Plan and manage your Joint Living Trust: Joint Living Trust Funding Worksheet

What is a Joint Living Trust Funding Worksheet?

A Joint Living Trust Funding Worksheet can help you and your spouse plan and manage your living trust. Maybe you want to figure out which assets to move, or maybe you just want to work out how to do it. A Joint Living Trust Funding Worksheet can give you a solid foundation to get started.

A living trust can be a great way to manage your assets a Joint Living Trust Funding Worksheet can help make that process easier. Make sure you and your spouse are on the same page: which assets are going to be moved to the living trust? What are all the assets you have? You may also need a bill of transfer document to keep your filing updated, or maybe you want to keep certain assets separate. If you already have joint assets in a living trust, you can make changes to ensure that some assets are your individual property or make current individual assets joint. It's your decision. A Joint Living Trust Funding Worksheet can help you stay organized.

When to use a Joint Living Trust Funding Worksheet:

- You're married and thinking about a living trust.

- You and your spouse want to make a list of assets that might go into a living trust.

- You and your spouse need to create a property schedule.

- You and your spouse want to create a bill of transfer ownership.

- You need to change assets to joint or individual ownership.

How do I get my Joint Living Trust Funding Worksheet reviewed?

If you already have a Joint Living Trust Funding Worksheet and want to have it reviewed, or if you have questions about creating or using one, there are a few ways to get help.

Use Rocket Copilot to ask questions or review your document; this helps you better understand what it says and identify anything that may need a closer look.

If you are looking for help from a Legal Pro, you can also ask a question and receive a response within one business day, or request a more in-depth document review.

Sample Joint Living Trust Funding Worksheet

The terms in your document will update based on the information you provide

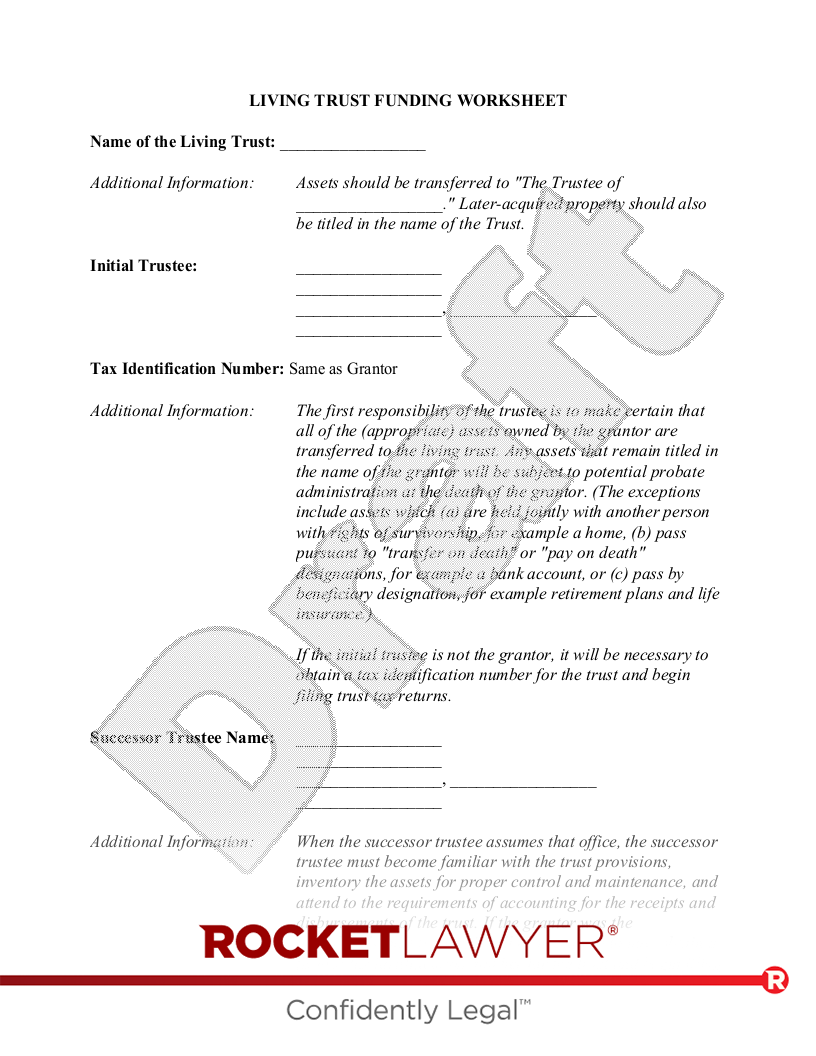

LIVING TRUST FUNDING WORKSHEET

Name of the Living Trust:

| Additional Information: | Assets should be transferred to "The Trustee of ." Later-acquired property should also be titled in the name of the Trust. |

| Initial Trustee: |

,

| Initial Co-Trustee: |

,

Tax Identification Number:

| Additional Information: | The first responsibility of the trustee is to make certain that all of the (appropriate) assets owned by the grantor are transferred to the living trust. Any assets that remain titled in the name of the grantor will be subject to potential probate administration at the death of the grantor. (The exceptions include assets which (a) are held jointly with another person with rights of survivorship, for example a home, (b) pass pursuant to "transfer on death" or "pay on death" designations, for example a bank account, or (c) pass by beneficiary designation, for example retirement plans and life insurance.) |

