination' or 'exit' clause.

An exit can be triggered when the project is completed (often by mutual agreement, meaning that all co-venturers need to agree to bring the JV to an end), or it can be initiated by one of the parties. The agreement should dictate:

-

how assets are to be valued and sold, or distributed

-

any notice periods required to leave the venture

-

any pre-emption rights (ie giving the remaining partners the first right to buy the leaving partner's shares or interest)

If the JV is a limited company, you can also exit by selling your shares, selling the entire company (eg by using a Share purchase agreement), or by winding up the company. Without a clear agreement, ending the venture can become complex and lead to disputes.

In an LLP, the LLP agreement covers what happens when a partner wishes to leave. Similarly, if your JV is a partnership, the Partnership agreement covers these situations.

If you are starting a new project with a partner, you can enter into a tailor-made joint venture agreement to protect your interests. For simpler collaborations, a Collaboration agreement may be more suitable. If you have any questions, don't hesitate to Ask a lawyer.