If the initial trustee is not the grantor, it will be necessary to obtain a tax identification number for the trust and begin filing trust tax returns.

| Successor Trustee Name: |

,

| Additional Information: | When the successor trustee assumes that office, the successor trustee must become familiar with the trust provisions, inventory the assets for proper control and maintenance, and attend to the requirements of accounting for the receipts and disbursements of the trust. If the grantor was the immediately-past trustee, it will be necessary to now obtain a federal tax identification number for the trust and begin filing trust tax returns. |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Include in Trust Property Schedule? |

| Living Trust Tax Return | As long as the grantor is a trustee (and, for a joint living trust, as long as the grantors file a joint return), it is not necessary to file a separate tax return for the trust. All income and deductions of both the grantor and the trust are reported on the grantor's personal income tax return (joint personal return for the grantors of a joint living trust). However, if and when the grantor is no longer a trustee, the trust must obtain its own tax identification number and file a separate income tax return. While the grantor is alive and can therefore still revoke the trust, the tax return is merely a "pass-through" return where the trust allocates the income to the beneficiaries who received the income. This allocation of income is detailed on schedules that are filed with the IRS by both the trust and the individual beneficiaries. When the grantor dies and the trust therefore becomes irrevocable, the beneficiaries are still taxed on the income paid to them. But if some of the income is retained in the trust, the trust pays the tax on that income. |

Especially after the grantor's death, the trust may provide that trust INCOME is to be paid to one beneficiary, perhaps the spouse, while the trust PRINCIPAL is to be maintained intact for the "remainder" beneficiaries, those who will receive the assets that remain in the trust after the death of the income beneficiary. In such cases, it is especially important for the trustee to follow the terms of the trust instrument, or established state law if the trust is silent, in making allocations between income and principal. Income receipts consist of earnings from the investment of the principal, usually including such items as dividends, interest, rents and royalties. Principal receipts consist of such items as the proceeds received from the sale of assets, stock dividends, casualty insurance proceeds, royalties from depletable resources, and principal payments from loans and installment obligations. Expenses attributable to income consist of the costs of administering and preserving the trust property. Expenses attributable to principal consist of the costs of investing and reinvesting the principal, including defending an action to protect the trust property, making capital improvements to the assets, and taxes on capital gains.

| Tax Basis in Assets | Assets transferred to a living trust carry with them the same tax "basis" (used to compute taxable gain, if any, upon a sale of the asset) as the grantor had in those assets prior to the transfer. Upon the grantor's death, however, a living trust generally acquires a date-of-death value basis in all such assets. This is the same tax benefit applicable at death to assets owned in the name of individuals. Thus, there is no disadvantage to transferring appreciated assets into the living trust. |

An example may be useful: Thomas purchased 100 shares of Acme stock in 1981 for $1000, which $1000 then constitutes his cost "basis" on which to compute taxable gain if he should later sell the stock. In 1998 the stock is worth $2500. If Thomas sells the stock in 1998, he must report $1500 in taxable gain. If he dies in 1998 still owning the stock, the basis is "stepped up" tax-free to the stock's $2500 date-of-death value, resulting in no taxable gain if his beneficiaries immediately sell it for $2500. Likewise, if Thomas transfers the stock to his living trust at any time before his death in 1998, the basis inside the trust remains at $1000 while Thomas is alive, but enjoys a step-up basis to $2500 at his death.

| Isolation of Trust Assets | It is important to respect the distinction in the ownership of trust assets -- assets owned by the trust as opposed to owned individually by the grantor. The trustee is only a caretaker of the trust assets and must keep appropriate records of income, expenses, additions and distributions of the trust. Especially when a successor trustee assumes the trustee duties, all cash should be channeled through a separate trust-owned bank account. |

Protecting Trust Assets

Insurance Coverage:

| Insurance Company: |

| Type of Coverage: |

| Policy Number: |

| Agent: |

| Address: |

| City, state, zip: | , |

| Phone: |

| Additional Information: | When the trust has been signed and assets transferred to the trust, the trust is then a viable, legal entity and the trustee has full authority, power and control to manage the trust assets. The trustee also has certain responsibilities to preserve and protect the assets. |

Insurance. After insured assets have been transferred to a living trust, the insurance agent should be notified of the change. The named insured on the policy should be amended to add the trustee. The change should not affect the coverage or cost of the policy.

Documents. After the title of each asset has been transferred from the grantor to the trustee, there will be various title documents such as deeds, stock certificates, bank certificates, etc., which evidence the fact that these assets are owned by the trust. Each such title document should be kept in a safe place, such as a safe deposit box, and the person named as the successor trustee should be notified as to the location of these documents. If any securities are held in "bearer" form, such as bearer bonds or unregistered securities, it is recommended that a separate safe deposit box be obtained and clearly identified as holding only trust assets. If such items were instead held in the grantor's safe deposit box or at the grantor's home, it could be argued that those assets should be subject to probate administration, that is, that they are not effectively owned by the trust. Additionally, the safe deposit box should be held in the name of the trust so that the successor trustee will have the right to gain entrance to the box.

All of 's household goods, furniture and furnishings, now owned or later acquired.

All of 's household goods, furniture and furnishings, now owned or later acquired.

All of 's clothing and personal effects, now owned or later acquired.

All of 's clothing and personal effects, now owned or later acquired.

All of 's jewelry, now owned or later acquired.

All of 's jewelry, now owned or later acquired.

All of 's untitled recreational equipment, now owned or later acquired.

All of 's untitled recreational equipment, now owned or later acquired.

All of 's collections, collectibles and antiques, now owned or later acquired.

All of 's collections, collectibles and antiques, now owned or later acquired.

All of 's works of art, now owned or later acquired.

All of 's works of art, now owned or later acquired.

, , Account Number

, Account Number

Shares , CUSIP No.

Shares

interest in

interest in

Savings Bond, Serial Number

, Serial Number

real estate located at

Promissory Note from , dated , in the face amount of

Installment Contract with , dated , in the original amount of

units

()

()

()

life insurance policy number , insuring , face amount

All of 's household goods, furniture and furnishings, now owned or later acquired.

All of 's household goods, furniture and furnishings, now owned or later acquired.

All of 's clothing and personal effects, now owned or later acquired.

All of 's clothing and personal effects, now owned or later acquired.

All of 's jewelry, now owned or later acquired.

All of 's jewelry, now owned or later acquired.

All of 's untitled recreational equipment, now owned or later acquired.

All of 's untitled recreational equipment, now owned or later acquired.

All of 's collections, collectibles and antiques, now owned or later acquired.

All of 's collections, collectibles and antiques, now owned or later acquired.

All of 's works of art, now owned or later acquired.

All of 's works of art, now owned or later acquired.

All of 's household goods, furniture and furnishings, now owned or later acquired.

All of 's household goods, furniture and furnishings, now owned or later acquired.

All of 's clothing and personal effects, now owned or later acquired.

All of 's clothing and personal effects, now owned or later acquired.

All of 's jewelry, now owned or later acquired.

All of 's jewelry, now owned or later acquired.

All of 's untitled recreational equipment, now owned or later acquired.

All of 's untitled recreational equipment, now owned or later acquired.

All of 's collections, collectibles and antiques, now owned or later acquired.

All of 's collections, collectibles and antiques, now owned or later acquired.

All of 's works of art, now owned or later acquired.

All of 's works of art, now owned or later acquired.

All of 's household goods, furniture and furnishings, now owned or later acquired.

All of 's household goods, furniture and furnishings, now owned or later acquired.

All of 's clothing and personal effects, now owned or later acquired.

All of 's clothing and personal effects, now owned or later acquired.

All of 's jewelry, now owned or later acquired.

All of 's jewelry, now owned or later acquired.

All of 's untitled recreational equipment, now owned or later acquired.

All of 's untitled recreational equipment, now owned or later acquired.

All of 's collections, collectibles and antiques, now owned or later acquired.

All of 's collections, collectibles and antiques, now owned or later acquired.

All of 's works of art, now owned or later acquired.

All of 's works of art, now owned or later acquired.

, VIN

units

BILL OF TRANSFER

We, and (the "Grantors") hereby sell, transfer, and assign to the Trustee of , all of our right, title and interest in the assets listed on the attached Schedule A.

| _____________________ | ________________________________ |

| Date |

| ________________________________ |

Bill of Transfer

Schedule A

interest in

interest in

Promissory Note from , dated , in the face amount of

Installment Contract with , dated , in the original amount of

units

()

| ________ | ________ |

| Initials | Initials |